A. Introduction

The contribution of changes in inventories to changes in reported GDP is easily misunderstood. One saw this in reports on the recent release (on July 28) by the Bureau of Economic Analysis (BEA) of its first estimate of GDP for the second quarter of 2022. It estimated that GDP fell – at an annualized rate of -0.9% in the quarter – and that along with the first quarter decline in GDP (at an estimated rate of -1.6%), the US has now seen two straight quarters of falling GDP. While there will be revisions in the coming months of the second quarter figures, as additional data become available, a fall in GDP for two straight quarters has often been used as a rule of thumb for an economy being in recession.

News reports on the figures noted also that were it not for the estimated change in inventories, GDP would have gone up rather than down. The estimate was that GDP fell by -0.9% (at an annual rate) in the second quarter, and that the change in private inventories alone accounted for a 2.0% point reduction in GDP. That is, if the inventory contribution had been neutral, GDP would have grown by about 1% rather than fallen by almost 1%.

But it would be wrong to attribute this to “decreases in inventories”, as some reports did. Inventories grew strongly in the fourth quarter of 2021, with this continuing at a similarly strong pace in the first quarter of 2022 and still (although at a slower pace) in the second quarter of 2022. How, then, could this have contributed to a reduction in GDP in 2022?

It is easy to become confused on this. While really just a consequence of some basic arithmetic, it does require a good understanding of what GDP is and how changes in inventories are reflected in GDP. I discussed this in a January 2012 post on this blog, but that was more than a decade ago and a revisit to the issue may be warranted. This post will examine the problem from a different perspective from that used before. It will start with a review of what GDP measures, and then use some simple numerical examples to show how changes in inventories affect GDP. It will then use a series of charts, based on actual numbers from the GDP accounts in recent years, to show how changes in inventories have mattered.

A note of the data: All the figures used come from the BEA National Income and Product Accounts (NIPA), as updated through the July 28 release. These are often also called by many (including myself) the GDP accounts, but NIPA is the more proper term. Also, the figures for inventories in the NIPA accounts are for private inventories only. Inventories held by government entities are small and are not broken out separately in the accounts. Instead, changes in such inventories are aggregated into the figures for government consumption. While I will often refer to “inventories” in this post, the measures of those inventories are technically for private inventories only.

B. Inventories and GDP, with Some Simple Numerical Illustrations

GDP – Gross Domestic Product – is a measure of production (product). Yet as anyone who has ever taken an Econ 101 class knows, GDP is typically described as (and measured by) how those goods and services are used: for Consumption plus Investment plus Government Spending plus Net Foreign Trade (Exports less Imports). In symbols:

GDP = C + I + G + (X-M)

Where “C” is private consumption; “I” is private investment; “G” is government spending on goods or services for direct consumption or investment; and “X-M” is exports minus imports, or net foreign trade.

(Imports, M, can be thought of either as an addition to the supply of available goods or netted out from exports, X, to yield net exports. To keep the language simple, I will treat it as being netted out from exports.)

Private investment includes investment both in new fixed assets (such as buildings or machinery and equipment) and in accumulation of inventory. This accumulation of inventory, or net change in inventory, is key to why this equation adds up. As noted above, GDP is product – how much is produced. Whatever is produced can then be sold for consumption, fixed asset investment, government spending on consumption or investment, or net exports. If whatever is produced exceeds what is sold in the period for these various purposes, then the difference will accrue as inventories. If the amount produced falls short of what is sold, there will have to have been a drawdown of inventories for the demands to have been met. Otherwise it would not have been possible – the goods had to come from somewhere.

The balancing item is therefore the change in inventories. It is what allows us to go from an estimate of what is sold to an estimate (if one knows how much inventories changed by) of what was produced, i.e. to Gross Domestic Product.

