A. Introduction

Previous posts on this blog (including this older one from 2012) have discussed how the sluggish recovery from the 2008 economic collapse could have been avoided if one had allowed government spending to grow as it had during Reagan’s term. This post will look in more detail at what the resulting path for GDP would have been if government spending had followed the path as it had under Reagan, or even had simply been allowed to grow at its normal historical rate.

The 2008 collapse was of course not caused by fiscal actions, but rather by the bursting of the housing bubble, and its consequent impact both in bankrupting a large share of an overly-leveraged financial system and in causing household consumption to fall as many homeowners struggled to repay mortgages that were now greater than the value of their homes. Faced with the high unemployment resulting from this, an expansion of government spending would have supported the demand for output and hence for workers to produce that output. And initially, fiscal spending did indeed grow. This growth (along with aggressive action by the Fed) did succeed in turning around the steep slide of the economy that Obama faced as he took office. But since 2009 government spending has been cut back, and as a result the recovery of GDP has been by far the slowest in any cyclical downturn of the last four decades.

This blog post will look at alternative scenarios of what the recovery path of GDP could have been, had government spending not been reduced. Two primary alternatives will be examined. In the first, government spending is allowed to grow from the point President Obama took office at a rate equal to its average rate of growth over the period 1981 to 2008. In the second, government spending is allowed to grow from the onset of the recession (i.e. from the fourth quarter of 2007) at the same rate as it had during the Reagan years, following the downturn that began in the third quarter of 1981.

B. Government Spending Growth at the Historic Average Rate

In the first scenario, real government spending on goods and services (as measured in the GDP accounts, and inclusive of state and local government as well as federal) is allowed to grow at a rate of 2.24% per year. This is the average rate of growth for government spending over the 28 years from 1980 to 2008. This was a modest growth rate, and spanned the presidencies of three Republicans (Reagan and the two Bushes) for 20 of the 28 years, and one Democrat (Clinton) for 8 of the 28 years. The 2.24% growth rate was substantially below the growth rate of GDP of 3.04% over this same period (note this is for total GDP, not per capita). As a result, real GDP grew by over 50% more over this period than government spending did. But this modest pace of government spending growth was substantially more than the absolute fall in government spending during Obama’s term in office.

Note that this path for government spending is not some special rate faster than the historical average, as would normally be called for in a downturn when fiscal stimulus is needed because aggregate demand in the economy is less than what is needed for full employment. Rather, it is just the historical average rate. This should be seen as a neutral path, with government spending neither purposely stimulative, nor purposely contractionary.

This path for government spending is shown as the orange line in the following, where the path is superimposed on the graph presented in the earlier blog post of such paths of government spending in each of the downturns the US has faced since the 1970s:

Maintaining government spending growth at the historical 2.24% rate would have led to government spending well below that seen during the Reagan years (in the recoveries from the July 1981 and January 1980 downturns), roughly where it was in the recoveries from the November 1973 and March 2001 downturns, and well above where it was in the recoveries from the July 1990 downturn (during the Clinton years) and of course the December 2007 downturn (under Obama). Government spending in the current downturn (the brown curve in the graph) has fallen substantially during the period Obama has been in office.

The graph at the top of this post then shows what the GDP path would have been if government spending would have been allowed to grow at the historic average rate. The impact will depend on the multiplier. As was discussed in the earlier post on fiscal multipliers, the multiplier for the US in this period of high unemployment and short-term interest rates of close to zero will be relatively high. But for the purposes here, we will run scenarios of multipliers of 1.5, of 2.0, and of 2.5. This will span the range most economists would find reasonable for this period.

The results indicate that had one simply had government spending grow at its historic average rate, the economy would likely now be at or close to potential GDP, which is what GDP would be at full employment. But because of the fall in government spending since 2009 rather than this increase, current actual GDP is over 6% below potential GDP, and unemployment is high. (Potential GDP comes from the CBO estimates used in its May 2013 budget projections, but adjusted to reflect the methodological change made by the BEA in July 2013. Due to these adjustments, including for the GDP deflators used, the potential GDP path is not as “smooth” as one would normally see. But it will be close.)

Republicans have argued that we cannot, however, afford higher government spending, even if it would lead the economy back to full employment, as it would lead to an even higher public debt to GDP ratio. But as was discussed in a recent post on this blog on the arithmetic of the debt to GDP ratio, it is not necessarily the case that higher government spending will lead to a higher ratio. The Republican argument fails to recognize both that GDP will higher (due to the multiplier, and indeed a relatively high multiplier in the current conditions of high unemployment and close to zero short-term interest rates), and that a higher GDP will generate higher tax revenues due to that growth, which will off-set at least in part the impact on the deficit of the higher spending.

The resulting paths for the debt to GDP ratios by fiscal year, using a 30% marginal tax rate for the higher income, would be:

The impact of the higher government spending is to reduce the debt to GDP ratios over this period. The higher government spending leads to a higher GDP, and this higher GDP along with the extra tax revenues generated at the higher output means the debt rises by proportionately less. The ratios fall the most, as one would expect, the higher the multiplier. If one is truly concerned about the burden of the debt, one should be supportive of fiscal spending in this environment to bring the economy quickly back to full employment. The debt burden will then be less.

