A. Introduction

A debate now underway between the Trump Administration and others is on the question of how fast the economy can and will grow. Trump claimed during the presidential campaign that if elected, he would get the economy to grow at a sustained rate of 5% or even 6%. Since then the claim has been scaled back, to a 4% rate over the next decade according to the White House website (at least claimed on that website as I am writing this). And an even more modest rate of growth of 3% for GDP (to be reached in 2020, and sustained thereafter) was forecast in the budget OMB submitted to Congress in May of this year.

But many economists question whether even a 3% growth rate for a sustained period is realistic, as would I. One needs to look at this systematically, and this post will describe one way economists would address this critically important question. It is not simply a matter of pulling some number out of the air (where the various figures presented by Trump and his administration, varying between 6% growth and 3%, suggests that that may not be far removed from what they did).

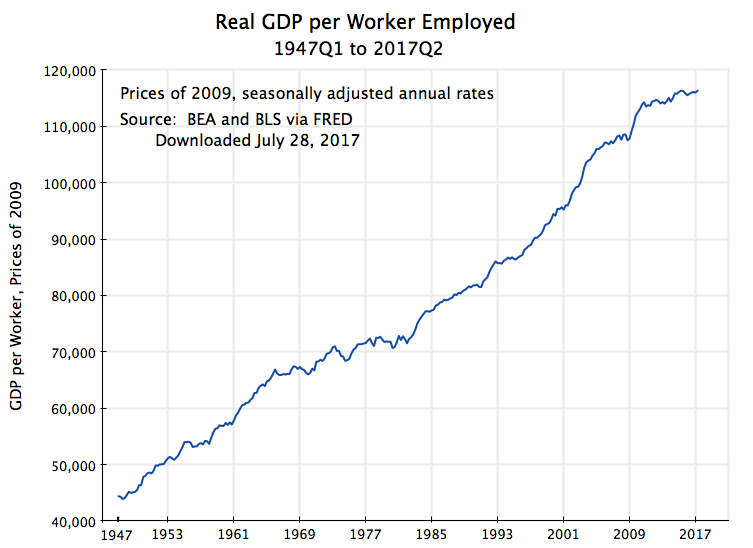

One way to approach this is to recognize the simple identity: GDP will equal GDP per worker employed times the number of workers employed. Over time, growth in the number of workers who can be employed will be equal to the growth in the labor force, and we have a pretty good forecast for that will be from demographic projections. The other element will then depend on growth in how much GDP is produced per worker employed. This is the growth in productivity, and while more difficult to forecast, we have historical numbers which can provide a sense for what its growth might be, at best, going forward. The chart at the top of this post shows what it has been since 1947, and will be discussed in detail below. Forecasts that productivity will now start to grow at rates that are historically unprecedented need to be viewed with suspicion. Miracles rarely happen.

I should also be clear that the question being examined is the maximum rate at which one can expect GDP to grow. That is, we are looking at growth in what economists call capacity GDP. Capacity GDP is what could be produced in the economy with all resources, in particular labor, being fully utilized. This is the full employment level of GDP, and the economy has been at or close to full employment since around 2015. Actual GDP can be less than capacity GDP when the economy is operating at less than full employment. But it cannot be more. Thus the question being examined is how fast the economy could grow, at most, for a sustained period going forward, not how fast it actually will grow. With mismanagement, such as what was seen in the government oversight of the financial markets (or, more accurately, the lack of such oversight) prior to the financial and economic collapse that began in 2008 in the final year of the Bush administration, the economy could go into a recession and actual GDP will fall below capacity GDP. But we will give Trump the benefit of the doubt and look at how fast capacity GDP could grow at, assuming the economy can and will remain at full employment.

We will start with a look at what is expected for growth in the labor force and hence in the number of workers who can be employed. That is relatively straightforward, and the answer is not to expect much possible growth in GDP from this source. We will then look at productivity growth: what it has been in the past and whether it could grow at anything close to what is implicit in the Trump administration forecasts. Predicting what that actual rate of productivity growth might be is beyond the scope of this blog post. Rather, we will be looking at it whether it can grow as fast as is implied by the Trump forecasts. The answer is no.

