Source: Wikipedia – Super heavy-lift launch vehicle

A. Introduction

SpaceX is currently developing a truly gigantic rocket it has named Starship. It would be revolutionary. Not only would it lift a heavier payload than the Saturn V, the rocket that took Apollo to the Moon and until now the heaviest lift launch vehicle that has successfully flown, but Starship is also being designed to be fully reusable. Both the first stage and the orbiter would fly back to the launch pad, where they each would be caught in mid-air as they land by arms extending from the launch tower. They would then be refueled and after minimal reinspection be able to take off again, within hours. And each flight would cost only $2 million.

If all this works as intended. And that remains to be seen. But there are good reasons to believe it will, eventually.

It is certainly likely that there will be explosions or other causes of failure in the early orbital test flights now upcoming, and that even once operational the turn-around time will at first be a good deal longer than a few hours and the cost a good deal more than $2 million for a flight. But even a cost that is ten times higher would still be incredibly cheap for such a lift capacity. Indeed, it would still be cheap at one hundred times that cost. And the iterative process SpaceX follows of testing to failure, learning from the test, redesigning to address the problems found, and then testing to failure again, is a process that has allowed SpaceX to work through to a successful design. It took several years of such tests before the first stage of the Falcon 9 rocket of SpaceX was successfully flown back to the launch site (or to a platform on a drone ship in the ocean) and landed, and then reused after some refurbishment. But eventually, after a number of test failures, SpaceX worked out how to do this. It is now routine. And prior to SpaceX demonstrating this technology, the established view was that this would be basically impossible for an orbital launch vehicle.

Furthermore, in April 2021 NASA awarded SpaceX a close to $3 billion contract to build a variant of the Starship orbiter that would carry NASA astronauts from lunar orbit to the surface of the Moon and back. It did this following a year of NASA engineers closely examining the SpaceX proposal (along with competing proposals from two others), reviewing the Starship plans with full access to all the technical information and to the development and testing plans. NASA concluded the SpaceX Starship system could be relied upon to deliver on its proposal. This is a tremendously important vote of confidence in the Starship system.

