Source: James Hansen, Global Temperatures, update of December 18, 2017

A. Introduction

The final element of a comprehensive tax reform would be a tax to address climate change. Previous posts have looked at what a true reform of corporate and individual income taxes could look like, plus what could be done to ensure Social Security benefits can continue to be paid in accord with current formulae, and indeed enhanced. This post will look at a tax on greenhouse gas emissions (commonly called a carbon tax, as carbon dioxide is the primary contributor) to address global warming.

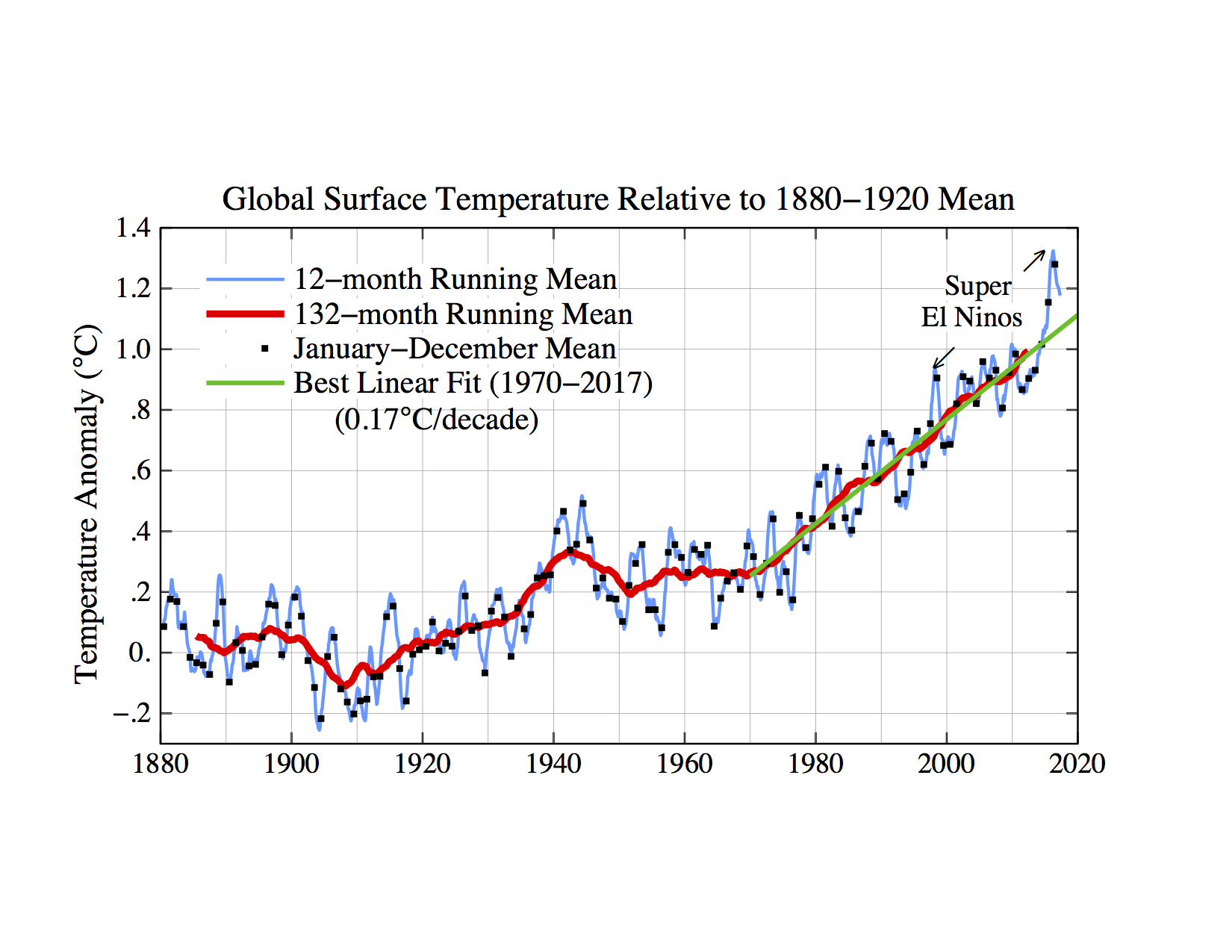

There is no doubt the planet is warming – the chart above shows the most recent estimates. And this is primarily due to our economies pouring into the air carbon dioxide and certain other gases (such as methane) that lead to heat being retained by the atmosphere. These greenhouse gases have warmed the planet, leading to an increased frequency of extreme weather events such as the series of remarkably intense hurricanes that hit the US this August and September. The cost, already being incurred, has been staggering. Early estimates of the cost of just Hurricanes Harvey (which hit Texas) and Irma (which hit Florida) reach $290 billion. Hurricane Maria (which hit Puerto Rico) may have cost Puerto Rico as much as $95 billion according to an early estimate (and this excludes the cost to other Caribbean nations it hit).