How then do changes in inventories affect measured GDP? This is best seen through a series of simple numerical examples, tracing changes in the stock of inventories over time.

|

Period |

Stock |

Change |

Change in the Change |

|

0 |

2000 |

||

|

1 |

2200 |

200 |

|

|

2 |

2400 |

200 |

0 |

Start with a stock of inventories in the economy as a whole in period 0 of say 2000 (in whatever units – perhaps billions of dollars). This stock then grows to 2200 in period 1 and 2400 in period 2. The change in inventories in period 1 will then be 200, and that change in inventories will be one of the components making up GDP (along with private consumption, private fixed investment, and so on). It is an investment – an investment in inventories – and thus one of the uses of whatever product was produced in the period. It will equal the total of what was produced (GDP) less what was sold for the sum of all final demands (private consumption, private fixed Investment, government, and net foreign trade).

With the stock of inventories growing to 2400 in period 2, the change in inventories in that period will once again be 200. Hence the contribution to GDP will once again be 200. This is the same as what its contribution to GDP was in the previous period, and hence the higher inventories would not have been a contributor to some higher level of GDP – its contribution to GDP is the same as before. The change in the change in the stock of inventories is zero.

But this does not mean that inventories fell in period 2. They grew by 200. But that was simply the same as its accumulation in the prior period, so it did not add to GDP growth.

To make a contribution to GDP growth in period 2, the addition to inventories would have had to have grown. For example:

|

Period |

Stock |

Change |

Change in the Change |

|

0 |

2000 |

||

|

1 |

2200 |

200 |

|

|

2 |

2500 |

300 |

100 |

In this example, the stock of inventories grew to 2500 in period 2. The change in inventories was then 300, which is higher than the change in inventories of 200 in period 2 – it is 100 more. This would be reflected in a GDP in period 2 which would be 100 higher than it would have been otherwise.

If, on the other hand, the pace of inventory accumulation slows, then inventory accumulation will subtract from GDP:

|

Period |

Stock |

Change |

Change in the Change |

|

0 |

2000 |

||

|

1 |

2200 |

200 |

|

|

2 |

2300 |

100 |

-100 |

In this example, inventories are still growing in period 2 – to a level of 2300. This is 100 higher than what it was in period 2. But the change in inventories is then only 100 – which is less than the change of 200 in period 1. Inventories are still growing but they will add less to GDP than they had in period 2. Hence they will subtract from whatever growth in GDP there might have been otherwise.

This is what happened in the recently released estimates for GDP growth in the second quarter of 2022. Inventories were still growing, but they were growing at a slower pace than in the prior quarter. In terms of annual rates (and with seasonally adjusted figures), inventories grew by $81.6 billion in the second quarter (in terms of constant 2012 dollar prices; see line 40 of Table 3 of the BEA release). But this was less than the $188.5 billion growth in inventories in the first quarter of 2022. In percentage point terms, that difference (a reduction of $106.8 billion) subtracted 2.0% from what GDP growth would have otherwise been in the second quarter (see line 40 of Table 2 of the BEA release). With the changes in the other components of GDP, the end result was that estimated GDP fell by 0.9% in the quarter. Thus one can attribute the fall in GDP in the quarter to what happened to inventories, but not because inventories fell. It was because they did not grow as fast as they had in the previous quarter.

C. Changes in Inventories in the Data

Based on this, it is of interest to see how inventories have in fact changed quarter to quarter in recent years. These changes, and especially the changes in the changes, are volatile. They can make a big difference in the quarter-to-quarter changes in GDP. Over time, however, they will even out, as there is some desired level of inventories in relation to their sales and producers will target their purchases to levels to try to reach that desired level.