The debt to GDP ratios still rise over these years. This serves to point out that the assertion made by the Republicans that the public debt to GDP ratio has risen so much during Obama’s term due to explosive spending under Obama is simply nonsense. The debt to GDP ratios rose not due to higher government spending, but primarily due to the economic collapse and slow recovery, which has decimated tax revenues. With higher government spending, the debt to GDP ratios would have been lower.

C. Government Spending Growth at the Rate During the Reagan Years

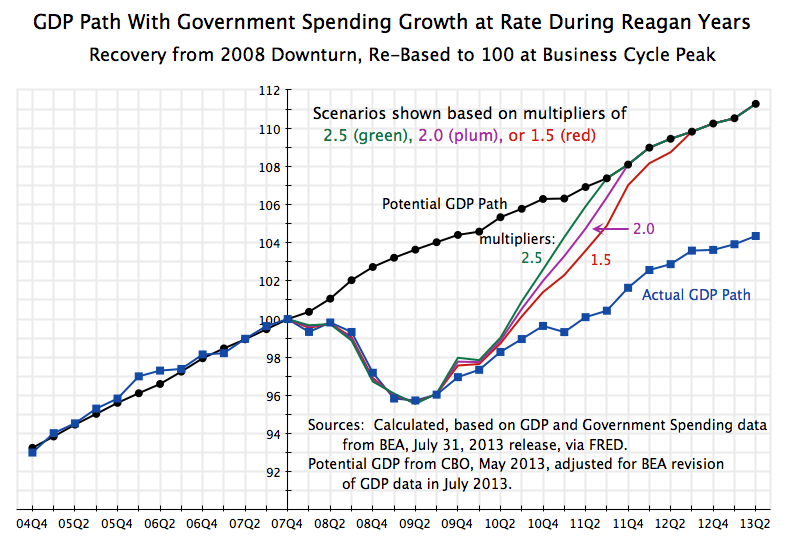

The second set of scenarios examine what the path of GDP would have been had government spending been allowed to grow, following the onset of the downturn in December 2007, at the same pace as it had during the Reagan years following the onset of the July 1981 downturn. The path followed is shown as the green line in the graph above on government spending around the business cycle peaks.

The resulting recovery in GDP during the current downturn would have been significantly faster:

If government spending had been allowed to grow under Obama as it had under Reagan, the economy likely would have reached full employment in 2011 (multipliers of 2.5 or 2.0), or at least by the summer of 2012 (multiplier of just 1.5). That is, the economy would have been at full employment well before the election.

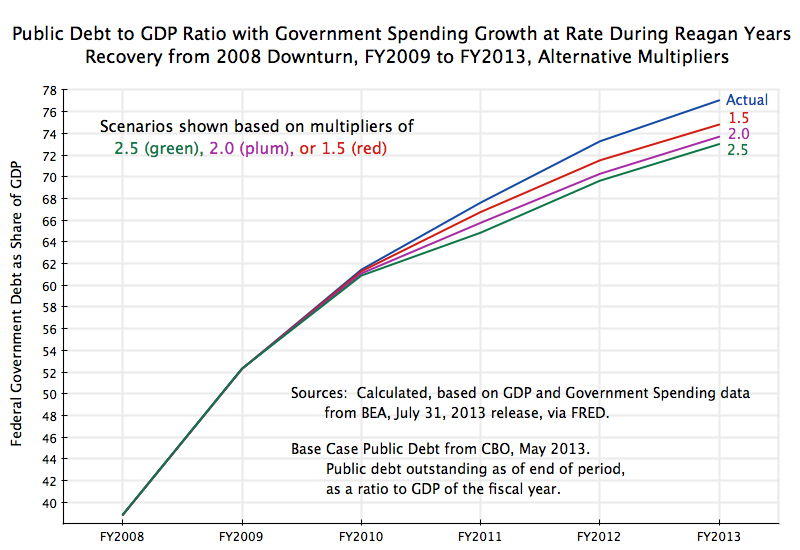

The deb to GDP ratios would also have been less than what they actually were:

Note that for these calculations I assumed that once the economy reached full employment GDP (potential GDP), that government spending was then scaled back to what was then necessary to maintain full employment, and not over-shoot it. Hence the curves for the 2.5 and 2.0 multipliers move parallel to each other (and are close to each other) once this ceiling has been reached.

D. Conclusion

Fiscal spending was not the cause of the 2008 collapse. Rather, the cause was the bursting of the housing bubble, and the resulting bankruptcy of a large share of the financial system, as well as the resulting reduction in household spending when many homeowners found that their homes were now worth less than their mortgages.

But following an initial increase in government spending, in particular as part of the fiscal stimulus package passed soon after Obama took office, government spending has been cut back. The scenarios reviewed above indicate that had government spending merely been allowed to grow at its normal historical rate from when Obama took office (i.e. even without the special stimulus package), the US would by now be at or at least close to full employment. And if government spending had grown as it had during the Reagan years, the economy would likely have reached full employment in 2011.

There is no need to introduce some special factor to explain why GDP is still so far below what it would be at full employment. There is no need to assume that something such as “business uncertainty” due to Obama, or new and burdensome regulations, have for some reason led to this slow recovery in GDP. Rather, the sluggish recovery of GDP and hence of employment can be explained fully by the policies that have kept government spending well below the historical norms.

You must be logged in to post a comment.