A. Introduction

Since World War II, the US has never run such high fiscal deficits in times of full employment as it will now. With the tax cuts pushed through by the Republican Congress and signed into law by Trump in December, and to a lesser extent the budget passed in March, it is expected that the US will soon be running a fiscal deficit of over $1.0 trillion a year, exceeding 5% of GDP. This is unprecedented.

We now have good estimates of how high the deficits will grow under current policy and in a scenario which assumes (optimistically) that the economy will remain at full employment, with no downturn. The Congressional Budget Office (CBO) published on April 9 its regular report on “The Budget and Economic Outlook”, this year covering fiscal years 2018 to 2028. In this report to Congress and to the public, the CBO assesses the implications of federal budget and tax policy, as set out under current law. The report normally comes out in January or February of each year but was delayed this year in order to reflect the tax bill approved in December and also the FY18 budget, which was only approved in March (even though the fiscal year began last October).

The forecast is that the deficits will now balloon. This should not be a surprise given the magnitude of the tax cuts pushed through Congress in December and then signed into law by Trump, but recall that the Republicans pushing through the tax bill asserted deficits would not increase as a result. The budget approved in March also provides for significant increases in legislated spending – especially for the military but also for certain domestic programs. But as will be discussed below, government spending (other than on interest) over the next decade is in fact now forecast by the CBO to be less than what it had forecast last June.

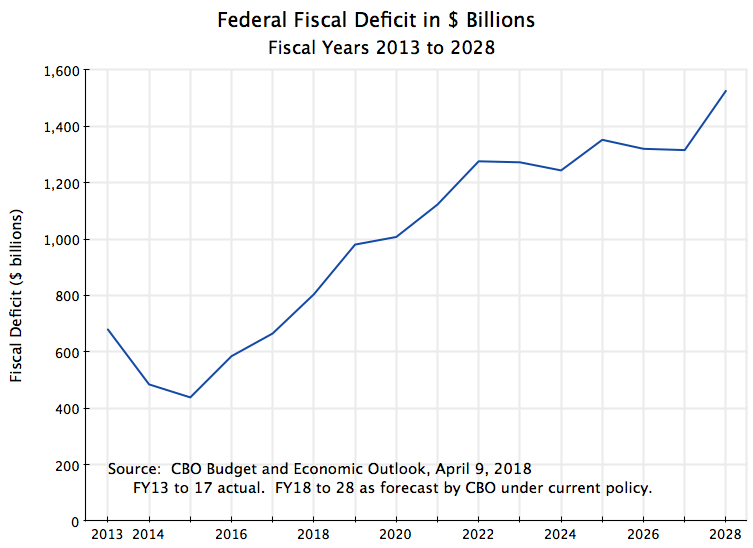

The CBO assessment is the first set of official estimates of what the overall impact will be. And they are big. The CBO forecasts that even though the economy is now at full employment (and assumed to remain there for the purposes of the scenario used), deficits are forecast to grow to just short of $1 trillion in FY2019, and then continue to increase, reaching over $1.5 trillion by FY2028. In dollar terms, it has never been that high – not even in 2009 at the worst point in the recession following the 2008 collapse of the economy.

That is terrible fiscal policy. While high fiscal deficits are to be expected during times of high unemployment (as tax revenues are down, while government spending is the only stabilizing element for the economy when both households and corporations are cutting back on spending due to the downturn), standard policy would be to limit deficits in times of full employment in order to bring down the public debt to GDP ratio. But with the tax cuts and spending plans this is not going to happen under Trump, even should the economy remain at full employment. And it will be far worse when the economy once again dips into a recession, as always happens eventually.

This blog post will first discuss the numbers in the new CBO forecasts, then the policy one should follow over the course of the business cycle in order to keep the public debt to GDP under control, and finally will look at the historical relationship between unemployment and the fiscal deficit, and how the choices made on the deficit by Trump and the Republican-controlled Congress are unprecedented and far from the historical norms.

