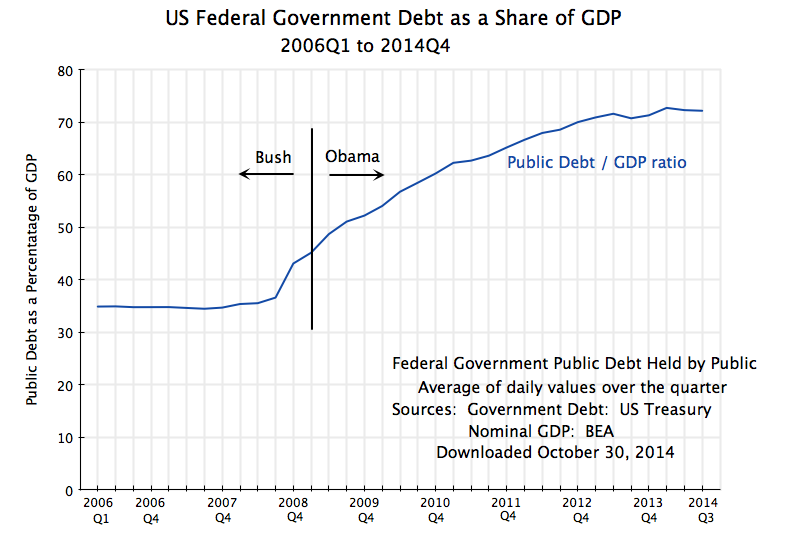

The US federal government debt to GDP ratio is falling. A few years ago, conservative critics (such as Congressman Paul Ryan) argued that if drastic action were not taken immediately to slash government expenditures, consequent rapidly rising federal government debt would stifle growth and spiral ever upwards. Liberals (such as Paul Krugman) argued that the federal deficit and debt were far less of a concern than these critics asserted: With the recovery of the economy, both would soon start to fall. And the detailed projections from the Congressional Budget Office backed this up, with projected falls in the debt to GDP ratio for at least a few years. There would be a rise later if nothing further is done, in particular on medical costs, but the question at issue here is whether the debt to GDP ratio could fall in the near term without drastic cuts in government expenditures. Conservatives asserted it would not be possible.

But these were projections and assertions. The chart above shows the actual data. With the release this morning by the Bureau of Economic Analysis of its first estimate of 2014 third quarter GDP (growth at a fairly solid 3.5% real rate), one can now see that there has been a downward turn in the debt to GDP ratio. The ratio peaked at 72.8% of GDP in the first quarter of 2014, and dropped to 72.2% as of the third quarter.

The federal government debt figure used here is the debt held by the public. There are also various trust funds (most notably the Social Security Trust Fund) that formally hold government debt in trust, but this reflects internal accounting within government. The figures come from the US Treasury, with quarterly averages taken based on an average of the amounts outstanding each day of the quarter. This average is then taken as a share of nominal GDP for the quarter (nominal GDP since debt is also a nominal concept). And since nominal GDP reflects the flow of production over the course of the quarter, taking the daily average debt outstanding over the course of the quarter will better reflect the debt burden than simply taking debt as of the end of the quarter and dividing this by GDP (although this is commonly done by many).

There was an earlier downward dip in the public debt to GDP ratio in the third quarter of 2013, but this was due to special circumstances surrounding the delay by Congress to approve a rise in the statutory government debt ceiling. Various accounting tricks were used to delay recognition of items that would add to the formally defined government debt in order to keep under the ceiling, which artificially suppressed the debt to GDP ratio in that quarter. This carried over into the fourth quarter, with the Republicans forcing a shutdown of the federal government from October 1 by not approving a new budget. The dispute was not resolved until October 16, when deals were reached to raise the debt ceiling and to approve a budget. The debt ratio then returned to its previous path.

The fall in the debt ratio in 2014 is more significant. Accounting tricks are not now being used due to debt ceiling disputes, and the fall reflects the continued fall in the fiscal deficit coupled with reasonably sound growth. The deficit is estimated to have totaled $483 billion in fiscal 2014 (which just ended on September 30), or 2.8% of GDP. This is sharply down from the $1.4 trillion (or 9.8% of GDP) of fiscal 2009, in the first year of the downturn. The fiscal deficit has fallen primarily due to the recovery, but also due to cuts in federal government expenditures under Obama since 2010. While not nearly as drastic as Congressman Ryan and other conservatives had insisted would be necessary, government spending has still fallen under Obama, in contrast to the increases allowed in previous downturns.

Note that the government expenditure cuts that were done do not represent what would have been the desirable path in deficit reduction: As discussed in an earlier post on this blog, it would have been far better to follow a fiscal path similar to that followed by Reagan and others in earlier downturns, with government spending allowed to grow so that the economy could have more quickly returned to full employment. Once full employment was reached, one would then consider fiscal cuts, if warranted, to address any debt concerns.

The path followed has thus been far from optimal. But it has shown that the alarms raised by the conservative critics, that the debt to GDP ratio could not fall without drastic government cutbacks (far more severe than that seen under Obama), were simply wrong.

You must be logged in to post a comment.