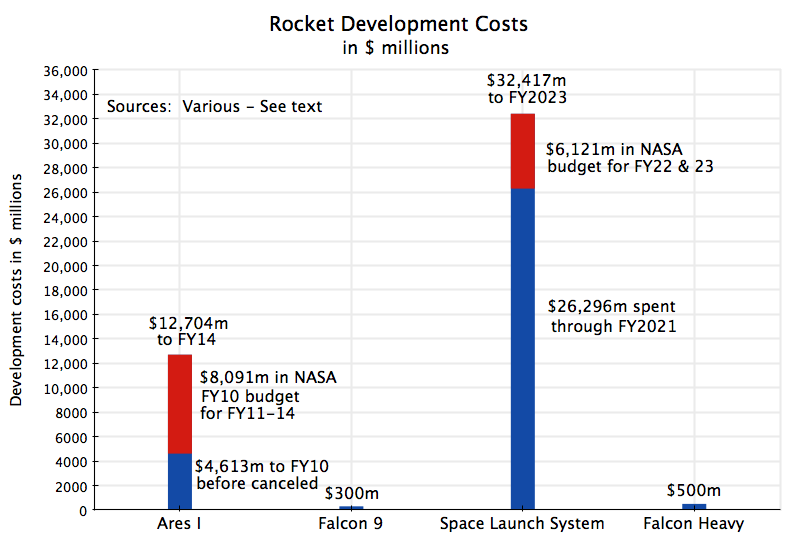

This post will first review the Starship system and what it promises to deliver. It is really pretty astounding. The big question is whether it will work, and that remains to be seen. But the post will review the development process SpaceX is following, and contrast that with the sharply different process NASA is following with its Space Launch System (SLS) rocket. The SLS, with its high cost and long delays, was discussed in some detail in an earlier post of this blog. The contrasts in the approaches taken are stark. The SLS will be a similarly sized rocket as Starship (a bit smaller), but has followed a very different design and development process. Development began in 2011, with a design where the major components (the engines and the solid-fuel boosters strapped on the side) were the same as those used on the Space Shuttle or from other existing sources. This should have saved both time and expense. Yet despite this, there has yet to be a test flight of the SLS even though it is now more than ten years later. The much delayed first flight is now scheduled (as I write this) for February 2022 (and had been set as November 2021 just a few months ago), and it is expected that recently discovered problems will delay this further. Hopefully that first (and only planned) test flight will succeed. If it does not, it is not at all clear what will happen to NASA’s plans to return to the Moon under the Artemis program. As discussed in my earlier post, each SLS costs $2 billion to build, and under current production plans a second one will not be available for another two years in any case.

The Starship system that NASA has chosen to carry crew to the Lunar surface and back is also quite astounding. This post will review what it would be able to do, and contrast this with the two competing proposals that NASA considered – the proposal from a team with Blue Origin (owned by Jeff Bezos) in the lead and one with the firm Dynetics in the lead. The contrast is huge, where the SpaceX Starship proposal would deliver far more in several different dimensions (and at far lower cost).

The capabilities of the Starship also immediately raise the question of whether NASA should make use of it in a total revamp of its Artemis program to return astronauts to the Moon. Instead of stuffing the crew into the relatively tiny Orion capsule for the trip from the Earth to lunar orbit, launched on an SLS that costs $2 billion per launch, why not use what would otherwise be an empty Lunar Starship for the journey? The Lunar Starship will not only have all the life support systems needed by the crew for a multi-week journey, but the fully furbished habitable volume on the Lunar Starship is over 1,000 cubic meters, vs. just 9 cubic meters in the Orion capsule. Certain technical issues would of course need to be worked out, but that should not be an insurmountable obstacle.

There likely will be obstacles, however, but political ones rather than technical ones. This post will conclude with a discussion of those issues. In my earlier blog post, I estimated that just for the period from when the programs started to what is planned by FY2023, Congress will have appropriated and NASA will have spent a total of $21.8 billion on the Orion capsule and a total of $32.4 billion on the SLS, for a total of $54.2 billion on them together. It would be embarrassing, to say the least, to recognize that they turn out not to be needed, and that the SpaceX Starship system would not only be far less expensive but also far more capable. And politicians do not appreciate being embarrassed. While the politicians have asserted that they have been funding these programs to achieve certain space exploration goals, what appears to have driven the support of a number of the key Senators and Congressmen on the committees that set the NASA budget has been less the space exploration goals and more the resulting number of well-paid jobs in their constituencies. Seen in this light, the high cost of the SLS / Orion systems is not a flaw but a feature.

But this is not sustainable. How much the US government will spend on space exploration is limited, and treating it as a jobs program will mean national goals will either be long delayed or never met at all. And while private companies such as SpaceX can help NASA achieve national goals (faster and at lower cost), they can only help if they are used to help. Congress has often been opposed, with both Democrats and Republicans unfortunately aligned on this. China is now moving fast in its space exploration program, and NASA may soon be left far behind if Congressional priorities do not change.

B. The SpaceX Starship, and the SpaceX Approach to Development and Testing

SpaceX is currently developing, and actively testing, the extremely large rocket it has named Starship. If it works, it will be revolutionary. Starship will be huge – larger than the Saturn V as well as the SLS – and capable of delivering to low earth orbit a payload of 100,000 kg initially with this expected to grow to 150,000 kg or more as it is further developed.