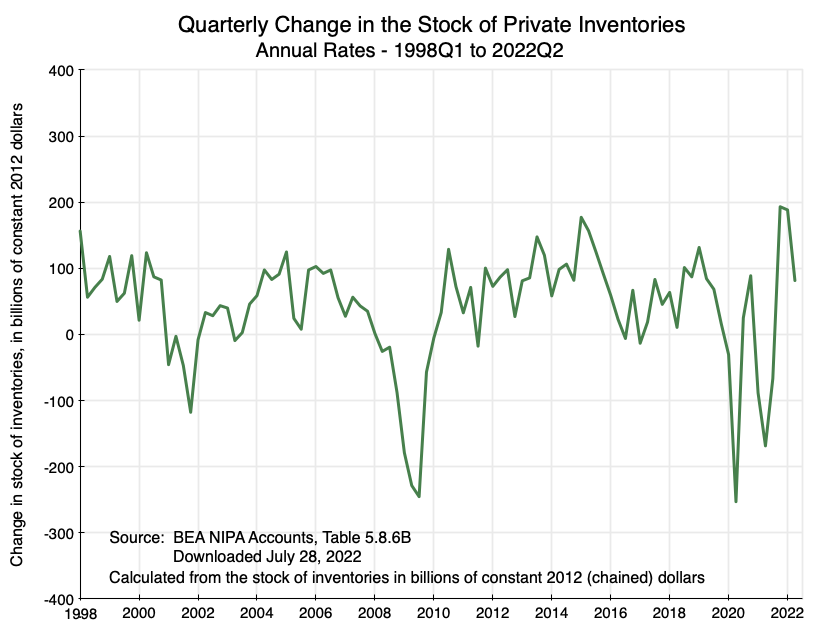

Start with the chart at the top of this post. It shows the stock of private inventories by quarter going back to 1998. The figures are in constant 2012 dollars so that inflation is not a factor (and more precisely using what are called “chained” dollars where the weights used to compute the overall indices are based on prior period shares of each of the goods – so the weights shift over time as these shares shift).

Stocks generally move up over time as the economy grows, although there have been reductions in periods when the economy was in recession or otherwise disrupted. Thus one sees a fall in 2001, due to the recession in the first year of the Bush II administration, an especially sharp fall in 2008 with the onset of the economic and financial collapse in the last year of the Bush II administration with this then carrying over into 2009, and then a fall again in 2020 due to the Covid lockdowns. The trough in the most recent downturn was reached in the third quarter of 2021, following which the stock of inventories grew rapidly. They are still, however, slightly below the level reached in mid-2019 even though GDP is higher now than what it was then.

One starts with the stocks, but as was discussed above, the contribution to GDP comes from the accumulation of inventories – the change in the stocks. These changes, based on the figures underlying the chart at the top of this post, have been:

There is considerable quarter-to-quarter volatility. Note that the figures here are expressed in terms of annual rates. That is, they are each four times what the actual change was (in dollar terms) in the given quarter. One sees that the change in the fourth quarter of 2021 was quite high – higher than in any other quarter of this 24-year period – and was still almost as high in the first quarter of 2022. The increase was then less in the second quarter of 2022, but was still a substantial increase (of $81.6 billion at an annual rate) in the quarter.