B. The CBO Forecast of the Fiscal Deficits

The forecasts made by the CBO of the fiscal accounts that would follow under current policies are always eagerly awaited by those concerned with what Congress is doing. Ten-year budget forecasts are provided by the CBO at least annually, and typically twice or even three times a year, depending on the decisions being made by Congress.

The CBO itself is non-partisan, with a large professional staff and a director who is appointed to a four-year term (with no limits on its renewal) by the then leaders in Congress. The current director, Keith Hall, took over on April 1, 2015, when both the House and the Senate were under Republican control. He replaced Doug Elmensdorf, who was widely respected as both capable and impartial, but who had come to the end of a term. Many advocated that he be reappointed, but Elmensdorf had first taken the position when Democrats controlled the House and the Senate. Hall is a Republican, having served in senior positions in the George W. Bush administration, and there was concern that his appointment signaled an intent to politicize the position.

But as much as his party background, a key consideration appeared to have been Hall’s support for the view that tax cuts would, through their impact on incentives, lead to more rapid growth, with that more rapid growth then generating more tax revenue which would partially or even fully offset the losses from the lower tax rates. I do not agree. An earlier post on this blog discussed that that argument is incomplete, and does not take into account that there are income as well as substitution effects (as well as much more), which limit or offset what the impact might be from substitution effects alone. And another post on this blog looked at the historical experience after the Reagan and Bush tax cuts, in comparison to the experience after the (more modest) increases in tax rates on higher income groups under Clinton and Obama. It found no evidence in support of the argument that growth will be faster after tax cuts than when taxes are raised. What the data suggest, rather, is that there was little to no impact on growth in one direction or the other. Where there was a clear impact, however, was on the fiscal deficits, which rose with the tax cuts and fell with the tax increases.

Given Hall’s views on taxes, it was thus of interest to see whether the CBO would now forecast that an acceleration in GDP growth would follow from the new tax cuts sufficient to offset the lower tax revenues following from the lower tax rates. The answer is no. While the CBO did forecast that GDP would be modestly higher as a result of the tax cuts (peaking at 1.0% higher than would otherwise be the case in 2022 before then diminishing over time, and keep in mind that these are for the forecast levels of GDP, not of its growth), this modestly higher GDP would not suffice to offset the lower tax revenues following from the lower tax rates.

Taking account of all the legislative changes in tax law since its prior forecasts issued in June 2017, the CBO estimated that fiscal revenues collected over the ten years FY2018 to FY2027 would fall by $1.7 trillion from what it would have been under previous law. However, after taking into account its forecast of the resulting macroeconomic effects (as well as certain technical changes it made in its forecasts), the net impact would be a $1.0 trillion loss in revenues. This is almost exactly the same loss as had been estimated by the staff of the Joint Committee on Taxation for the December tax bill, which also factored in an estimate of a (modest) impact on growth from the lower tax rates.

Fiscal spending projections were also provided, and the CBO estimated that legislative changes alone (since its previous estimates in June 2017) would raise spending (excluding interest) by $450 billion over the ten year period. However, after taking into account certain macro feedbacks as well as technical changes in the forecasts, the CBO is now forecasting government spending will in fact be $100 billion less over the ten years than it had forecast last June. The higher deficits over those earlier forecast are not coming from higher spending but rather totally from the tax cuts.

Finally, the higher deficits will have to be funded by higher government borrowing, and this will lead to higher interest costs. Interest costs will also be higher as the expansionary fiscal policy at a time when the economy is already at full employment will lead to higher interest rates, and those higher interest rates will apply to the entire public debt, not just to the increment in debt resulting from the higher deficits. The CBO forecasts that higher interest costs will add $650 billion to the deficits over the ten years.