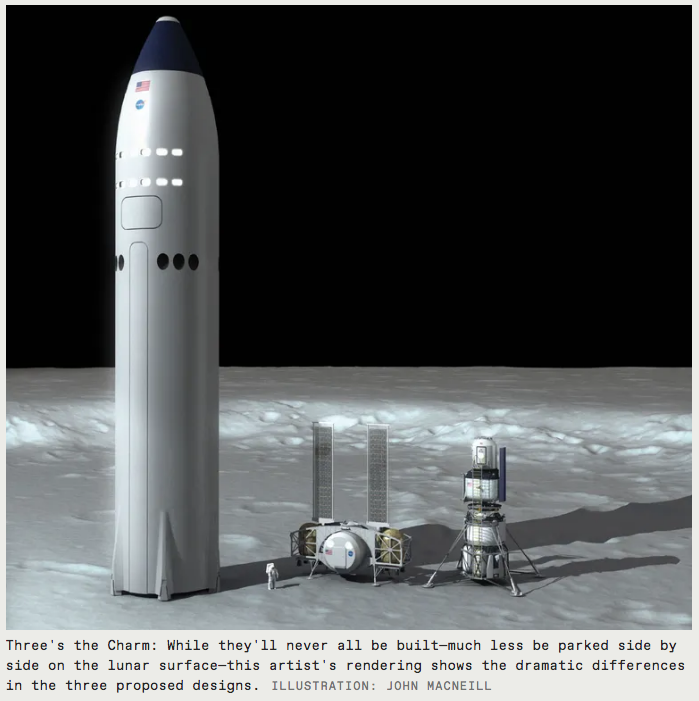

The diagram at the top of this post shows Starship in comparison to other heavy-lift vehicles to give you a sense of its size. It is huge. And while the design is still evolving as its testing program proceeds (with the version of Starship shown in the diagram from a year or two ago), its basic dimensions will remain the same. The Saturn V is well known, and is the heaviest-lift launch vehicle that has ever flown. The SLS Block 1 will be the initial version of the SLS, with its first flight test now planned for 2022. The SLS Block 2 Cargo is a planned follow-on SLS variant – still to be developed – that would have the heaviest lift capacity of the SLS series if it is ever built. Finally, the N1 launch vehicle was developed, in secrecy at the time, in the USSR in the 1960s to carry its cosmonauts to the Moon. There were four tests between 1969 and 1972. Each failed with an explosion, and the especially spectacular explosion on the second test on July 3, 1969 – just 13 days before the launch of Apollo 11 – has been estimated to have been comparable in magnitude to that of the nuclear bomb dropped on Hiroshima. It was the biggest man-made non-nuclear explosion in history.

The SpaceX Starship will be a two-stage vehicle, with a first stage (named the Super Heavy) that will have a thrust at take-off that is more than double what it was on the Saturn V. The first stage will initially use 33 of the newly-developed engines named Raptor, but that number might later rise to as many as 37. The engines burn liquid methane with liquid oxygen. The second stage will be powered by 6 Raptor engines (three optimized for burning in the vacuum of space and three for operation at ground level), with the spacecraft carrying the cargo and/or crew fully integrated into it. Confusingly, this second stage/spacecraft has been named Starship, which is also the name of the whole rocket including the first stage Super Heavy booster. To ease possible confusion, some refer to the second stage/spacecraft as the “Orbital Starship”, and I will as well. The Orbital Starship would come in several variants, with vehicles just for cargo (Cargo Starship), for a human crew (Crew Starship), and to serve as a fuel depot in space (Fuel Depot Starship). And as will be discussed in more detail below, NASA has extended a contract to SpaceX to build a variant that will take an astronaut crew to the Lunar surface and back (Lunar Starship).

Importantly, all components of Starship will be fully reusable, with the plan that there would be just minimal to no maintenance required between launches. The Super Heavy booster would return to the launch site and relight some subset of its engines for a soft landing. Indeed, as noted above, the plan is that it would come down precisely at the launch tower, where two extended arms on the tower would catch it as it (slowly) comes down. No landing legs would be required.

The Orbital Starship would also be fully reusable. It will have heat shield tiles that are chemically very similar to those used on the Space Shuttle, along with wing flaps and tail (see the drawing above) to guide the Orbital Starship as it re-enters the atmosphere and then lands. A restart of a subset of the engines near the end will allow for a soft landing. And as with the Super Heavy, the plan is for it to return to the launch tower to be caught as it comes down by the two large arms. The plan (and hope) then is that the Starship and Super Heavy could be re-attached, refueled, and launched again within hours, with just minimal inspection required to ensure all was fine.