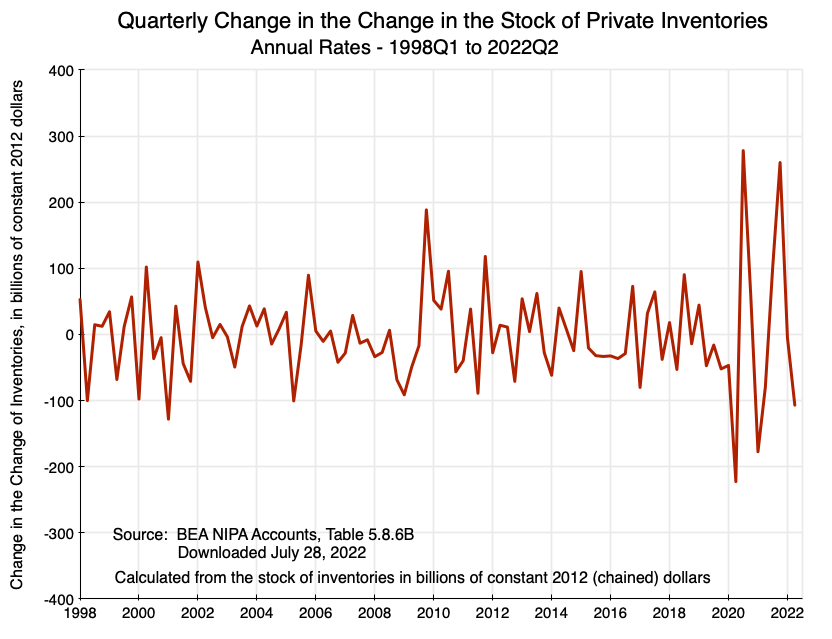

The changes in inventories are a component of GDP, but the contribution to the growth in GDP comes from the changes in the change in inventories. These are easily computed as well by simple subtraction, and were:

These are now very highly volatile, and one sees especially sharp fluctuations in the last couple of years. With all the disruptions of the lockdowns, the subsequent supply chain disruptions, and the very strong recovery of the economy in 2021 (with GDP growing faster than in any year in almost four decades, and private consumption growing faster than in any year since 1946!), it has been difficult to manage production to meet expected demands and allow for some desired target level of inventories.

This had a substantial impact on the quarter-to-quarter changes in GDP, both positive and negative. Focussing on the recent quarters, the changes in inventories were a $193.2 billion increase in the fourth quarter of 2021, and as noted before, a further $188.5 billion increase in the first quarter of 2022 and a further although smaller increase of $81.6 billion in the second quarter of 2022. These were the changes in inventories. But the changes in the changes, which is what will add to or subtract from GDP growth, were a very high $260.0 billion in the fourth quarter of 2021, and then a fall of $4.7 billion in the first quarter of 2022. This reduction in the first quarter of 2022 came despite inventories increasing in that quarter by close to a record high level. But they followed a quarter where inventories rose by a bit more, so the change in the change was small and indeed a bit negative.

In the second quarter of 2022 inventories again rose – by $81.6 billion. But following the close to record high growth in the first quarter of 2022, its contribution to the growth in GDP in the quarter was substantially negative. The $81.6 billion increase in inventories in the second quarter was $106.9 billion less than the increase of $188.5 billion in the first quarter. And it is this $106.9 billion which is a contribution to (or in this case a subtraction from) what GDP growth would have been in the quarter.

Finally, one can show this also in the possibly more helpful units of the percentage point contribution to the growth in GDP:

Although in different units, the chart here mirrors closely the preceding one, as one would expect if one has been doing the calculations correctly. The only difference, in principle, is that with GDP growth over time, the dollar values of the quarter-to-quarter changes will look larger when expressed as a share of GDP in the earlier years of the period.

There are, however, some minor differences deriving from the nature of the data used. The chart here was drawn directly from the figures presented in the BEA NIPA accounts for the percentage point contributions to GDP growth from changes in inventories. One can also calculate it by taking the quarterly changes in the change in constant dollar terms (from the preceding chart, in red), dividing it by the previous quarter’s GDP (as one is looking at growth over the preceding quarter), and then annualizing it by taking one plus the ratio to the fourth power. I did that, and the curve lies very close to on top of the curve shown here (in orange).

But not quite, due in part to rounding errors that compound when one is taking the changes and then the changes in the changes. In addition, inventories by their nature are highly heterogeneous, with some going up and some down in any given period even though there is some bottom line total on whether the aggregate rose or fell. This makes working with price indices tricky. The BEA figures are based on far more disaggregated calculations than the ones they present in the NIPA accounts, and their underlying data also have more significant digits than what they show in the tables they report.

D. Inventories to Sales, and Near Term Prospects

What will happen to inventories now? Given how important changes in inventories are to the quarter-to-quarter figures on GDP growth, economists have long tried to develop some system to predict how they will change (as have Wall Street analysts, where success in this could make some of them very rich). But they have all failed (at least to my knowledge).