B. Growth in the Labor Force

Every two years, the Bureau of Labor Statistics provides a detailed ten-year forecast of what it estimates the US labor force will be. The most recent such forecast was published in December 2015 and provided its forecast for 2024 (along with historical figures up to 2014). The basic story is that while the labor force is continuing to grow in the US, it is growing at an ever decreasing rate as the population is aging, the baby boom generation is entering into retirement, and decades ago birth rates fell. The total labor force grew at a 1.2% annual rate between 1994 and 2004, at a 0.6% rate between 2004 and 2014, and is forecast by the BLS to grow at a 0.5% rate between 2014 and 2024.

But it is now 2017. With a decelerating rate of growth, a growth rate in the latter part of a period will be less than in the early part of a period. Taking account of where the labor force is now, growth going forward to 2024 will only be 0.3% (with these figures calculated based on the full numbers before round-off). This is not much.

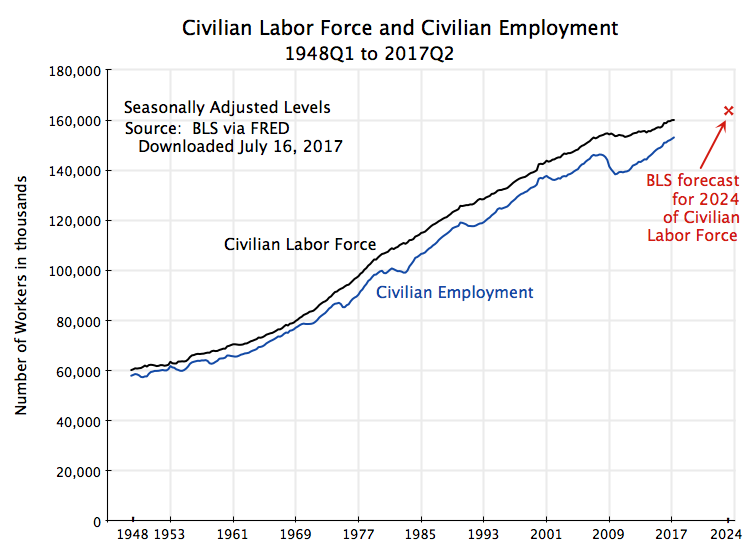

A plot of the US civilian labor force going back to 1948 puts this in perspective:

The labor force will be higher in 2024 than it is now, but not by much. The labor force grew at a relatively high rate from the 1950s to the 1970s (of a bit over 2% a year), but then started to level off. As it did, it continued to grow but at an ever slower rate. There was also a dip after the economic collapse of 2008/09, but then recovered to its previous path. When unemployment is high, some workers drop out of the labor force for a period. But we are now back to what the path before would have predicted. If the BLS forecasts are correct, growth in the labor force will continue, but at a rate of just 0.3% from where it is now to 2024, to the point shown in red on the chart. And this is basically a continuation of the path followed over the last few decades.

One should in particular not expect the labor force to get back to the rapid growth rate (of over 2% a year) the US had from the 1950s to the 1970s. This would require measures such as that immigration be allowed to increase dramatically (which does not appear to enjoy much support in the Trump administration), or that grandma and grandpa be forced back into the labor force in their 70s and 80s rather than enjoy their retirement years (where it is not at all clear how this would “make America great again”).

I have spoken so far on the figures for the labor force, since that is what the BLS and others can forecast based largely on demographics. Civilian employment will then be some share of this, with the difference equal to the number of unemployed. That curve is also shown, in blue, in the chart. There will always be some unemployment, and in an economic downturn the rate will shoot up. But even in conditions considered to be “full employment” there will be some number of workers unemployed for various reasons. While economists cannot say exactly what the “full employment rate of unemployment” will be (it will vary over time, and will also depend on various factors depending on the make-up of the labor force), it is now generally taken to be in the range of a 4 to 5% unemployment rate.

The current rate of unemployment is 4.4%. It is doubtful it will be much lower than this in the future (at least not for any sustained period). Hence if the economy is at full employment in 2024, with unemployment at a similar rate to what it is now, the rate of growth of total employment from now to 2024 will be the same as the rate of growth of the labor from now to then. That is, if unemployment is a similar share of the total labor force in 2024 as it is now, the rates of growth of the labor force and of total employment will match. And that rate of growth is 0.3% a year.

