A. Introduction

Having recently completed and filed this year’s income tax forms, it is timely to examine what impact the Republican tax bill, pushed quickly through Congress in December 2017 along largely party-line votes, has had on the taxes we pay and on the process by which we figure out what they are. I will refer to the bill as the Trump/GOP tax bill as the new law reflected both what the Republican leadership in Congress wanted and what the Trump administration pushed for.

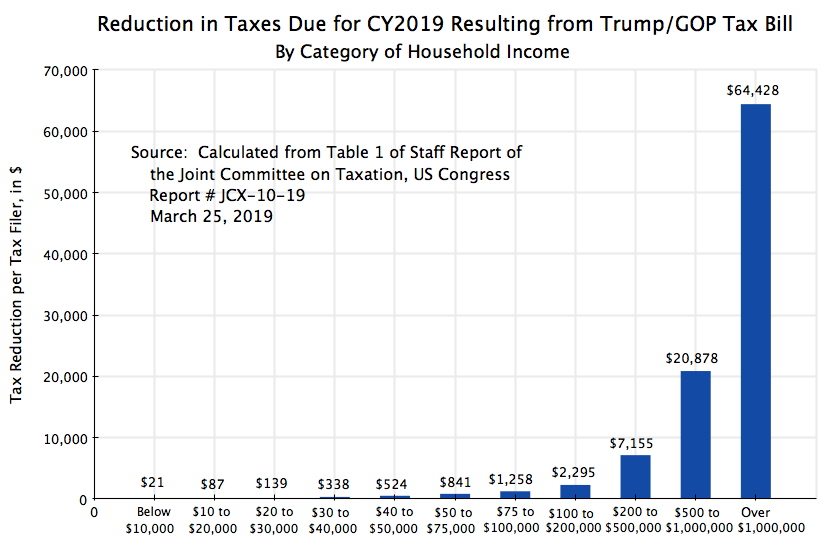

We already know well that the cuts went largely to the very well-off. The chart above is one more confirmation of this. It was calculated from figures in a recent report by the staff of the Joint Committee on Taxation of the US Congress, released on March 25, 2019 (report #JCX-10-19). While those earning more than $1 million in 2019 will, on average, see their taxes cut by $64,428 per tax filing unit (i.e. generally households), those earning $10,000 or less will see a reduction of just $21. And on the scale of the chart, it is indeed difficult to impossible even to see the bars depicting the reductions in taxes for those earning less than $50,000 or so.

The sharp bias in favor of the rich was discussed in a previous post on this blog, based there on estimates from a different group (the Tax Policy Center, a non-partisan think tank) but with similar results. And while it is of course true that those who are richer will have more in taxes that can be cut (one could hardly cut $64,428 from a taxpayer earning less than $10,000), it is not simply the absolute amounts but also the share of taxes which were cut much further for the rich than for the poor. According to the Joint Committee on Taxation report cited above, those earning $30,000 or less will only see their taxes cut by 0.5% of their incomes, while those earning between $0.5 million and $1.0 million will see a cut of 3.1%. That is more than six times as much as a share of incomes. That is perverse.

And the overall average reduction in individual income taxes will only be a bit less than 10% of the tax revenues being paid before. This is in stark contrast to the more than 50% reduction in corporate income taxes that we have already observed in what was paid by corporations in 2018.

Furthermore, while taxes for households in some income category may have on average gone down, the numerous changes made to the tax code on the Trump/GOP bill meant that for many it did not. Estimates provided in the Joint Committee on Taxation report cited above (see Table 2 of the report) indicate that for 2019 a bit less than two-thirds of tax filing units (households) will see a reduction in their taxes of $100 or more, but more than one-third will see either no significant change (less than $100) or a tax increase. The impacts vary widely, even for those with the same income, depending on a household’s particular situation.

But the Trump/GOP tax bill promised not just a reduction in taxes, but also a reduction in tax complexity, by eliminating loopholes and from other such measures. The claim was that most Americans would then be able to fill in their tax returns “on a postcard”. But as is obvious to anyone who has filed their forms this year, it is hardly that. This blog post will discuss why this is so and why filling in one’s tax returns remains such a headache. The fundamental reason is simple: The tax system is not less complex than before, but more.

