A. Introduction

Economists have long recommended taxing pollution as an effective as well as efficient way to achieve societal aims to counter that pollution. What is commonly called a “carbon tax”, but which in fact would apply to all emissions of greenhouse gases (where carbon dioxide, CO2, is the largest contributor), would do this. “Cap and trade” schemes, where polluters are required to acquire and pay for a limited number of permits, act similarly. The prime example in the US of such a cap and trade scheme was the program to sharply reduce the sulfur dioxide (SO2) pollution from the burning of coal in power plants. That program was launched in 1995 and was a major success. Not only did the benefits exceed the costs by a factor of 14 to 1 (with some estimates even higher – as much as 100 to 1), but the cost of achieving that SO2 reduction was only one-half to one-quarter of what officials expected it would have cost had they followed the traditional regulatory approach.

Cost savings of half or three-quarters are not something to sneer at. Reducing greenhouse gas emissions, which is quite possibly the greatest challenge of our times, will be expensive. The benefits will be far greater, so it is certainly worthwhile to incur those expenses (and it is just silly to argue that “we cannot afford it” – the benefits far exceed the costs). One should, however, still want to minimize those costs.

But while such cost savings are hugely important, one should also not ignore the distributional consequences of any such plan. These are a concern of many, and rightly so. The poor should not be harmed, both because they are poor and because their modest consumption is not the primary cause of the pollution problem we are facing. But this is where there has been a good deal of confusion and misunderstanding. A tax on all greenhouse gas emissions, with the revenue thus generated then distributed back to all on an equal per capita basis, would be significantly beneficial to the poor in purely financial terms. Indeed it would be beneficial to most of the population since it is a minority of the population (mostly those who are far better off financially than most) who account for a disproportionate share of emissions.

A specific carbon tax plan that would work in this way was discussed in an earlier post on this blog. I would refer the reader to that earlier post for the details on that plan. But briefly, under this proposal all emissions of greenhouse gases (not simply from power plants, but from all sources) would pay a tax of $49 per metric ton of CO2 (or per ton of CO2 equivalent for other greenhouse gases, such as methane). A fee of $49 per metric ton would be equivalent to about $44.50 per common ton (2,000 pounds, as commonly used in the US but nowhere else in the world). The revenues thus generated would then be distributed back, in full, to the entire population in equal per capita terms, on a monthly or quarterly basis. There would also be a border-tax adjustment on goods imported, which would create the incentive for other countries to join in such a scheme (as the US would charge the same carbon tax on such goods when the source country hadn’t, but with those revenues then distributed to Americans).

The US Treasury published a study of this scheme in January 2017, and estimated that such a tax would generate $194 billion of revenues in its initial year (which was assumed to be 2019). This would allow for a distribution of $583 to every American (man, woman, and child – not just adults). Furthermore, the authors estimated what the impact would be by family income decile, and concluded that the bottom 7 deciles of families (the bottom 70%, as ranked by income) would enjoy a net benefit, while only the richest 30% would pay a net cost.

That distributional impact will be the focus of this blog post. It has not received sufficient attention in the discussion on how to address climate change. While the Treasury study did provide estimates on what the impacts by income decile would be (although not always in an easy to understand form), views on a carbon tax often appear to assume, incorrectly, that the poor will pay the most as a share of their income, while the rich will be able to get away with avoiding the tax. The impact would in fact be the opposite. Indeed, while the primary aim of the program is, and should be, the reduction of greenhouse gas emissions, its redistributive benefits are such that on that basis alone the program would have much to commend it. It would also be just. As noted above, the poor do not account for a disproportionate share of greenhouse gas emissions – the rich do – yet the poor suffer similarly, if not greater, from the consequences.

This blog post will first review those estimated net cash benefits by family income decile, both in dollar amounts and as a share of income. To give a sense of how important this is in magnitude, it will then examine how these net benefits compare to the most important current cash transfer program in the US – food stamp benefits. Finally, it will briefly review the politics of such a program. Perceptions have, unfortunately, been adverse, and many pundits believe a carbon tax program would never be approved. Perhaps this might change if news sources paid greater attention to the distribution and economic justice benefits.