As I am writing this (January 3, 2018), record-breaking cold has swept over much of the eastern half of the US. And it is forecast to get worse over the next few days. Trump has, not surprisingly, tweeted that this cold shows that global warming is not true. But this illustrates well his ignorance. First, there is more to the world than the eastern US. There is also today unseasonably warm weather in the western US (especially Alaska, relative to what is normal there), as well as in Europe, Russia, and especially Siberia. Overall, the average global surface temperature today is 0.5 degrees Celsius above the 1979 to 2000 average for this time of year, and 0.9 degrees Celsius above that average in the Northern Hemisphere. But second, that blast of cold hitting the eastern US should not be taken as a surprising outcome of global warming. Warming leads to greater volatility in atmospheric currents, including in the jet streams that allow (or block) cold air to come down from the Arctic.

One cannot, of course, attribute with certainty any particular severe weather event (whether hurricanes, extreme hot or cold temperatures, drought or floods, and more) to climate change. We had severe weather events before global warming became significant. But the same is true of lung cancer and smoking: One cannot attribute any individual’s death from lung cancer to his or her smoking. People died of lung cancer before smoking became common. The issue, rather, is that smoking increases the likelihood of getting lung cancer. Similarly, global warming increases the likelihood and hence frequency of severe weather events.

And that is precisely what we have seen. Severe weather events have increased in number in recent years as the planet has warmed and as climate change models have predicted. A database maintained by the National Oceanic and Atmospheric Administration (NOAA, the home of the National Weather Service) has kept track since 1980 of the number of weather and climate disasters in the US which each cost $1 billion or more (in 2017 prices). Over that close to 37 year period the 7 worst years (in terms of the number of such disasters) have all come in the last 10 years (including 2017, which as of end September already had tied the worst full year so far, and will exceed it once fourth quarter data is included).

Global warming, arising from man-made emissions of carbon dioxide (CO2), methane (natural gas), and certain other gases (together, greenhouse gases or GHGs, for the greenhouse effect they cause), is thus imposing a huge cost already on society, and one which will get worse as the planet warms further. It is thus a mark of confusion to say, as Trump and many Republican politicians have, that we cannot “afford” to address the causes of the warming planet. We are already bearing the costs, and those costs will get far worse if nothing is done. The question is whether steps will be taken to reduce those costs by addressing the underlying causes.

The issue is that the costs such GHG emissions cause are not being borne by those who emit those gases. The emitters of GHGs are in effect being subsidized, and encouraged to burn fossil fuels rather than make use of a cleaner alternative. And when a producer is not bearing the full cost of what he is producing, it will be badly done. The key is to charge a tax or fee on such production equal to the cost being imposed on others, so that the producer faces the full cost of what he is making. The producer will then have a reason to make suitable choices on how the product can be made at the least cost to all. And consumers, facing the full costs of what they are buying, can then make suitable choices on whether to buy one product or another.

A suitable tax on greenhouse gas emissions would bring prices in line with the total costs being incurred. A comprehensive tax reform should include this. And it would be straightforward to implement. There is indeed a well worked out plan being promoted by a group of traditional Republican conservatives, the Climate Leadership Council, with the active involvement and endorsements of several Treasury Secretaries in past Republican administrations (Hank Paulson, James Baker, and George Schultz); as well as of individuals such as Michael Bloomberg and liberal and conservative economists such as Larry Summers, Martin Feldstein, and Gregory Mankiw; companies such as ExxonMobil, General Motors, and Shell; and environmental organizations such as The Nature Conservancy and Conservation International.

It is a good plan, and I would suggest basically just copying it. The proposal will be explained below. A one-page summary of the Climate Leadership Council’s specific proposal is available here, while a more complete description is available here. A very similar proposal has also been assessed by the US Treasury, with a brief summary of the Treasury analysis available on the Climate Leadership Council website here, while the complete Treasury analysis is available here on the Treasury website (assuming the Trump administration has not taken it down). The Treasury assessment is excellent, as it reviews precisely how one could implement such a tax, including the practicalities, and arrives at specific quantitative estimates of the impact on different income groups. The analysis below will basically follow the variant of the plan as assessed by the Treasury.