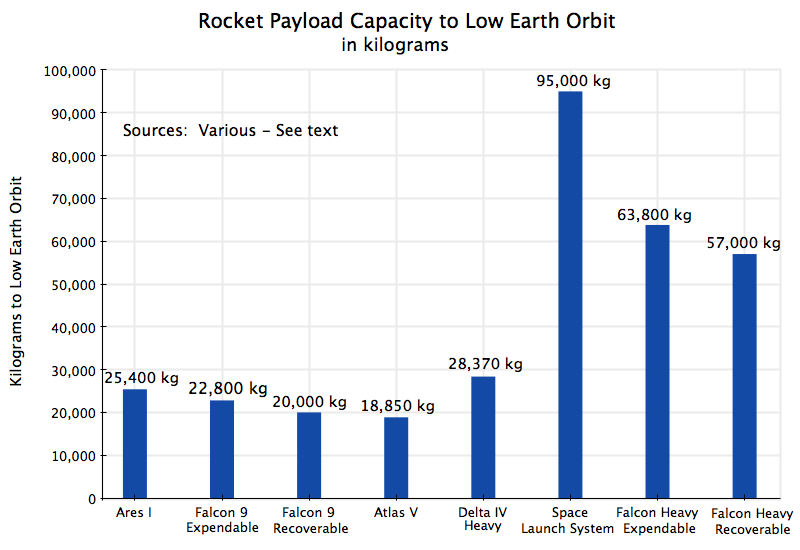

The payload will also be huge. The immediate design goal is a payload to low Earth orbit of 100 tons. This would be more than the SLS (95 tons in the initial, Block 1, version), although less than the Saturn V (140 tons). But SpaceX plans to raise the payload capacity relatively soon to 150 tons through various means, and some have argued it might grow to even more. As noted above, the number of Raptor engines on the first test flight will be 33, but may eventually be increased to 37. Elon Musk (in a tweet on Twitter in July 2021) also mentioned the possibility that the number of Raptor engines on the Orbital Starship might be increased from six to nine at some point. The additional three would all be the Vacuum Raptor variant. This flexibility that has been built into the design of the Starship system – where adding core engines does not necessitate a complete revamping – is really quite remarkable.

The power of each engine will also soon be raised. The Raptor 2 engine, which is already now starting to be produced, will have 230 or more tons of force – a big increase over the 185 tons of force in the first version of the engine that has been on the test flights thus far. SpaceX also has a history of upgrading the performance of its rockets over time. The initial version 1.0 of the Falcon 9 rocket could carry a payload to low Earth orbit of 9.0 tons. But this rose to 22.8 tons in the Block 5 model that is now standard (22.8 tons when the booster is expended, or 16.8 tons when the booster is recovered). That is, the Falcon 9 can now carry to orbit 2 1/2 times what it could when it first flew.

Will Starship work? That remains to be seen, but testing is underway and there are reasons to be optimistic. As I write this in December 2021, there have been seven test flights, all (so far) of the Starship upper stage, with simple up and down flights of up to 12.5 kilometers and a landing attempt on each. There were a series of sometimes spectacular crashes (or as SpaceX calls them, RUDs, for Rapid Unscheduled Disassemblies), but the seventh (and hence final flight of the series) was fully successful, so they have moved on. The plan now is to conduct a first test of the full Starship, with the Super Heavy plus the Orbital Starship launching from the SpaceX base in Boca Chica, Texas (on the Gulf of Mexico at the border with Mexico). The first test would be of an almost orbital flight (more than 80% of what a full orbit would be) to land about 100 kilometers northwest of Kauai in the Hawaiian Islands. The Super Heavy would return most of the way to the Boca Chica base but come down softly in a “landing” in the waters of the Gulf of Mexico around 20 kilometers off the coast on this first try. The Orbiter Starship would come down through the atmosphere, testing its heat shield in particular, to “land” in the waters of the Pacific.