B. Net Benefits or Costs by Family Income Decile from a Carbon Tax with Redistribution

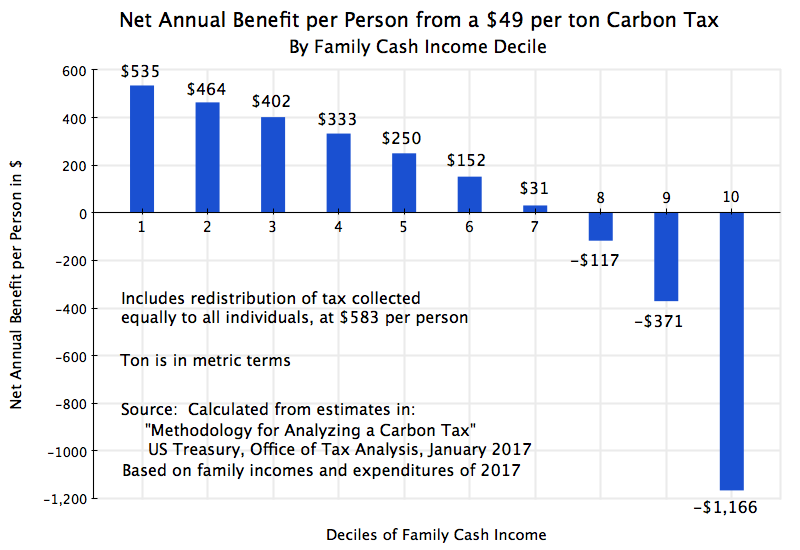

The chart at the top of this post shows what the average net impact would be in dollars per person, by family cash income decile, if a carbon tax of $49 per metric ton were charged with the revenues then distributed on an equal per capita basis. While prices of energy and other goods whose production or use leads to greenhouse gas emissions would rise, the revenues from the tax thus generated would go back in full to the population. Those groups who account for a less than proportionate share of greenhouse gas emissions (the poor and much of the middle class) would come out ahead, while those with the income and lifestyle that lead to a greater than average share of greenhouse gas emissions (the rich) will end up paying in more.

The figures are derived from estimates made by the staff of the US Treasury – staff that regularly undertake assessments of the incidence across income groups of various tax proposals. The study was published in January 2017, and the estimates are of what the impacts would have been had the tax been in place for 2019. The results were presented in tables following a standard format for such tax incidence studies, with the dollars per person impact of the chart above derived from those tables.

To arrive at these estimates, the Treasury staff first calculated what the impact of such a $49 per metric ton carbon tax would be on the prices of goods. Such a tax would, for example, raise the price of gasoline by $0.44 per gallon based on the CO2 emitted in its production and when it is burned. Using standard input-output tables they could then estimate what the price changes would be on a comprehensive set of goods, and based on historic consumption patterns work out what the impacts would be on households by income decile. The net impact would then follow from distributing back on an equal per capita basis the revenues collected by the tax. For 2019, the Treasury staff estimated $194 billion would be collected (a bit less than 1% of GDP), which would allow for a transfer back of $583 per person.

Those in the poorest 10% of households would receive an estimated $535 net benefit per person from such a scheme. The cost of the goods they consume would go up by $48 per person over the course of a year, but they would receive back $583. They do not account for a major share of greenhouse gas emissions because they cannot afford to consume much. They are poor, and a family earning, say, $20,000 a year consumes far less of everything than a family earning $200,000 a year. In terms of greenhouse gas emissions implicit in the Treasury numbers, the poorest 10% of Americans account only for a bit less than 1.0 metric tons of CO2 emissions per person per year (including the CO2 equivalent in other greenhouse gases). The richest 10% account for close to 36 tons CO2 equivalent per person per year.

As one goes from the lower income deciles to the higher, consumption rises and CO2 emissions from the goods consumed rises. But it is not a linear trend by decile. Rather, higher-income households account for a more than proportionate share of greenhouse gas emissions. As a consequence, the break-even point is not at the 50th percentile of households (as it would be if the trend were linear), but rather something higher. In the Treasury estimates, households up through the 70th percentile (the 7th decile) would on average still come out ahead. Only the top three deciles (the richest 30%) would end up paying more for the carbon tax than what they would receive back. But this is simply because they account for a disproportionately high share of greenhouse gas emissions. It is fully warranted and just that they should pay more for the pollution they cause.

But it is also worth noting that while the richer household would pay more in dollar terms than they receive back, those higher dollar amounts are modest when taken as a share of their high incomes:

In dollar terms the richest 10% would pay in a net $1,166 per person in this scheme, as per the chart at the top of this post. But this would be just 1.0% of their per-person incomes. The 9th decile (families in the 80 to 90th percentile) would pay in a net of 0.7% of their incomes, and the 8th decile would pay in a net of 0.3%. At the other end of the distribution, the poorest 10% (the 1st decile) would receive a net benefit equal to 8.9% of their incomes. This is not minor. The relatively modest (as a share of incomes) net transfers from the higher-income households permit a quite substantial rise (in percentage terms) in the incomes of poorer households.