This rate of growth in what employment can be going forward (at 0.3%) is well below what it was before. Total employment grew at an annual rate of 2.1% over the 20 years between 1947 and 1967, and a slightly higher 2.2% between 1967 and 1987. With total employment able to grow only at 1.8 or 1.9% points per annum less than what was seen between 1947 and 1987, total GDP growth (for any given rate of productivity growth) will be 1.8 or 1.9% points less. This is not a small difference.

C. Growth in Productivity

Growth in productivity (how much GDP is produced per worker employed) is then the other half of the equation. What it will be going forward is hard to predict; economists have never been very good at this. But one can get a sense of what is plausible based on the historical record.

The chart below is the same as the one at the top of this post, but with the growth rates over 20 year periods from 1947 (10 years from 2007) also shown:

These 20 year periods broadly coincide with the pattern often noted for the post-World War II period for the US: Relatively high growth (2.0% per year) from the late 1940s to the late 1960s; a slowdown from then to the mid 1980s (to 0.9%); a return to more rapid growth in productivity in the 1990s / early 2000s, although not to as high as in the 1950s and 60s (1.5% for 1987 to 2007); and then, after the economic collapse of 2008/2009, only a very modest growth (0.8% for 2007 to 2017, but much less from 2010 onwards).

Note also that these break points all coincide, with one exception (1987), with years where the economy was operating at full employment. In the one exception (1987, near the end of the Reagan administration) unemployment was still relatively high at 6.6%. While one might expect productivity levels to reach a local peak when the economy is at or close to full employment, that is not always true (the relationship is complex), and is in any case controlled for here by the fact the break points coincide (with the one exception) with full employment years.

Another way to look at this is productivity growth as a rolling average, for example over continuous 10 year periods:

Productivity, averaged over 10 year periods, grew at around 2% a year from the late 1940s up to the late 1960s. It then started to fall, bottoming out at roughly 0.5% in the 1970s, before reverting to a higher pace. It reached 2% again in the 10 year period of 1995 to 2005, but only for a short period before starting to fall again. And as noted before, it fell to 0.8% for the 2007 to 2017 period.

What productivity growth going forward could at most be will be discussed below, but first it is useful to summarize what we have seen so far, putting employment growth and productivity growth together:

|

Growth Rates |

Employment |

GDP per worker |

GDP |

|

1947-1967 |

2.1% |

2.0% |

4.1% |

|

1967-1987 |

2.2% |

0.9% |

3.1% |

|

1987-2007 |

1.6% |

1.5% |

3.1% |

|

2007-2017 |

0.6% |

0.8% |

1.4% |

Employment grew at over 2% a year between the late 1940s and 1987. This was the period of the post-war recovery and baby boom generation coming of working age. With GDP per worker growing at 2.0% a year between 1947 and 1967, total GDP grew at a 4.1% rate. It still grew at a 3.1% rate between 1967 and 1987 despite productivity growth slowing to just 0.9%, as the labor force continued to grow rapidly over this period. And total GDP continued to grow at a 3.1% rate between 1987 and 2007 despite slower employment (and labor force) growth, as a recovery in productivity growth (to a 1.5% pace) offset the slower availability of labor.

It might, at first glance, appear from this that a return to 3% GDP growth (or even 4%) is quite doable. But it is not. Employment growth fell to a pace of just 0.6% between 2007 and 2017 (and the unemployment rates were almost exactly the same in early 2007, at 4.5%, and now, at 4.4%, so this matched labor force growth). Going forward, as discussed above, the labor force is forecast to grow at a 0.3% pace between now and 2024. To get to a 3% GDP growth rate now at such a pace of labor growth, one would need productivity to grow at a 2.7% pace. To get a 4% GDP growth, productivity would have to grow at a 3.7% pace. But productivity growth in the US since 1947 has never been able to get much above a 2% pace for any sustained period. To go well beyond this would be unprecedented.