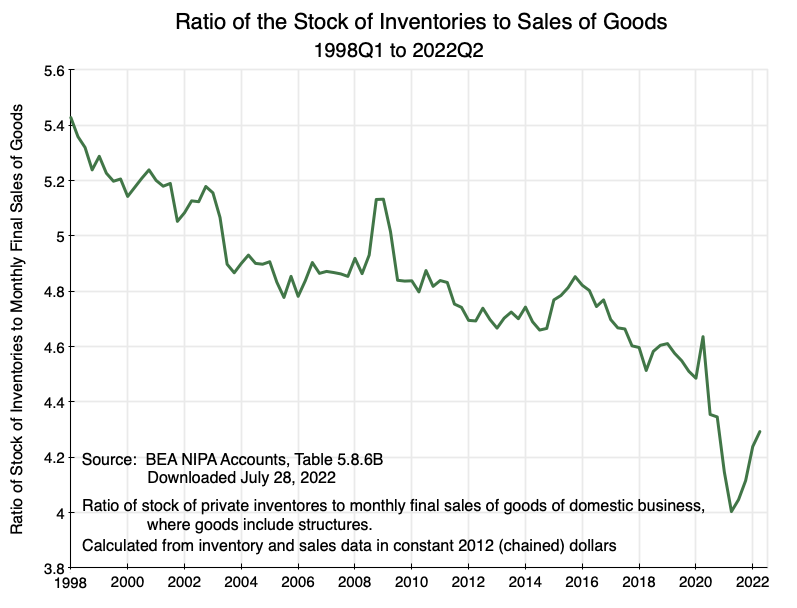

One statistic that many focus on, quite logically, is the ratio of inventory to sales:

The figures here were computed from data reported in the BEA NIPA Accounts, Table 5.8.6B, where inventories include all private inventories while sales are of goods (including newly built structures) sold by domestic businesses. Inventories are by nature of goods only, and hence one should leave out services (as an increasing share of services in GDP would, on its own, lead to a fall in the ratio). Sales of newly built structures are included as one has inventories of building materials. The figures on the sale of goods by domestic businesses are provided by the BEA. Note that “sales” here are expressed on a monthly basis. Hence the ratio is of inventories in terms of months of sales.

As one sees in the chart, the ratio of inventory to sales has been coming down over time. This is consistent with all the literature advising on tighter inventory management. There was then an unusually sharp decline in 2020 – a consequence of the Covid lockdowns – that bottomed out in the second quarter of 2021 (as a share of sales) and has since grown strongly. But the ratio is still below where it was prior to the pre-Covid trend, although how much below depends on how one would draw the trend line pre-Covid.

Where will it go from here? While important to what will happen to the quarter-to-quarter figures for GDP growth, as discussed above, I doubt that anyone has a good forecast of what that will be. While there might well be room for the inventory to sales ratio to rise from where it is now, keep in mind that the ratio can rise not only by adding to inventories but also by sales going down. And while GDP growth was exceptionally strong in 2021, it has been weak so far this year (indeed negative) and that weakness might well worsen. Personally, while I do not see that the economy is in recession now (employment growth has been strong, with 2.7 million net new jobs in the first half of 2022, and the unemployment rate has been just 3.6% for several months now), the likelihood of a recession in 2023 is, I would say, quite high.

There also have been recent announcements by major retailers that the inventories they are currently holding are well in excess of what they want, and that they will take exceptional measures to try to bring them down. Target announced a plan to do so in June (with a warning it will squeeze their near-term profits), Walmart announced in July they had similar issues (and that it would slash prices to move that inventory), and other retailers have announced similar problems. If this is indeed a general issue, then those efforts to bring down inventories in themselves will act as a strong drag on the economy, making a recession even more likely. And as was discussed above, the stock of inventories does not need to fall in absolute terms to cut GDP growth – a change that is less than what the change had been in the prior period will subtract from GDP growth, even though the inventories may still be growing in absolute terms.

Firms such as Target and Walmart employ many highly trained professionals to manage their inventories. Yet even they find it difficult to get their inventories to come out where they want them to be. If they and others now begin a concerted effort to bring down their inventory levels in the coming months, the impact on GDP in the rest of this year could be severe.

You must be logged in to post a comment.