This post will first provide a description of that plan, how it could be implemented, and what the impact on prices might be. Importantly, clean alternatives exist for many of the processes which emit GHGs, particularly from the burning of fossil fuels, which thus can be substituted for processes emitting those gases. This would limit the price impact and smooth the way to sharp reductions in GHG emissions. Furthermore, a key feature of this plan is that the revenues that would be collected by the carbon tax would all be rebated to the American population. The final section will discuss this and the distributional implications. The plan would be revenue neutral – the aim is to change prices so that they fully reflect the costs being incurred, not to raise revenues. And the rebates would be distributionally positive, with the bottom seven deciles of the population (the bottom 70%) coming out ahead after the rebates. Only the top three deciles (top 30%) would see a net loss, as a direct consequence of their disproportionate share in consumption of goods that cause the GHG emissions in the first place.

B. A Carbon Tax to Address Climate Change

In brief, under this proposal a tax would be charged for each unit of GHG pollution emitted. The Climate Leadership Council would set the tax to start at $40 per ton of CO2, with the taxes on other GHGs set in proportion based on their global warming impact per ton relative to that of CO2. This is often called simply a carbon tax, although it is in fact a tax on CO2 (carbon dioxide) emissions and on other GHGs in proportion to their global warming impact. The tax would then rise in real terms over time. The start date would presumably have been 2018, although this was not explicit (the proposal came out in early 2017). The Treasury variant examined a price of $49 per ton of CO2-equivalent starting in 2019 (with some phasing in of the goods to which it would apply until 2021), and then increasing at a rate of 2% a year in real terms from 2019.

Importantly, all revenues collected would be returned directly to the American population. The impact on the federal budget thus would be revenue neutral. There would also be border adjustments for imports and exports (discussed below). The Treasury estimates that at $49 per ton, the carbon tax would lead to a rebate in the first year (2019) of $583 per person, or $2,332 for a family of four. Scaling this in proportion, a $40 per ton carbon tax would lead to a rebate of $476 per person, or $1,904 for a family of four. And the tax would be highly progressive. The Treasury estimated that there would on average be net income gains for the bottom 70% of the population. That is, their rebates would be greater than the higher amounts they would need to spend on goods and services to reflect the cost of the carbon tax.

In more detail, under this plan a price (whether $40 or $49 to start) would be charged which reflects the cost to society of the GHGs being emitted as part of the production process for the good or service being produced. This is called the “social cost of carbon”, and while the concept is clear, it is difficult in practice to estimate precisely. Its value will depend on factors which are difficult to know at this point in time, including the full cost to our economies (starting now and extending many decades into the future) as a consequence of climate change, the cost of technologies to limit GHG emissions (again starting now, and then for decades into the future), and the appropriate values for parameters such as the proper discount rate to use to put the costs and benefits over this range of time all into the prices of today. A fundamental difficulty of GHG emissions is that their impact is not just in the near term, but can extend for centuries. They remain in the atmosphere for a very long time.

Thus while starting at a reasonable cost of carbon (whether $40 or $49) is important, probably more important is how this price should be adjusted over time to reflect actual experience. Some predictability in the path is also valuable, so firms can make their investment decisions accordingly. Thus the Climate Leadership Council plan would have the price rise in real terms over time at some unspecified pace, while the Treasury assessment assumed concretely a rise of 2% a year in real terms. Such a 2% real increase is reasonable.

One should, however, also recognize the inherent uncertainty, as the proper price on carbon is difficult to know before we have any experience with such a plan. Thus one should allow for reassessment and adjustment, perhaps every five years or so, with the pace of price adjustment increased or decreased depending on the observed response. The pace would be raised if we find that GHG emissions are not falling at the pace needed, or reduced if we find GHGs are falling at a more rapid pace than anticipated and needed. Past experience with market mechanisms to reduce pollution (in particular the use of trading schemes to reduce sulfur dioxide and nitrogen oxides pollution) worked surprisingly well, with costs well below what had been anticipated and what would have been incurred through traditional regulatory regimes. The same would be likely, in my view, if we would start to price GHG emissions.