The total effect of all this will thus be to increase the fiscal deficit by $1.6 trillion over the ten years, over what it would otherwise have been. The resulting annual fiscal deficits, in billions of dollars, would be as shown in the chart at top of this post. Under the assumed scenario that the economy will remain at full employment over the entire period, the fiscal deficit will still rise to reach almost $1 trillion in FY19, and then to over $1.5 trillion in FY28. Such deficits are unprecedented for when the economy is at full employment.

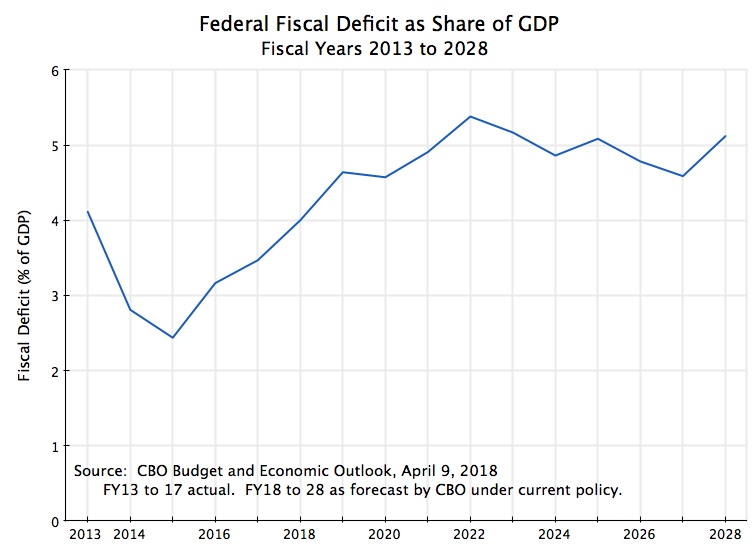

The deficits forecast would then translate into these shares of GDP, given the GDP forecasts:

The CBO is forecasting that fiscal deficits will rise to a range of 4 1/2 to 5 1/2% of GDP from FY2019 onwards. Again, this is unprecedented for the US economy in times of full employment.

C. Fiscal Policy Over the Course of the Business Cycle

As noted above, fiscal policy has an important role to play during economic downturns to stabilize conditions and to launch a recovery. When something causes an economic downturn (such as the decision during the Bush II administration not to regulate banks properly in the lead up to the 2008 collapse, believing “the markets” would do this best), both households and corporations will reduce their spending. With unemployment increasing and wages often falling even for those fortunate enough to remain employed, as well as with the heightened general concerns on the economy, households will cut back on their spending. Similarly, corporations will seek to conserve cash in the downturns, and will cut back on their spending both for the inputs they would use for current production (they cannot sell all of their product anyway) and for capital investments (their production facilities are not being fully used, so why add to capacity).

Only government can sustain the economy in such times, stopping the downward spiral through its spending. Fiscal stimulus is needed, and the Obama stimulus program passed early in his first year succeeded in pulling the economy out of the freefall it was in at the time of his inauguration. GDP fell at an astounding 8.2% annual rate in the fourth quarter of 2008 and was still crashing in early 2009 as Obama was being sworn in. It then stabilized in the second quarter of 2009 and started to rise in the third quarter. The stimulus program, as well as aggressive action by the Federal Reserve, accounts for this turnaround.

But fiscal deficits will be high during such economic downturns. While any stimulus programs will add to this, most of the increase in the deficits in such periods occur automatically, primarily due to lower tax revenues in the downturn. Incomes and employment are lower, so taxes due will be lower. There is also, but to a much smaller extent, some automatic increase in government spending during the downturns, as funds are paid out in unemployment insurance or for food stamps for the increased number of the poor. The deficits will then add to the public debt, and the public debt to GDP ratio will rise sharply (exacerbated in the short run by the lower GDP as well).