There is, however, a way to address this, and not solely by ending the complexity (although that would in itself be desirable). Even with the tax code as complicated as it now is (and more so after the Trump/GOP bill), the IRS could complete for each of us a draft of what our filing would look like based on the information that the IRS already collects. Those draft forms would match what would be due for perhaps 80 to 85% of us (basically almost all of those who take the standard deduction). For that 80 to 85% one would simply sign the forms and return them along with a payment if taxes are due or a request for a refund if a refund is due. Most remaining taxpayers would also be able to use these initial draft forms from the IRS, but for them as the base for what they would need to file. In their cases, additions or subtractions would be made to reflect items such as itemized deductions (mostly) and certain special tax factors (for some) where the information necessary to complete such calculations would not have been provided in the normal flow of reports to the IRS. And a small number of filers might continue to fill in all their forms as now. That small number would be no worse than now, while life would be much simpler for the 95% or more (perhaps 99% or more) who could use the pre-filled in forms from the IRS either in their entirety or as a base to start from.

The IRS receives most of the information required to do this already for each of us (and all that is required for most of us). But what would be different is that instead of the IRS using such information to check what we filed after the fact, and then impose a fine (or worse) if we made a mistake, the IRS would now use that same information to fill in the forms for us. We would then review and check them, and if necessary or advantageous to our situation we could then adjust them. We will discuss how such a tax filing system could work below.

B. Our Tax Forms are Now Even More Complex Than Before

Trump and the Republican leaders in Congress promised that with the Trump/GOP tax bill, the tax forms we would need to file could, for most of us, fit just on a postcard. And Treasury Secretary Steven Mnuchin then asserted that the IRS (part of Treasury) did just that. But this is simply nonsense, as anyone who has had to struggle with the new Form 1040s (or even just looked at them) could clearly see.

Specifically:

a) Form 1040 is not a postcard, but a sheet of paper (front and back), to which one must attach up to six separate schedules. This previously all fit on one sheet of paper, but now one has to complete and file up to seven just for the 1040 itself.

b) Furthermore, there are no longer the forms 1040-EZ or 1040-A which were used by those with less complex tax situations. Now everyone needs to work from a fully comprehensive Form 1040, and try to figure out what may or may not apply in their particular circumstances.

c) The number of labeled lines on the old 1040 came to 79. On the new forms (including the attached schedules) they come to 75. But this is misleading, as what used to be counted as lines 1 through 6 on the old 1040 are now no longer counted (even though they are still there and are needed). Including these, the total number of numbered lines comes to 81, or basically the same as before (and indeed more).

d) Spreading out the old Form 1040 from one sheet of paper to seven does, however, lead to a good deal of extra white space. This was likely done to give it (the first sheet) the “appearance” of a postcard. But the forms would have been much easier to fill in, with less likelihood of error, if some of that white space had been used instead for sub-totals and other such entries so that all the steps needed to calculate one’s taxes were clear.

e) Specifically, with the six new schedules, one has to carry over computations or totals from five of them (all but the last) to various lines on the 1040 itself. But this was done, confusingly, in several different ways: 1) The total from Schedule 4 was carried over to its own line (line 14) on the 1040. It would have been best if all of them had been done this way, but they weren’t. Instead, 2) The total from Schedule 2 was added to a number of other items on line 11 of the 1040, with the total of those separate items then shown on line 11. And 3) The total from Schedule 1 was added to the sum of what is shown on the lines above it (lines1 through 5b of the 1040) and then recorded on line 6 of the 1040.

If this looks confusing, it is because it is. I made numerous mistakes on this when completing my own returns (yes – I do these myself, as I really want to know how they are done). I hope my final returns were done correctly. And it is not simply me. Early indications (as of early March) were that errors on this year’s tax forms were up by 200% over last year’s (i.e. they tripled).

f) There is also the long-standing issue that the actual forms that one has to fill out are in fact substantially greater than those that one files, as one has to fill in numerous worksheets in order to calculate certain of the figures. These worksheets should be considered part of the returns, and not hidden in the directions, in order to provide an honest picture of what is involved. And they don’t fit on a postcard.

g) But possibly what is most misleading about what is involved in filling out the returns is not simply what is on the 1040 itself, but also the need to include on the 1040 figures from numerous additional forms (for those that may apply). Few if any of them are applicable to one’s particular tax situation, but to know whether they do or not one has to review each of those forms and make such a determination. How does one know whether some form applies when there is a statement on the 1040 such as “Enter the amount, if any, from Form xxxx”? The only way to know is to look up the form (fortunately now this can be done on the internet), read through it along with the directions, and then determine whether it may apply to you. Furthermore, in at least a few cases one can only know if the form applies to your situation is by filling it in and then comparing the result found to some other item to see whether filing that particular form applies to you.

