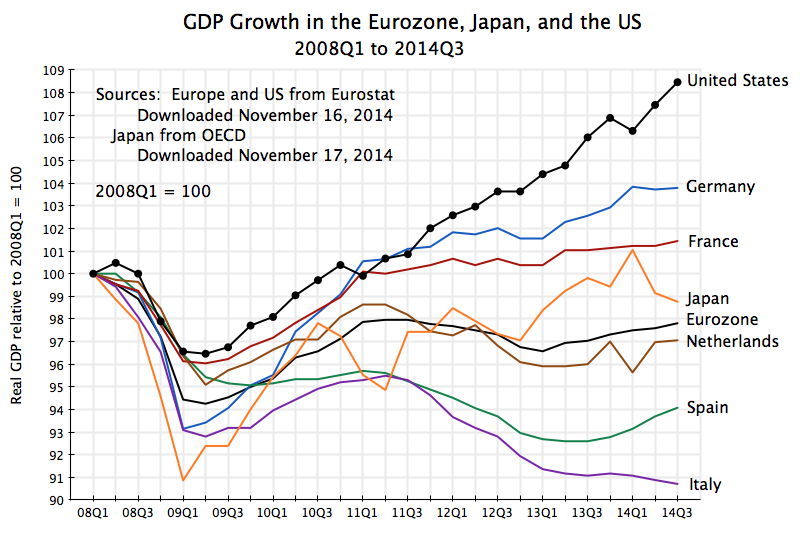

A recent post on this blog looked at the disappointing growth in the Eurozone since early 2011, when Europe shifted to austerity policies from its previous focus on recovery from the 2008 economic and financial collapse. There has indeed been no growth at all in the Eurozone in the three and a half years since that policy shift, with GDP at first falling by about 1 1/2% (leading to a double-dip recession) and then recovering by only that same amount thus far. The recovery has been exceedingly slow, and prospects remain poor.

The consequences of the shift to austerity can be seen even more clearly in the unemployment figures. See the chart above (the data comes from Eurostat). Unemployment in Europe rose sharply starting in early 2008 and into early 2009. But it then started to level off in late 2009 and early 2010 following the stimulus programs and aggressive central bank programs launched in late 2008. Unemployment in the US followed a similar path during this period, and for similar reasons.

But the paths then diverged. After peaking in early 2010 at about 10% and then starting to come down, the unemployment rate in the Eurozone switched directions and started to rise again in mid-2011. It reached 12.0% in early 2013 and has since come down slowly and only modestly to a still high 11.5% currently. In the US, in contrast, the unemployment rate reached a peak of 10.0% in October 2009, and has since fallen more or less steadily (with bumps along the way) to the current 5.8% (as of October 2014). It has been a slow recovery, but at least it has been a recovery.

This divergence began in 2010, as Europe shifted from its previous expansionary stance to austerity. Influential Europeans, in particular German officials and Jean-Claude Trichet (then the head of the European Central Bank) argued that not only was austerity needed, but that austerity would be expansionary rather than contractionary. We now see that that was certainly not the case: GDP fell and unemployment rose.

The most clear mark of that shift in policy can be found in the actions of the European Central Bank. ECB interest rates had been kept at a low 0.25% for its Deposit Facility rate (one of its main policy rates) for two years until April 2011. The ECB then raised the rate to 0.50% on April 13, and to 0.75% on July 13, 2011. But European growth was already faltering (for a variety of reasons), and it was soon recognized by most that the hike in ECB interest rates had been a major mistake. Trichet left office at the end on his term on November 1, replaced by Mario Draghi. On November 9 the ECB Board approved a reversal. The Deposit Facility rate was cut to 0.50% that day, to 0.25% a month later on December 11, and to 0.00% on July 11, 2012.

Fiscal policy had also been modestly expansionary up to 2010, as monetary policy had been up to that point, but then went into reverse. Unfortunately, and unlike the quick recognition that raising central bank interest rates had been a mistake, fiscal expenditures have continued to be cut since mid-2010.

Germany in particular called for cuts in fiscal spending for the members of the Eurozone, and forced through a significantly stricter set of rules for fiscal deficits and public debt to GDP ratios for Eurozone members. Discussions began in 2010, amendments to the existing “Stability and Growth Pact” were approved on March 11, 2011, and a formal new treaty among Eurozone members was signed on March 2, 2012. The new treaty (commonly referred to as the Fiscal Compact) mandated a balanced budget in structural terms (defined as not exceeding 0.5% of GDP when the economy was close to full employment, with a separate requirement of the deficit never exceeding 3% of GDP no matter how depressed the economy might be). Financial penalties would be imposed on countries not meeting the requirements.

The result was cuts to fiscal expenditures:

Government fiscal expenditures in the Eurozone had been growing in real terms in line with real GDP up to 2008, at around 2 to 3% a year. With the onset of the crisis, fiscal expenditures at first grew to counter the fall GDP. But instead of then allowing fiscal expenditures to continue to grow even at historical rates, much less the higher rates that would have been warranted to offset the fall in private demand during the crisis, fiscal expenditures peaked in mid-2010 and were then cut back. By 2014 they were on the order of 14 to 15% below where they would have been had they been allowed to keep to their historical path. This has suppressed demand and therefore output.

The path of US real government expenditures is also shown on the graph. Note that government expenditures here include all levels of government (federal, state, and local), and include all government expenditures including transfers (such as for Social Security). Government expenditures for the Eurozone are defined similarly. The US data comes from the BEA, while the Eurozone data comes from Eurostat.

Government expenditures in the US also peaked in 2010, as they had in the Eurozone, and then fell. This has been discussed in previous posts on this blog. But while US government expenditures fell after 2010, they had grown by relatively more in the period leading up to 2010 than they had in the Eurozone, and then fell by relatively less. They have now in 2014 started to pick up, mostly as a consequence of the budget deal reached last year between Congress and President Obama. State and local government expenditures, which had been severely cut back before, have also now stabilized and started to grow as tax revenues have begun to recover from the downturn. And in part as a result, recent GDP growth in the US has been good, with real GDP growing by 4.6% in the second quarter of 2014 and by 3.9% in the third quarter.

The fiscal path followed in the US could have been better. An earlier post on this blog calculated that GDP would have returned to its full employment level by 2013 if government spending had been allowed to grow merely at its historical rate. And the US could have returned to full employment by late 2011 or early 2012 if government spending had been allowed to grow at the more rapid rate that it had under Reagan.

But with the fiscal cuts, unemployment has come down only slowly in the US. The recovery has been the slowest of any in the US for at least 40 years, and fiscal drag by itself can account for it. But at least unemployment has come down in the US, in contrast to the path seen in Europe.

You must be logged in to post a comment.