One confusion, sometimes seen in news reports, should be clarified. While fiscal deficits will be high in a downturn, for the reasons noted above, and any stimulus program will add further to those deficits, one should not equate the size of the fiscal deficit with the size of the stimulus. They are two different things. For example, normally the greatest stimulus, for any dollar of expenditures, will come from employing directly blue-collar workers in some government funded program (such as to build or maintain roads and other such infrastructure). A tax cut focused on the poor and middle classes, who will spend any extra dollar they receive, will also normally lead to significant stimulus (although probably less than via directly employing a worker). But a tax cut focused on the rich will provide only limited stimulus as any extra dollar they receive will mostly simply be saved (or used to pay down debt, which is economically the same thing). The rich are not constrained in how much they can spend on consumption by their income, as their income is high enough to allow them to consume as much as they wish.

Each of these three examples will add equally to the fiscal deficit, whether the dollar is used to employ workers directly, to provide a tax cut to the poor and middle classes, or to provide a tax cut to the rich. But the degree of stimulus per dollar added to the deficit can be dramatically different. One cannot equate the size of the deficit to the amount of stimulus.

Deficits are thus to be expected, and indeed warranted, in a downturn. But while the resulting increase in public debt is to be expected in such conditions, there must also come a time for the fiscal deficits to be reduced to a level where at least the debt to GDP ratio, if not the absolute level of the debt itself, will be reduced. Debt cannot be allowed to grow without limit. And the time to do this is when the economy is at full employment. It was thus the height of fiscal malpractice for the tax bills and budget passed by Congress and signed into law by Trump not to provide for this, but rather for the precise opposite. The CBO estimates show that deficits will rise rather than fall, even under a scenario where the economy is assumed to remain at full employment.

It should also be noted that the deficit need not be reduced all the way to zero for the debt to GDP ratio to fall. With a growing GDP and other factors (interest rates, the rate of inflation, and the debt to GDP ratio) similar to what they are now, a good rule of thumb is that the public debt to GDP ratio will fall as long as the fiscal deficit is around 3% of GDP or less. But the budget and tax bills of Trump and the Congress will instead lead to deficits of around 5% of GDP. Hence the debt to GDP ratio will rise.

[Technical note for those interested: The arithmetic of the relationship between the fiscal deficit and the debt to GDP ratio is simple. A reasonable forecast, given stated Fed targets, is for an interest rate on long-term public debt of 4% and an inflation rate of 2%. This implies a real interest rate of 2%. With real GDP also assumed to grow in the CBO forecast at 2% a year (from 2017 to 2028), the public debt to GDP ratio will be constant if what is called the “primary balance” is zero (as the numerator, public debt, will then grow at the same rate as the denominator, GDP, each at either 2% a year in real terms or 4% a year in nominal terms) . The primary balance is the fiscal deficit excluding what is paid in interest on the debt. The public debt to GDP ratio, as of the end of FY17, was 76.5%. With a nominal interest rate of 4%, this would lead to interest payments on the debt of 3% of GDP. A primary balance of zero would then imply an overall fiscal deficit of 3% of GDP. Hence a fiscal deficit of 3% or less, with the public debt to GDP ratio roughly where it is now, will lead to a steady debt to GDP ratio.

More generally, the debt to GDP ratio will be constant whenever the rate of growth of real GDP matches the real interest rate, and the primary balance is zero. In the case here, the growth in the numerator of debt (4% in nominal terms, or 2% in real terms when inflation is 2%) matches the growth in the denominator of GDP (2% in real terms, or 4% in nominal terms), and the ratio will thus be constant.]

Putting this in a longer-term context:

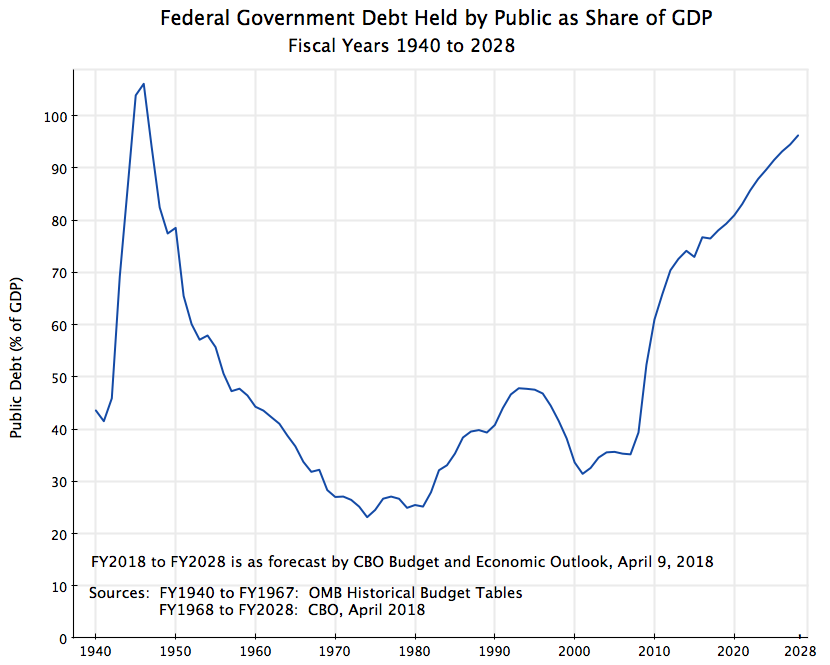

Federal government debt rose to over 100% of GDP during World War II. The war spending was necessary. But it did not then doom the US to perpetual economic stagnation or worse. Rather, fiscal deficits were kept modest, the economy grew well, and over the next several decades the debt to GDP ratio fell.

For the fiscal balances over this period (with fiscal deficits as negative and fiscal surpluses as positive):

Fiscal balances were mostly but modestly in deficit (and occasionally in surplus) through the 1950s, 60s, and 70s. The 3% fiscal deficit rule of thumb worked well, and one can see that as long as the fiscal deficit remained below 3% of GDP, the public debt to GDP ratio fell, to a low of 23% of GDP in FY1974. It then stabilized at around this level for a few years, but reversed and started heading in FY1982 after Reagan took office. And it kept going up even after the economy had recovered from the 1982 recession and the country was back to full employment, as deficits remained high following the Reagan tax cuts.

The new Clinton budgets, along with the tax increase passed in 1993, then stabilized the accounts, and the economy grew strongly. The public debt to GDP ratio, which had close to doubled under Reagan and Bush I (from 25% of GDP to 48%), was reduced to 31% of GDP by the year Clinton left office. But it then started to rise again following the tax cuts of Bush II (plus with the first of the two recessions under Bush II). And it exploded in 2008/2009, at the end of Bush II and the start of Obama, as the economy plunged into the worst economic downturn since the Great Depression.

The debt to GDP ratio did stabilize, however, in the second Obama term, and actually fell slightly in FY2015 (when the deficit was 2.4% of GDP). But with the deficits now forecast to rise to the vicinity of 5% of GDP (and to this level even with the assumption that there will not be an economic downturn at some point), the public debt to GDP ratio will soon be approaching 100% of GDP.

This does not have to happen. As noted above, one need not bring the fiscal deficits all the way down to zero. A fiscal deficit kept at around 3% of GDP would suffice to stabilize the public debt to GDP ratio, while something less than 3% would bring it down.

D. Historical Norms

What stands out in these forecasts is how much the deficits anticipated now differ from the historical norms. The CBO report has data on the deficits going back to FY1968 (fifty years), and these can be used to examine the relationship with unemployment. As discussed above, one should expect higher deficits during an economic downturn when unemployment is high. But these deficits then need to be balanced with lower deficits when unemployment is lower (and sufficiently low when the economy is at or near full employment that the public debt to GDP ratio will fall).