D. Why Does This Matter? And What Can Be Achieved?

Some readers might wonder why all this matters. On the surface, the difference between growth at a 2% rate or 3% rate may not seem like much. But it is, as some simple arithmetic illustrates:

|

Alternative Growth Scenarios |

Growth Rates: | ||

|

GDP |

Population |

GDP per capita |

Cumulative Over 30 years |

|

1.0% |

0.8% |

0.2% |

6% |

|

2.0% |

0.8% |

1.2% |

43% |

|

3.0% |

0.8% |

2.2% |

91% |

|

4.0% |

0.8% |

3.2% |

155% |

This table works out the implications of varying rates of hypothetical GDP growth, between 1.0% and 4.0%. Population growth in the US is forecast by the Census Bureau at 0.8% a year (for the period to the 2020s). It is higher than the forecast pace of labor force growth (of 0.3% in the BLS figures) primarily because of the aging of the population, so a higher and higher share of the adult population is entering their retirement years.

The result is that GDP growth at 1.0% a year will be just 0.2% a year in per capita terms with a 0.8% population growth rate. After 30 years (roughly one generation) this will cumulate to a total growth in per capita income of just 6%. But GDP growth at 2% a year will, by the same calculation, cumulate to total per capita income growth of 43%, to 91% with GDP growth of 3%, and to 155% with GDP growth of 4%. These differences are huge. What might appear to be small differences in GDP growth rates add up over time to a lot. It does matter.

[Note that this does not address the distribution issue. Overall GDP per capita may grow, as it has over the last several decades, but all or almost all may go only to a few. As a post on this blog from 2015 showed, only the top 10% of the income distribution saw any real income growth at all between 1980 and 2014 – real incomes per household fell for the bottom 90%. And the top 1%, or richer, did very well.

But total GDP growth is still critically important, as it provides the resources which can be distributed to people to provide higher standards of living. The problem in the US is that policies followed since 1980, when Ronald Reagan was first elected, have led to the overwhelming share of the growth the US has achieved to go to the already well off. Measures to address this critically important, but separate, issue have been discussed in several earlier posts on this blog, including here and here.]

Looking forward, what pace of productivity growth might be expected? As discussed above, while the US was able to achieve productivity growth at a rate of about 2.0% in the 1950s and 1960s, since then it was able to achieve a rate as high as this over a ten year period only once (between 1995 and 2005), and only very briefly. And over time, there is some evidence that reaching the rates of productivity growth enjoyed in the past is becoming increasingly difficult.

A reason for this is the changing structure of the economy. Productivity growth has been, and continues to be, relatively high in manufacturing and especially in agriculture. Mechanization and new technologies (including biological technologies) can raise productivity in manufacturing and in agriculture. It is more difficult to do this in services, which are often labor intensive and personal. And with agriculture and manufacturing a higher share of the economy in the past than they are now (precisely because their higher rates of productivity growth allowed more to be produced with fewer workers), the overall pace of productivity growth in the economy will move, over time, towards the slower rate found in services.

The following table illustrates this. The figures are taken from an earlier blog post, which looked at the changing shares of the economy resulting from differential rates of productivity growth.

|

Productivity Growth |

Agriculture |

Manufacturing |

Services |

Overall (calculated) |

|

1947 to 2015: |

3.3% |

2.8% |

0.9% |

1.4% |

|

At GDP Shares of: |

||||

|

– 1947 shares |

8.0% |

27.7% |

64.3% |

1.7% |

|

– 1980 shares |

2.2% |

23.6% |

74.2% |

1.4% |

|

– 2015 shares |

1.0% |

13.9% |

85.2% |

1.2% |

The top line (with the figures in bold) shows the overall rates of productivity growth between 1947 and 2015 in agriculture (3.3%), manufacturing (2.8%), services (0.9%), and overall (1.4%). The overall is for GDP, and matches the average for growth in GDP per employed worker between 1947 and 2017 in the chart shown at the top of this post.

The remaining lines on the table show what the pace of overall productivity growth would then have been, hypothetically, at these same rates of productivity growth by sector but with the sector shares in GDP what they were in 1947, or in 1980, or in 2015. In 1947, with the sector shares of agriculture and manufacturing higher than what they were later, and services correspondingly lower, the pace of productivity growth overall (i.e. for GDP) would have been 1.7%. But at the sector shares of 2015, with services now accounting for 85% of the economy, the overall rate of productivity growth would have been just 1.2%, or 0.5% lower.