It will be an ambitious first test of the complete rocket, and the likelihood of everything working right the first time is low. But this is in keeping with the SpaceX development and testing approach (to be further discussed below), which is to test early and often, and then iterate on the designs until they work. While no date has been publicly announced for this first test (SpaceX is a private company and under no obligation to announce this), the indications are that the aim is for a first flight sometime early in 2022. However, this will depend on SpaceX receiving necessary permits (related to environmental and safety issues) from the FAA, and it is not clear as I write this when this process will be completed. While SpaceX ignored this requirement on one of the early test flights of Starship, it is now on notice from the FAA and it is doubtful they will ignore them again.

Update on April 21, 2023: The first test flight of Starship did not take place early in 2022, but rather on April 20, 2023 – more than a year later. To no one’s surprise, Starship did not complete the full flight plan but rather had to be destroyed using a self-destruct mechanism when it started to spin uncontrollably at about four minutes into the flight (having reached an altitude of about 39 kilometers). The causes of the failure are now being examined, but one issue that was immediately obvious was that several of the Raptor engines failed to light up, with six eventually going out (leaving only 27 of the 33 firing). While Starship has been designed to be able to function with some of the engines out, this may have grown to be too many. The imbalances created may have grown to be greater than the Super Heavy booster could compensate for, thus leading to the spin.

But as discussed in this post, this is precisely the iterative process SpaceX has used to determine where unforeseen problems are, so that they can then work out how to fix them. There will be more such test flights – probably many more – until all the kinks are worked out of the system. When that next test flight will be is impossible to know at this point. The SpaceX team will need to determine what caused the failure this time and then work out how to fix it. Furthermore, there has clearly been substantial damage done to the concrete around the launch pad, with major debris then scattered for miles. The pad will not only need to be repaired, but they will also need to work out how to minimize such damage on future launches. A flame diverter system was already planned but not yet installed, but they may well decide that what had been planned might not suffice. Changes may need to be made.

Despite all this, the first launch of Starship should be considered a success. They have learned a good deal.

As noted before, if the design works it would be revolutionary. It would be fully reusable, with both the first (Super Heavy) and second (Orbital Starship) stages returning not simply to a base but to the very launch tower where they would be caught in mid-air. Probably the biggest question mark is whether the heat shield that covers one side of the Orbital Starship will prove to be durable and quickly reusable with no maintenance required. As noted above, the chemical composition of the material is similar to that used on the heat shield for the Space Shuttle. But on the Space Shuttle, extensive checks and maintenance of the heat shields proved to be necessary after each flight, with this a major contributor to the high cost of the Shuttle. The original plan (and hope) was that a Space Shuttle could be turned around and flown again within two weeks of its landing from its preceding flight. This proved impossible. In the later years of the Shuttle program, each operational Shuttle was generally flying only once a year.

SpaceX has learned and applied important lessons from the experience with the Space Shuttle, and has addressed the heat shield tile issues in two important ways. First, while most of the over 21,000 heat shield tiles on each Space Shuttle Orbiter had to have a unique shape due to the shape of the Shuttle, most (although not all) of the tiles on the Starship Orbiter will have a standard, hexagonal, shape. This will make them far easier to replace when needed, as a new, custom-molded, tile will not (normally) need to be made each time. And second, the tiles on the Starship Orbiter will be attached to built-in spikes on the body of the Starship, rather than attached with just a special glue. It is hoped this will make them more durable.

If a fully and rapidly reusable design can be made to work, the cost of each flight of the Starship will be incredibly low. Elon Musk has said that the fuel would cost only about $900,000 on each flight, and with the other operational costs the total would only be about $2 million per flight This might well be optimistic (Elon Musk often is), but even if it is, say, ten times higher at $20 million per flight, then with a 100,000 kg payload the cost per kilogram will be roughly one-hundredth of the cost per kilogram of a launch on the similarly sized SLS. And it will be roughly one-tenth of the cost per kilogram of launching on the current lowest-cost launcher – the Falcon Heavy. And if it truly works out to be $2 million per launch, then the cost will be one-thousandth of what it would cost on the SLS. This is all pretty incredible – if it works.