Pricing GHG emissions is also relatively straightforward administratively for the bulk of GHG sources. Fully 76% of GHG emissions in the US come from the burning of fossil fuels. This rises to 83% if one adds in the emission of GHGs in the production of the fossil fuels themselves (at the mine or well-head) plus from the non-energy use of fossil fuels. The carbon tax thus could be applied at the level of the limited number of power plants that still burn coal; at the level of petroleum refineries where substantially all crude oil must be processed; and at the level of gas pipelines as substantially all natural gas is transported via pipelines. A limited number of industrial plants then account for a significant share of the remainder. These include from the use of coking coals in the production of iron and steel; from the production of petrochemicals such as plastics; and GHGs resulting from the production of cement, glass, limestone, and similar products. For these, it would be straightforward to apply a carbon tax at the factory or plant level. There would remain GHG emissions from a range of resources, including in particular in agriculture (accounting for about 8% of GHG emissions in the US), and the Treasury analysis assumes the carbon tax would not apply to those sources. But they are a small share of the total, and an issue one could address in the future.

A key part of the plan is that there would also be a border tax adjustment, where exports would receive a rebate for the carbon taxes paid on their production, while imports would be charged a carbon tax based on the GHGs emitted in their production. The rebate for exports means that US production would not be disadvantaged by being located here, and there would be no incentive from this source to move such plants abroad. This addresses the Trump criticism (and confusion) that such carbon taxes will make US industry uncompetitive. And imports would be charged a carbon tax based on their GHG emissions to the extent such imports do not already reflect such charges (which would likely be the case, as they too would likely be given rebates in their home countries on carbon taxes paid, just as US exports would be).

A feature of this border tax adjustment is that revenues for the US would be generated (and rebated to the US population) in the case where other countries are not themselves charging a carbon tax (or the equivalent, such as in a cap and trade system), but also (given the US trade structure) even when they are. In the first case, where other countries are not at first themselves charging such a tax, imposing the carbon tax on such imports will generate revenues which would be distributed to the US population. This would provide a strong incentive for those other countries to join the US and start to charge a similar carbon tax. And such a border adjustment for the carbon tax would be compliant with WTO rules on trade, as the tax would simply be ensuring that imported goods are being taxed the same as their domestic equivalents are (just as is true for a value-added tax). This is not discrimination against imports, but rather equal treatment.

In the second case, where trading partners are themselves all charging a similar carbon tax (let’s assume), the US would still come out ahead in carbon tax revenues due to our trade structure. US imports of goods are about 50% higher than its exports of goods, and it is primarily in the production of goods that GHGs are emitted. Partially offsetting this in the overall trade balance, US exports of services are about 50% higher than its imports of services. But services are a smaller share of trade, plus services are not as intensive as goods in the GHGs emitted. Overall, the US has a current account deficit (more imports of goods and services than exports), matched by capital inflows being invested in the US. With such a trade structure, the carbon taxes charged on imports will substantially exceed whatever is rebated on exports. The US population would come out ahead. Put another way, producers of goods being sold in the US are currently being provided a subsidy by not charging them for the cost we are incurring due to the greenhouse gases being emitted in their production. Given the US trade structure, a substantial share of this subsidy is going to foreign producers. A tax on such GHG emissions is simply the removal of this subsidy.

C. Price Impacts, and the Viability of Clean Alternatives

Applying the carbon tax will lead producers to raise their prices if they do not otherwise adjust their processes. For transportation fuels, for example, the Treasury analysis estimated that at $49 per ton of CO2 (and its equivalent for other GHGs), the tax would equal 44 cents per gallon for gasoline, or 50 cents per gallon for diesel fuel. While significant, such increases are not huge. There have been far greater fluctuations in such fuel prices in recent years in response to the price of crude oil rising or falling, and consumers and the economy have been able to accommodate such changes.

More broadly, and expressed in terms of percentage increases, the Treasury analysts estimated that if the cost increases from the carbon tax were all fully passed along, the price of gasoline would rise by 11.8%, home heating oil by 12.4%, and air transportation by 7.5%. The price of natural gas would go up by 27.0% and the price of electricity by 16.9%, but note these are the prices of just the energy alone. The delivered price to our homes also includes distribution and other charges. For natural gas, for example, the energy component of my bill (in Washington, DC) was just 44% of my total bill over the last 12 months, so a 27% increase in the wholesale cost of natural gas would mean a 15% increase in my overall bill for gas. There would be no reason for distribution and other such charges to go up by any significant amount, as their costs depend on the volume delivered and not on the wholesale cost of the gas being delivered (and similarly for electricity). Overall, the Treasury analysis forecasts that prices in general would go up by 2.6% if the new carbon tax (at $49 per ton of CO2) were fully passed forward.