C. A Comparison to Transfers in the Food Stamps Program

The food stamps program (formally now called SNAP, for Supplemental Nutrition Assistance Program) is the largest cash income transfer program in the US designed specifically to assist the poor. (While the cost of Medicaid is higher, those payments are made directly to health care providers for their medical services to the poor.) How would the net transfers under a carbon tax with redistribution compare to SNAP? Are they in the same ballpark?

I had expected they would not be close. However, it turns out that they are not that far apart. While food stamps would still provide a greater transfer for the very poorest households, the supplement to income that those households would receive by such a carbon tax scheme would be significant. Furthermore, the carbon tax scheme would be of greater benefit than food stamps are, on average, for lower middle-class households (those in the 3rd decile and above).

The Congressional Budget Office (CBO) has estimated how food stamp (SNAP) benefits are distributed by household income decile. While the forecast year is different (2016 for SNAP vs. 2019 for the carbon tax), for the purposes here the comparison is close enough. From the CBO figures one can work out the annual net benefits per person under SNAP for households in the 1st to 4th deciles (with the 5th through the 10th deciles then aggregated by the CBO, as they were all small):

The average annual benefits from SNAP were estimated to be about $1,500 per person for households in the poorest decile and $690 per person in the 2nd decile. These are larger than the estimated net benefits of these two groups under a carbon tax program (of $535 and $464 per person, respectively), but it was surprising, at least to me, that they are as close as they are. The food stamp program is specifically targeted to assist the poor to purchase the food that they need. A carbon tax with redistribution program is aimed at cutting back greenhouse gas emissions, with the funds generated then distributed back to households on an equal per capita basis. They have very different aims, but the redistribution under each is significant.

D. But the Current Politics of Such a Program Are Not Favorable

A carbon tax with redistribution program would therefore not only reduce greenhouse gas emissions at a lower cost than traditional approaches, but would also provide for an equitable redistribution from those who account for a disproportionate share of greenhouse gas emissions (the rich) to those who do not (the poor). But news reporters and political pundits, including those who are personally in favor of such a program, consider it politically impossible. And in what was supposed to be a personal email, but which was part of those obtained by Russian government hackers and then released via WikiLeaks in order to assist the Trump presidential campaign, John Podesta, the senior campaign manager for Hillary Clinton, wrote: “We have done extensive polling on a carbon tax. It all sucks.”

Published polls indicate that the degree of support or not for a carbon tax program depends critically on how the question is worded. If the question is stated as something such as “Would you be in favor of taxing corporations based on their carbon emissions”, polls have found two-thirds or more of Americans in support. But if the question is worded as something such as “Would you be in favor of paying a carbon tax on the goods you purchase”, the support is less (often still more than a majority, depending on the specific poll, but less than two-thirds). But they really amount to the same thing.

There are various reasons for this, starting with that the issue is a complex one, is not well understood, and hence opinions can be easily influenced based on how the issue is framed. This opens the field to well-funded vested interests (such as the fossil fuel companies) being able to influence votes by sophisticated advertising. Opponents were able to outspend proponents by 2 to 1 in Washington State in 2018, when a referendum on a proposed carbon tax was defeated (as it had been also in 2016). Political scientists who have studied the two Washington State referenda believe they would be similarly defeated elsewhere.

There appear to be two main concerns: The first is that “a carbon tax will hurt the poor”. But as examined above, the opposite would be the case. The poor would very much benefit, as their low consumption only accounts for a small share of carbon emissions (they are poor, and do not consume much of anything), but they would receive an equal per capita share of the revenues raised.

In distinct contrast, but often not recognized, a program to reduce greenhouse gas emissions based on traditional regulation would still see an increase in costs (and indeed likely by much more, as noted above), but with no compensation for the poor. The poor would then definitely lose. There may then be calls to add on a layer of special subsidies to compensate the poor, but these rarely work well.

The second concern often heard is that “a carbon tax is just a nudge” and in the end will not get greenhouse gas emissions down. There may also be the view (internally inconsistent, but still held) that the rich are so rich that they will not cut back on their consumption of high carbon-emission goods despite the tax, while at the same time the rich can switch their consumption (by buying an electric car, for example, to replace their gasoline one) while the poor cannot.

But the prices do matter. As noted at the start of this post, the experience with the cap and trade program for SO2 from the burning of coal (where a price is put on the SO2 emissions) found it to be highly effective in bringing SO2 emissions down quickly. Or as was discussed in an earlier post on this blog, charging polluters for their emissions would be key to getting utilities to switch use to clean energy sources. The cost of both solar and wind new generation power capacity has come down sharply over the past decade, to the point where, for new capacity, they are the cheapest sources available. But this is for new generation. When there is no charge for the greenhouse gases emitted, it is still cheaper to keep burning gas and often coal in existing plants, as the up-front capital costs have already been incurred and do not affect the decision of what to use for current generation. But as estimated in that earlier post, if those plants were charged $40 per ton for their CO2 emissions, it would be cheaper for the power utilities to build new solar or wind plants and use these to replace existing fossil fuel plants.