There are more than a few such forms. By my count, one has just on the Form 1040 plus its Schedules 1 through 5 amounts that might need to be entered from Forms 8814, 4972, 8812, 8863, 4797, 8889, 2106, 3903, SE, 6251, 8962, 2441, 8863, 8880, 5695, 3800, 8801,1116, 4137, 8919, 5329, 5405, 8959, 8960, 965-A, 8962, 4136, 2439, and 8885. Each of these forms may apply to certain taxpayers, but mostly only a tiny fraction of them. But all taxpayers will need to know whether they might apply to their particular situation. They can often guess that they probably won’t (and it likely would be a good guess, as most of these forms only apply to a tiny sliver of Americans), but the only way to know for sure is to check each one out.

Filling out one’s individual income tax forms has, sadly, never been easy. But it has now become worse. And while the new look of the Form 1040 appears to be a result of a political decision by the Trump administration (“make it look like it could fit on a postcard”), the IRS should mostly not be blamed for the complexity. That complexity is a consequence of tax law, as written by Congress, which finds it politically advantageous to reward what might be a tiny number of supporters (and campaign contributors) with some special tax break. And when Congress does this, the IRS must then design a new form to reflect that new law, and incorporate it into the Form 1040 and now the new attached schedules. And then everyone, not simply the tiny number of tax filers to whom it might in fact apply, must then determine whether or not it applies to them.

There are, of course, also more fundamental causes of the complexity in the tax code, which must then be reflected in the forms. The most important is the decision by our Congress to tax different forms of income differently, where wages earned will in general be taxed at the highest rates (up to 37%) while capital gains (including dividends on stocks held for more than 60 days) are taxed at rates of just 20% or less. And there are a number of other forms of income that are taxed at various rates (including now, under the Trump/GOP tax bill, an effectively lower tax rate for certain company owners on the incomes they receive from their companies, as well as new special provisions of benefit to real estate developers). As discussed in an earlier post on this blog, there is no good rationale, economic or moral, to justify this. It leads to complex tax calculations as the different forms of income must each be identified and then taxed at rates that interact with each other. And it leads to tremendous incentives to try to shift your type of income, when you are in a position to do so, from wages, say, to a type taxed at a lower rate (such as stock options that will later be taxed only at the long-term capital gains rate).

Given this complexity, it is no surprise that most Americans turn either to professional tax preparers (accountants and others) to fill in their tax forms for them, or to special tax preparation software such as TurboTax. Based on statistics for the 2018 tax filing season (for 2017 taxes), 72.1 million tax filers hired professionals to prepare their tax forms, or 51% of the 141.5 million tax returns filed. The cost varies by what needs to be filed, but even assuming an average fee of just $500 per return, this implies a total of over $36 billion is being paid by taxpayers for just this service.

Most of the remaining 49% of tax filers use tax preparation software for their returns (a bit over three-quarters of them). But these are problematic as well. There is also a cost (other than for extremely simple returns), but the software itself may not be that good. A recent review by Consumer Reports found problems with each of the four major tax preparation software packages it tested (TurboTax, H&R Block, TaxSlayer, and TaxAct), and concluded they are not to be trusted.

And on top of this, there is the time the taxpayer must spend to organize all the records that will be needed in order to complete the tax returns – whether by a hired professional tax preparer, or by software, or by one’s own hand. A 2010 report by a presidential commission examing options for tax reform estimated that Americans spend about 2.5 billion hours a year to do what is necessary to file their individual income tax returns, equivalent to $62.5 billion at an average time cost of $25 per hour.

Finally there are the headaches. Figuring one’s taxes, even if a professional is hired to fill in the forms, is not something anyone wants to spend time on.

There is a better way. With the information that is already provided to the IRS each year, the IRS could complete and provide to each of us a draft set of tax forms which would suffice (i.e. reflect exactly what our tax obligation is) for probably 80% or more of households. And most of the remainder could use such draft forms as a base and then provide some simple additions or subtractions to arrive at what their tax obligation is. The next section will discuss how this could be done.

