The Bureau of Economic Analysis (BEA) released earlier today its second estimate of GDP growth in the fourth quarter ot 2018. (Confusingly, it was officially called the “third” estimate, but was only the second as what would have been the first, due in January, was never done due to Trump shutting down most agencies of the federal government in December and January due to his border wall dispute.) Most public attention was rightly focussed on the downward revision in the estimate of real GDP growth in the fourth quarter, from a 2.6% annual rate estimated last month, to 2.2% now. And current estimates are that growth in the first quarter of 2019 will be substantially less than that.

But there is much more in the BEA figures than just GDP growth. The second report of the BEA also includes initial estimates of corporate profits and the taxes they pay (as well as much else). The purpose of this note is to update an earlier post on this blog that examined what happened to corporate profit tax revenues following the Trump / GOP tax cuts of late 2017. That earlier post was based on figures for just the first half of 2018.

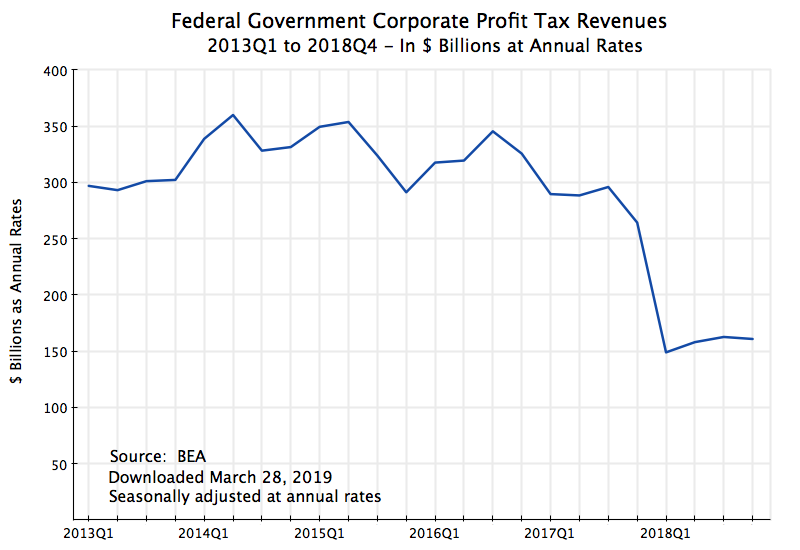

We now have figures for the full year, and they confirm what had earlier been found – corporate profit tax revenues have indeed plummeted. As seen in the chart at the top of this post, corporate profit taxes were in the range of only $150 to $160 billion (at annual rates) in the four quarters of 2018. This was less than half the $300 to $350 billion range in the years before 2018. And there is no sign that this collapse in revenues was due to special circumstances of one quarter or another. We see it in all four quarters.

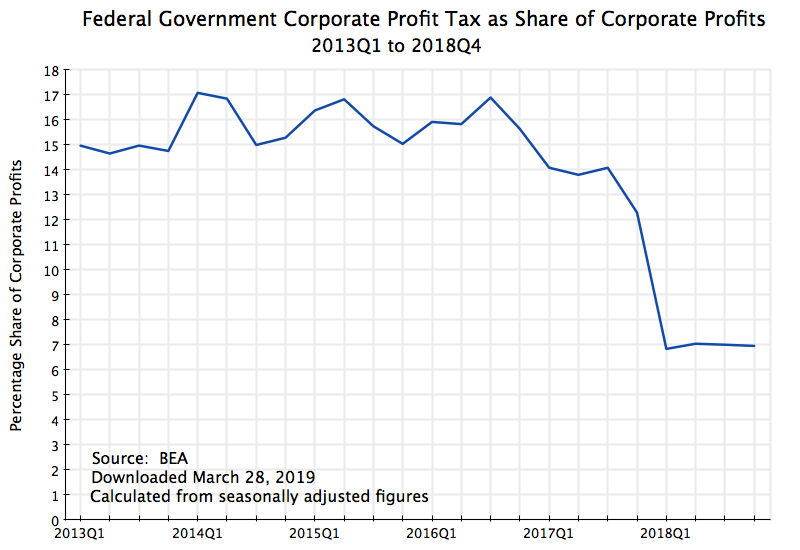

The collapse shows through even more clearly when one examines what they were as a share of corporate profits:

The rate fell from a range of generally 15 to 16%, and sometimes 17%, in the earlier years, to just 7.0% in 2018. And it was an unusually steady rate of 7.0% throughout the year. Note that under the Trump / GOP tax bill, the standard rate for corporate profit tax was cut from 35% previously to a new headline rate of 21%. But the actual rate paid turned out (on average over all firms) to come to just 7.0%, or only one-third as much. The tax bill proponents claimed that while the headline rate was being cut, they would close loopholes so the amount collected would not go down. But instead loopholes were not only kept, but expanded, and revenues collected fell by more than half.

If the average corporate profit tax rate paid in 2018 had been not 7.0%, but rather at the rate it was on average over the three prior fiscal years (FY2015 to 2017) of 15.5%, an extra $192.2 billion in revenues would have been collected.

There was also a reduction in personal income taxes collected. While the proportional fall was less, a much higher share of federal income taxes are now borne by individuals than by corporations. (They were more evenly balanced decades ago, when the corporate profit tax rates were much higher – they reached over 50% in terms of the amount actually collected in the early 1950s.) Federal personal income tax as a share of personal income was 9.2% in 2018, and again quite steady at that rate over each of the four quarters. Over the three prior fiscal years of FY2015 to 2017, this rate averaged 9.6%. Had it remained at that 9.6%, an extra $77.3 billion would have been collected in 2018.

The total reduction in tax revenues from these two sources in 2018 was therefore $270 billion. While it is admittedly simplistic to extrapolate this out over ten years, if one nevertheless does (assuming, conservatively, real growth of 1% a year and price growth of 2%, for a total growth of about 3% a year), the total revenue loss would sum to $3.1 trillion. And if one adds to this, as one should, the extra interest expense on what would now be a higher public debt (and assuming an average interest rate for government borrowing of 2.6%), the total loss grows to $3.5 trillion.

This is huge. To give a sense of the magnitude, an earlier post on this blog found that revenues equal to the original forecast loss under the Trump / GOP tax plan (summing to $1.5 trillion over the next decade, and then continuing) would suffice to ensure the Social Security Trust Fund would be fully funded forever. As things are now, if nothing is done the Trust Fund will run out in about 2034. And Republicans insist that the gap is so large that nothing can be done, and that the system will have to crash unless retired seniors accept a sharp reduction in what are already low benefits.

But with losses under the Trump / GOP tax bill of $3.1 trillion over ten years, less than half of those losses would suffice to ensure Social Security could survive at contracted benefit levels. One cannot argue that we can afford such a huge tax cut, but cannot afford what is needed to ensure Social Security remains solvent.

In the nearer term, the tax cuts have led to a large growth in the fiscal deficit. Even the US Treasury itself is currently forecasting that the federal budget deficit will reach $1.1 trillion in FY2019 (5.2% of GDP), up from $779 billion in FY2018. It is unprecedented to have such high fiscal deficits at a time of full employment, other than during World War II. Proper fiscal management would call for something closer to a balanced budget, or even a surplus, in those periods when the economy is at full employment, while deficits should be expected (and indeed called for) during times of economic downturns, when unemployment is high. But instead we are doing the opposite. This will put the economy in a precarious position when the next economic downturn comes. And eventually it will, as it always has.

You must be logged in to post a comment.