This is just an illustrative calculation, and shows the effects of solely the shifts in sector shares with the rates of productivity growth in the individual sectors left unchanged. But those individual sector rates could also change over time, and did. Briefly (see the earlier blog post for a discussion), the rate of productivity growth in services decelerated sharply after the mid-1960s; the pace in agriculture was remarkably steady; while the pace in manufacturing accelerated after the early 1980s (explaining, to a large extent, the sharp fall in the manufacturing share of the economy from 24% in 1980 to just 14% in 2015). But with services dominating the economy (74% in 1980, rising to 85% in 2015), it was the pace of productivity growth in services, and its pattern over time, which dominated.

What can be expected going forward? The issue is a huge one, and goes far beyond what is intended for this post. But especially given the headwinds created by the structural transformation in the economy of the past 70 years towards a dominance by the services sector, it is unlikely that the economy will soon again reach a pace of 2% productivity growth a year for a sustained period of a decade or more. Indeed, a 1.5% rate would be exceptionally good.

And with labor force growth of 0.3%, a 1.5% pace for productivity would imply a 1.8% rate for overall GDP. This is well below the 3% rate that the Trump administration claims it will achieve, and of course even further below the 4% (and 5% and 6%) rates that Trump has claimed he would get.

E. Conclusion

As a simple identity, GDP will equal GDP per worker employed (productivity) times the number of workers employed. Growth in GDP will thus equal the sum of the growth rates of these two components. With a higher share of our adult population aging into the normal retirement years, the labor force going forward (to 2024) is forecast to grow at just 0.3% a year. That is not much. Overall GDP growth will then be this 0.3% plus the growth in productivity. That growth in the post World War II period has never much exceeded 2% a year for any 10-year period. If we are able to get to such a 2% rate of productivity growth again, total GDP would then be able to grow at a 2.3% rate. But this is below the 3% figure the Trump administration has assumed for its budget, and far below the 4% (or 5% or 6%) rates Trump has asserted he would achieve. Trump’s forecasts (whether 3% or 4% or 5% or 6%) are unrealistic.

But a 2% rate for productivity growth is itself unlikely. It was achieved in the 1950s and 1960s when agriculture and manufacturing were greater shares of the economy, and it has been in those sectors where productivity growth has been most rapid. It is harder to raise productivity quickly in services, and services now dominate the economy.

Finally, it is important to note that we are speaking of growth rates in labor, productivity, and GDP over multi-year, sustained, periods. That is what matters to what living standards can be achieved over time, and to issues like the long-term government budget projections. There will be quarter to quarter volatility in the numbers for many reasons, including that all such figures are estimates, derived from surveys and other such sources of information. It is also the case that an exceptionally high figure in one quarter will normally soon be followed by an exceptionally low figure in some following quarter, as the economy, as well as the statistical measure of it, balances out over time.

Thus, for example, the initial estimate (formally labeled the “advance estimate”) for GDP growth in the second quarter of 2017, released on July 28, was 2.6% (at an annual rate). Trump claimed this figure to be “an unbelievable number” showing that the economy is doing “incredibly well”, and claimed credit for what he considered to be a great performance. But it is a figure for just one quarter, and will be revised in coming months as more data become available. It also follows an estimate of GDP growth in the first quarter of 2017 of just 1.2%. Thus growth over the first half of the year averaged 1.9%. Furthermore, productivity (GDP per worker) grew at just a 0.5% rate over the first half of 2017. While a half year is too short a period for any such figure on productivity to be taken seriously, such a performance is clearly nothing special.

The 1.9% rate of growth of GDP in the first half of 2017 is also nothing special. It is similar to the rate achieved over the last several years, and is in fact slightly below the 2.1% annual rate seen since 2010. More aptly, in the 28 calendar quarters between the second quarter of 2010 and the first quarter of 2017, GDP grew at a faster pace than that 2.6% estimated rate a total of 13 times, or almost half. The quarter to quarter figures simply bounce around, and any figure for a single quarter is not terribly meaningful by itself.

It therefore might well be the case that a figure for GDP growth of 3%, or even 4% or higher, is seen for some quarter or even for several quarters. But there is no reason to expect that the economy will see such rates on a sustained basis, as the Trump administration has predicted.

You must be logged in to post a comment.