C. Have the IRS Prepare Draft Tax Returns for Each of Us

The IRS already receives, from employers, financial institutions, and others, information on the incomes provided to each of us during the tax year. And these institutions then tell us each January what they provided to the IRS. Employers tell us on W-2 forms what wages were paid to us, and financial institutions will tell us through various 1099 forms what was paid to us in interest, in dividends, in realized capital gains, in earnings from retirement plans, and from other such sources of returns on our investments. Reports are also filed with the IRS for major transactions such as from the sale of a home or other real estate.

The IRS thus has very good information on our income each year. Our family situation is also generally stable from year to year, although it can vary sometimes (such as when a child is born). But basing an initial draft estimate on the household situation of the previous year will generally be correct, and can be amended when needed. One could also easily set up an online system through which tax filers could notify the IRS when such events occur, to allow the IRS to incorporate those changes into the draft tax forms they next produce.

For most of those who take the standard deduction, the IRS could then fill in our tax forms exactly. And most Americans take the standard deduction. Prior to the Trump/GOP tax bill, about 70% of tax filers did, and it is now estimated that with the changes resulting from the new tax bill, about 90% will. Under the Trump/GOP tax bill, the basic standard deduction was doubled (while personal exemptions were eliminated, so not all those taking the standard deduction ended up better off). And perhaps of equal importance, the deduction that could be taken on state and local taxes was capped at $10,000 while how much could be deducted on mortgage interest was also narrowed, so itemization was no longer advantageous for many (with these new limitations primarily affecting those living in states that vote for Democrats – not likely a coincidence).

The IRS could thus prepare filled in tax forms for each of us, based on information contained in what we had filed in earlier years and assuming the standard deduction is going to be taken. But they would just be drafts. They would be sent to us for our review, and if everything is fine (and for most of the 90% taking the standard deduction they would be) we would simply sign the forms and return them (along with a check if some additional tax is due, or information on where to deposit a refund if a tax refund is due).

But for the 10% where itemized deductions are advantageous, and for a few others who are in some special tax situation, one could either start with the draft forms and make additions or subtractions to reflect simple adjustments, or, if one wished, prepare a new set of forms reflecting one’s tax situation. There would likely not be many of the latter, but it would be an option, and no worse than what is currently required of everyone.

For those making adjustments, the changes could simply be made at the end. For example (and likely the most common such situation), suppose it was advantageous to take itemized deductions rather than the standard deduction. One would fill in the regular Schedule A (as now), but then rather than recomputing all of the forms, one could subtract from the taxes due an amount based on what the excess was of the itemized deductions over the standard deduction, and one’s tax rate. Suppose the excess of the itemized deductions over the standard deduction for the filer came to $1,000. Then for the very rich (households earning over $600,000 a year after deductions), one would reduce the taxes due by 37%, or $370. Those earning $400,000 to $600,000, in the 35% bracket, would subtract $350. And so on down to the lower brackets, where those in the 12% bracket (those earning $19,050 to $77,400) would subtract $120 (and those earning less than $19,050 are unlikely to itemize).

[Side Note: Why do the rich receive what is in effect a larger subsidy from the government than the poor do for what they itemize, such as for contributions to charities? That is, why do the rich effectively pay just $630 for their contribution to a charity ($1,000 minus $370), while the poor pay $880 ($1,000 minus $120) for their contribution to possibly the exact same charity? There really is no economic, much less moral, reason for this, but that is in fact how the US tax code is currently written. As discussed in an earlier post on this blog, the government subsidy for such deductions could instead be set to be the same for all, at say a rate of 20% or so. There is no reason why the rich should receive a bigger subsidy than the poor receive for the contributions they make.]

Another area where the information the IRS would not have complete information to compute taxes due would be where the tax filer had sold a capital asset which had been purchased before 2010. The IRS only started in 2010 to require that financial institutions report the cost basis for assets sold, and this cost basis is needed to compute capital gains (or losses). But as time passes, a smaller and smaller share of assets sold will have been purchased before 2010. The most important, for most people, will likely be the cost of the home they bought if before 2010, but such a sale will happen only once (unless they owned multiple real estate assets in 2010).