But the higher costs would provide incentives both to producers to change how they make things, and to consumers to take into account the total costs in their decisions on what to buy. One would see this most importantly (given its share as a source of GHG emissions) in how electricity is produced. Generating electricity by the burning of fossil fuels is now heavily subsidized, in effect, as nothing is charged for the cost of the damage done (hurricanes and other severe weather events, and more) by the resulting GHG emissions. But even with such subsidies going to those who burn fossil fuels, solar and wind produced power is now competitive (even without the subsidies going to solar and wind – see below) for newly built power plants, and indeed has been for some years. See the careful analysis of the relative costs that is undertaken annually by Lazard (see here for their November 2017 report). Indeed, Lazard found in its 2017 analysis that at current costs, utility-scale solar and wind generation is now often cheaper than just the operating costs of coal or nuclear plants, thus encouraging such substitution even when the capital costs of coal and nuclear plants are treated as a sunk cost.

Furthermore, solar and wind technology is still developing, with costs falling rapidly, while at this point the further reduction in costs in traditional power generation is slow. Lazard estimates the levelized cost of energy production at a new installation (in terms of dollars of overall costs, including capital costs, per megawatt hour of electricity generated, and excluding explicit subsidies on renewables) fell by 72% between 2009 and 2017 for utility-scale solar installations and by 47% for wind generation (to prices of $50 and $45 per megawatt hour, for solar and wind respectively; this is equivalent to 5 cents and 4.5 cents per kilowatt hour). In contrast, the cost for power generated by coal fell by just 8% over this period (to $102 per megawatt hour) and by 28% for natural gas (to $60). And the full levelized cost for nuclear power generation actually rose by 20% over the period (to $148).

There is, of course, wide variability in the cost of solar and wind across the country, depending on local conditions. Existing coal and nuclear plants are also of various ages and efficiencies, and hence also of varying costs. Thus overall averages tell only part of the story. The cost competitiveness (on average) of new installations does not mean that all new installations will be solar or wind, much less that all generation would or could shift immediately. But the now competitive costs have led to a bit over 50% of all new generation capacity built in the US over the last 10 years (2007 to 2016) to come from installations of solar, wind, or other renewables (with most of the solar coming only in the second half of that period).

No transition will be instantaneous, but should a significant carbon tax be imposed (of $40 or $49, for example), one should see an acceleration in the pace of such substitution of renewables for fossil fuels. And with such substitution, the impact on higher power prices will be limited in time, and should soon decline.

The other major user of fossil fuels is transportation, and here one sees a similar dynamic. Electric battery powered cars are now either competitive in cost or close to it (depending on how one values other attributes, such as better performance and inherently easier maintenance), and a carbon tax will accelerate the transition to such vehicles. And battery-powered vehicles are not just limited to cars. Tesla has announced plans to produce heavy trucks powered by batteries, with a range of up to 500 miles on a charge. Costs would be more than competitive with traditional fueled heavy trucks, and a substantial number of pre-orders have indeed already come in from owners of large trucking fleets. There is an interest at least in trying this. And with battery-powered heavy trucks possible, the same is true for full-size buses.

Again, starting to charge for the costs borne by society from the CO2 and other GHGs emitted in transportation would accelerate the shift to less polluting vehicles. It won’t happen overnight. But that shift will limit the extent and duration of higher costs stemming from charging a carbon tax.

And while such a tax alone will not lead to zero GHG emissions with current technologies available, it would be a giant step in that direction. It would also provide a strong incentive to develop the technologies that would carry this further and at a lower cost.

D. Distributional Implications

Finally and importantly, the funds collected by the carbon tax would be fully rebated to all Americans, with the same amount rebated per person. The Treasury analysis estimated that at $49 per ton of CO2 in 2019, the carbon tax would collect funds sufficient to provide a rebate of $583 per person (for the year), or $2,332 for a family of four. The rebate could be provided annually or quarterly, or even monthly, and through the IRS or Social Security.