A simple scatter-plot of the fiscal balance (where fiscal deficits are a negative balance) versus the unemployment rate, for the period from FY1968 to now and then the CBO forecasts to FY2028, shows:

While there is much going on in the economy that affects the fiscal balance, this scatter plot shows a surprisingly consistent relationship between the fiscal balance and the rate of unemployment. The red line shows what the simple regression line would be for the historical years of FY1968 to FY2016. The scatter around it is surprisingly tight. [Technical Note: The t-statistic is 10.0, where anything greater than 2.0 is traditionally considered significant, and the R-squared is 0.68, which is high for such a scatter plot.]

An interesting finding is that the high deficits in the early Obama years are actually very close to what one would expect given the historical norm, given the unemployment rates Obama faced on taking office and in his first few years in office. That is, the Obama stimulus programs did not cause the fiscal deficits to grow beyond what would have been expected given what the US has had in the past. The deficits were high because unemployment was high following the 2008 collapse.

At the other end of the line, one has the fiscal surpluses in the years FY1998 to 2000 at the end of the Clinton presidency. As noted above, the public debt to GDP ratio stabilized soon after Clinton took office (in part due to the tax increases passed in 1993), with the fiscal deficits reduced to less than 3% of GDP. Unemployment fell to below 5% by mid-1997 and to a low of 3.8% in mid-2000, as the economy grew well. By FY1998 the fiscal accounts were in surplus. And as seen in the scatter plot above, the relationship between unemployment and the fiscal balance was close in those years (FY1998 to 2000) to what one would expect given the historical norms for the US.

But the tax cuts and budget passed by Congress and signed by Trump will now lead the fiscal accounts to a path far from the historical norms. Instead of a budget surplus (as in the later Clinton years, when the unemployment rate was similar to what the CBO assumes will hold for its scenario), or even a deficit kept to 3% of GDP or less (which would suffice to stabilize the debt to GDP ratio), deficits of 4 1/2 to 5 1/2 % of GDP are foreseen. The scatter of points for the fiscal deficit vs. unemployment relationship for 2018 to 2028 is in a bunch by itself, down and well to the left of the regression line. One has not had such deficits in times of full employment since World War II.

E. Conclusion

Fiscal policy is being mismanaged. The economy reached full employment by the end of the Obama administration, fiscal deficits had come down, and the public debt to GDP ratio had stabilized. There was certainly more to be done to bring down the deficit further, and with the aging of the population (retiring baby boomers), government expenditures (for Social Security and especially for Medicare and other health programs) will need to increase in the coming years. Tax revenues to meet such needs will need to rise.

But the Republican-controlled Congress and Trump pushed through measures that will do the opposite. Taxes have been cut dramatically (especially for corporations and rich households), while the budget passed in March will raise government spending (especially for the military). Even assuming the economy will remain at full employment with no downturn over the next decade (which would be unprecedented), fiscal deficits will rise to around 5% of GDP. As a consequence, the public debt to GDP ratio will rise steadily.

This is unprecedented. With the economy at full employment, deficits should be reduced, not increased. They need not go all the way to zero, even though Clinton was able to achieve that. A fiscal deficit of 3% of GDP (where it was in the latter years of the Obama administration) would stabilize the debt to GDP ratio. But Congress and Trump pushed through measures to raise the deficit rather than reduce it.

This leaves the economy vulnerable. There will eventually be another economic downturn. There always is one, eventually. The deficit will then soar, as it did in 2008/2009, and remain high until the economy fully recovers. But there will then be pressure not to allow the debt to rise even further. This is what happened following the 2010 elections, when the Republicans gained control of the House. With control over the budget, they were able to cut government spending even though unemployment was still high. Because of this, the pace of the recovery was slower than it need have been. While the economy did eventually return to full employment by the end of Obama’s second term, unemployment remained higher than should have been the case for several years as a consequence of the cuts.

At the next downturn, the fiscal accounts will be in a poor position to respond as they need to in a crisis. Public debt, already high, will soar to unprecedented levels, and there will be arguments from conservatives not to allow the debt to rise even further. Recovery will then be even more difficult, and many will suffer as a result.

You must be logged in to post a comment.