But a simple adjustment could be made to reflect the cost basis of such assets, similar to the adjustment for itemized deductions. The draft tax forms filled in by the IRS would leave as blank (zero) the cost basis of the assets sold in the year for which it did not have a figure reported. The tax filer would then determine what the cost basis of all such assets should be (as they do now), add them up, and then subtract 20% of that total cost basis from the taxes due (for those in the 20% bracket for long term capital gains, as most people with capital gains are, or use 15% or 0% if those tax brackets apply in their particular cases).

There will still be a few tax filers with more complex situations where the IRS draft computations are not helpful, who will want to do their own forms. This is fine – there would always be that option. But such individuals would still be no worse off than what is required now. And their number is likely to be very small. While a guess, I would say that what the IRS could provide to tax filers would be fully sufficient and accurate for 80 to 85% of Americans, and that simple additions or subtractions to the draft forms (as described above) would work for most of the rest. Probably less than 5% of filers would need to complete a full set of forms themselves, and possibly less than 1%.

D. Final Remarks

Such an approach would be new for the US. But there is nothing revolutionary about it. Indeed, it is common elsewhere in the world. Much of Western Europe already follows such an approach or some variant of it, in particular all of the Scandinavian countries as well as Germany, Spain, and the UK, and also Japan. Small countries, such as Chile and Estonia, have it, as do large ones.

It has also often been proposed for the US. Indeed, President Reagan proposed it as part of his tax reduction and simplification bill in 1985, then candidate Barack Obama proposed it in 2007 in a speech on middle class tax fairness, a presidential commission in 2010 included it as one of the proposals in its report on simplifying the tax system, and numerous academics and others have also argued in its favor.

It would also likely save money at the IRS. The IRS collects already most of the information needed. But that information is not then sent back to us in fully or partially filled in tax forms, but rather is used by the IRS after we file to check to see whether we got anything wrong. And if we did, we then face a fine or possibly worse. Completing our tax returns should not be a game of “gotcha” with the IRS, but rather an effort to ensure we have them right.

Such a reform has, however, been staunchly opposed by narrow interests who benefit from the current frustrating system. Intuit, the seller of TurboTax software, has been particularly aggressive through its congressional lobbying and campaign contributions in using Congress to block the IRS from pursuing this, as has H&R Block. They of course realize that if tax filing were easy, with the IRS completing most or all of the forms for us, there would be no need to spend what comes to billions of dollars for software from Intuit and others. But the morality of a business using its lobbying and campaign contributions to ensure life is made particularly burdensome for the citizenry, so that it can then sell a product to make it easier, is something to be questioned.

One can, however, understand the narrow commercial interests of Intuit and the tax software companies. One can also, sadly, understand the opposition of a number of conservative political activists, with Grover Norquist the most prominent and in the lead. They have also aggressively lobbied Congress to block the IRS from making tax filing simpler. They are ideologically opposed to taxes, and see the burden and difficulty in figuring out one’s taxes as a positive, not as a negative. The hope is that with more people complaining about how difficult it is to fill in their tax forms, the more people will be in favor of cutting taxes. While that view on how people see taxes might well be accurate, what many may not realize is that the tax cuts of recent decades have led to greater complexity and difficulty, not less. With new loopholes for certain narrow interests, and with income taxed differently depending on the source of that income (with income from wealth taxed at a much lower rate than income from labor), the system has become more complex while generating less revenue overall.

But it is perverse that Congress should legislate in favor of making life more difficult. The tax system is indeed necessary and crucial, as Reagan correctly noted in his 1985 speech on tax reform, but as he also noted in that speech, there is no need to make them difficult. Most Americans, Reagan argued, should be able, and would be able under his proposals, to use what he called a “return-free” system, with the IRS working out the taxes due.

The system as proposed above would do this. It would also be voluntary. If one disagreed with the pre-filled in forms sent by the IRS, and could not make the simple adjustments (up or down) to the taxes due through the measures as discussed above, one could always fill in the entire set of forms oneself. But for that small number of such cases this would just be the same as is now required for all. Furthermore, if one really was concerned about the IRS filling in one’s forms for some reason (it is not clear what that might be), one could easily have a system of opting-out, where one would notify the IRS that one did not want the service.

The tax code itself should still be simplified. There are many reforms that can and should be implemented, if there was the political will. The 2010 presidential commission presented numerous options for what could be done. But even with the current complex system, or rather especially because of the current complex system, there is no valid reason why figuring out and filing our taxes should be so difficult. Let the IRS do it for us.

You must be logged in to post a comment.