The rebates would also be distributionally positive. The poor would indeed benefit on a net basis. Being poor, they do not consume that much, and thus do not account for a high share of GHG emissions. The rich, in contrast, not only consume more (they are rich, and can afford more), but the products they buy are also more polluting in greenhouse gases (big gas-guzzling cars rather than small fuel-efficient ones; jet travel for vacations but not public transit; large homes kept heated and air-conditioned rather than smaller homes and apartments; etc.). Thus the rich will receive back less than what is paid in carbon taxes on the goods they consume, while the poor will receive back more. Furthermore, because the poor are poor, a given dollar amount rebated to them will be a higher percentage of their (low) incomes, than the same dollar amount would be (in percentage terms) for the rich.

The impacts are significant. The Treasury analysis (based on data they use for their tax simulation models) concluded that the impacts by family income decile would be:

|

Net Impact on Income from $49 per ton Carbon Tax, with $583 per Person Rebate, by Family Decile |

|

Decile |

% of Income |

|

0 to 10 |

+8.9% |

|

10 to 20 |

+4.7% |

|

20 to 30 |

+3.1% |

|

30 to 40 |

+2.0% |

|

40 to 50 |

+1.2% |

|

50 to 60 |

+0.6% |

|

60 to 70 |

+0.1% |

|

70 to 80 |

-0.3% |

|

80 to 90 |

-0.7% |

|

90 to 100 |

-1.0% |

Families are ranked here by income decile, so the first decile (0 to 10%) is made up of the 10% of families (in number) who have the lowest incomes, the second decile (10 to 20%) is made up of the 10% of families with the next lowest incomes, and so on, up to the richest 10% of families (90 to 100%).

The results indicate that on a net basis (i.e. after taking account of the higher prices that would be paid on goods purchased, reflecting the carbon tax at $49 per ton), the lowest income decile families would see an increase in their real incomes of 8.9% following the $583 per person rebate. This is quite substantial. And the analysis found there would be a similar, positive, gain for all families up through the 7th decile, although at diminishing shares of their income. The top 3 deciles would end up paying more on a net basis, due to their greater purchases of goods where greenhouse gases are emitted (both in total amount and in the mix of their goods). But the net cost reaches just 1% of incomes for the richest decile. It is only a small share in part because their incomes are of course the highest. This tax is not unaffordable.

E. Conclusion

To conclude, imposing a carbon tax is administratively practical, would bring prices and costs in line with the costs being borne by society when greenhouse gases are emitted, and even with current technologies would lead to a significant shift away from processes that are warming our planet. It is a fundamental confusion to assert, as Trump and others have done, that “we cannot afford it”. That is nonsense: We are paying the costs already (in an increased frequency of severe weather events, in droughts in some areas and floods in others, and other such impacts), and they will get far worse if nothing is done. Furthermore, such a carbon tax would not reduce our competitiveness when applied equally to imported items (and rebated for exports). Indeed, with our current trade structure, the US would come out ahead financially by starting to charge for GHG emissions.

Such a tax also would be distributionally highly progressive, as the poor would come well ahead on a net basis with the revenues collected being rebated back to the population. Indeed, it is estimated that the bottom 70% of the population would come out ahead on a net basis. And while the rich would end up paying more, reflecting their greater consumption and the GHG intensity of the goods they buy, this would come just to 1% of the incomes of the richest 10% of the population.

Such a tax on GHG emissions would be the final component of what a comprehensive tax reform really should have looked like. As discussed in the preceding posts on this blog, there should have been a reform to simplify corporate and individual income taxes (with all sources of income taxed similarly), plus action taken on Social Security taxes to ensure the system will be sustained for the foreseeable future. None of this was done. Nor was any action taken to address climate change, where the subsidy we are implicitly providing fossil fuels and other sources of greenhouse gas emissions (by not charging for the damage being done as a result of those emissions) could have been addressed by a tax on such emissions.

This is not surprising, unfortunately. There are important vested interests in the fossil fuel industries (coal, oil, and gas) that benefit from not being charged for the damage their fuels are causing. As a rationalization of this, Trump and much of the Republican Party continue to deny that climate change even exists. But the result will be that the damage being done, already large, will grow over time. Plus, once the doubters do finally recognize it, the actions that will then need to be taken will be more costly and disruptive than if action were taken now.

As discussed above, there is no practical or special administrative difficulty to addressing the climate change problem now. It would be straightforward to implement a tax on GHG emissions. And the sooner this is done, the better.

You must be logged in to post a comment.