There are many other substitution possibilities as well, but many may not be well known when the focus is on a particular sector. For example, livestock account for about 30% of methane emissions resulting from human activity. This is roughly the same share as methane emissions from the production and distribution of fossil fuels. And methane is a particularly potent greenhouse gas, with 86 times the global warming potential over a 20-year horizon of an equal weight of CO2. Yet a simple modification of the diets of cows will reduce their methane emissions (due to their digestive system – methane comes out as burps and farts) by 33%. One simply needs to add to their feed just 100 grams of lemongrass per day and the digestive chemistry changes to produce far less methane. Burger King will now start to purchase its beef from such sources.

This is a simple and inexpensive change, yet one that is being done only by Burger King and a few others in order to gain favorable publicity. But a tax on such greenhouse gas emissions would induce such an adjustment to the diets of livestock more broadly (as well as research on other dietary changes, that might lead to an even greater reduction in methane emissions). A regulatory focus on emissions from power plants alone would not see this. One might argue that a broader regulatory system would cover emissions from such agricultural practices, and in principle it should. But there has been little discussion of extending the regulation of greenhouse gas emissions to the agricultural sector.

More fundamentally, regulations are set and then kept fixed over time in order to permit those who are regulated to work out and then implement plans to comply. Such systems are not good, by their nature, at handling innovations, as by definition innovations are not foreseen. Yet innovations are precisely what one should want to encourage, and indeed the ex-post assessment of the SO2 emissions trading program found that it was innovations that led to costs being far lower than had been anticipated. A carbon tax program would similarly encourage innovations, while regulatory schemes can not handle them well.

There may well be other concerns, including ones left unstated. Individuals may feel, for example, that while climate change is indeed a major issue and needs to be addressed, and that redistribution under a carbon tax program might well be equitable overall, that they will nonetheless lose. And some will. Those who account for a disproportionately high share of greenhouse gas emissions through the goods they purchase will end up paying more. But costs will also rise under the alternative of a regulatory approach (and indeed rise by a good deal more), which will affect them as well. If they do indeed account for a disproportionately high share of greenhouse gas emissions, they should be especially in favor of an approach that would bring these emissions down at the lowest possible cost. A scheme that puts a price on carbon emissions, such as in a carbon tax scheme, would do this at a lower cost than traditional approaches.

So while many have concerns with a carbon tax with redistribution scheme, much of this is due to a misunderstanding of what the impacts would be, as well as of what the impacts would be of alternatives. One sees this in the range of responses to polling questions on such schemes, where the degree of support depends very much on how the questions are worded or framed. There is a need to explain better how a carbon tax with redistribution program would work, and we have collectively (analysts, media, and politicians) failed to do this.

There are also some simple steps one can take which would likely increase the attractiveness of such a program. For example, perceptions would likely be far better if the initial rebate checks were sent up-front, before the carbon taxes were first to go into effect, rather than later, at the end of whatever period is chosen. Instead of households being asked to finance the higher costs over the period until they received their first rebate checks, one would have the government do this. This would not only make sense financially (government can fund itself more cheaply than households can), but more important, politically. Households would see up-front that they are, indeed, receiving a rebate check before the prices go up to reflect the carbon tax.

And one should not be too pessimistic. While polling responses depend on the precise wording used, as noted above, the polling results still usually show a majority in support. But the issue needs to be explained better. There are problems, clearly, when issues such as the impact on the poor from such a scheme are so fundamentally misunderstood.

E. Conclusion

Charging for greenhouse gases emitted (a carbon tax), with the revenues collected then distributed back to the population on an equal per capita basis, would be both efficient (lower cost) and equitable. Indeed, the transfers from those who account for an especially high share of greenhouse gas emissions (the rich) to those who account for very little of them (the poor), would provide a significant supplement to the incomes of the poor. While the redistributive effect is not the primary aim of the program (reducing greenhouse gases is), that redistributive effect would be both beneficial and significant. It should not be ignored.

The conventional wisdom, however, is that such a scheme could not command a majority in a referendum. The issue is complex, and well-funded vested interests (the fossil fuel companies) have been able to use that complexity to propagate a sufficient level of concern to defeat such referenda. The impact on the poor has in particular been misportrayed.

But climate change really does need to be addressed. One should want to do this at the lowest possible cost while also in an equitable manner. Hopefully, as more learn what carbon tax schemes can achieve, politicians will obtain the support they need to move forward with such a program.

You must be logged in to post a comment.