The development cost will also be far below what it has cost NASA to develop its similarly sized SLS. As discussed in the earlier blog post, the cost of developing the SLS will have reached over $32 billion by FY2023. While the cost of developing the Starship has not been published (SpaceX is a private company), and indeed as not is known by anyone what in the end it might be as development is still underway, Elon Musk has said in an interview that he expects it will come to about $5 billion to complete. If that turns out to be the case, that would be less than one-sixth the cost of the SLS. And while it is not clear whether the $5 billion includes the cost of including a section of the Starship to house the crew, if it does then for comparability the cost of developing the Starship with the crew quarters should be compared to the cost of SLS and Orion together That will total over $54 billion – $32.4 billion for the SLS plus $21.8 billion for Orion. That would be ten times higher than the cost of developing a crew capable Starship, if the $5 billion estimate for Starship turns out to be correct.

But the design remains to be proved. While the first test flight will be important, the odds are high that there will be a failure at some point during that test. As long as the Starship manages not to explode on the launch pad (with the damage that would cause to the launch pad) the flight should be considered a success. Valuable information will have been obtained. Particularly valuable, if it gets to that point, will be information on how well the heat shield holds up on re-entry.

The process followed by SpaceX is iterative. A design is developed, a prototype is built, and it is then quickly tested – to the point of failure to see how much it can do. Alterations are then made in response to what did not work in the test, with the revised design then soon tested again to take it to the next stage. Failures are common and indeed expected. Musk has noted that if failures did not occur, then you were not pushing it far enough.

Importantly also with this approach to development, manufacturing methods need to be developed to allow that frequent testing to the point of failiure to be at a cost per test that is not high. As Musk noted in a tweet in February 2020:

“Hardest problem by far is building the production system of something this big. … Building many rockets allows for successive approximation. Progress in any given technology is simply # of iterations * [times] progress between iterations.”

This would then also drive design decisions. For example, and directly counter to the conventional wisdom, the Starship hull and tanks are made of stainless steel. Steel is seen as heavy – not good for a flying vehicle – and almost all rockets and spacecraft have been made of aluminum. In the initial design, Starship was to be made of advanced carbon fiber. Carbon fiber is light and can be made to be strong, but for several reasons the decision was made to switch to stainless steel. Prominent among them was that stainless steel is relatively easy to work with – it can be bent or reshaped when needed for a design change – plus it is cheap. As Musk noted in an interview in January 2019 (just after they announced Starship would be made of steel rather than carbon fiber), the type of stainless steel they need costs only about $3 per kg, vs. $135 per kg for carbon fiber. Furthermore, there is about 35% wastage when one works with carbon fiber, so the true cost per ton for carbon fiber is over $200 per ton. Any scrap from the stainless steel can be melted down and used.

There are also other advantages to steel, including its far higher melting point (which means less depends on the heat shield tiles, and they can then be made both simpler and lighter). But the flexibility provided by using a relatively inexpensive and easily worked material is key in the SpaceX iterative development approach with its frequent testing and then redesign.

The decision to switch to stainless steel from the original plan to use carbon fiber also illustrates the flexibility in the overall approach followed by SpaceX. Elon Musk’s first public announcement of his intention to build what evolved into Starship was made in November 2012. The Raptor engines that would power the rocket were already being tested on NASA test stands in 2014. The initial design, then at a 12-meter diameter, was revealed in September 2016. This was then changed dramatically, to a 9-meter diameter design, in September 2017. Through this point, the rocket would have been made of carbon fiber. But then in December 2018, Musk revealed they had decided to switch to stainless steel for the reasons noted above. And then just four months later, in April 2019, they were already conducting their first flight tests of what they called the Starhopper vehicle. These were tests basically of the Raptor engine, the use of the engine to allow for a soft landing (and the controls required for this), and the stainless steel design. The Starhooper test vehicle was tethered for its first “flight” on April 3, 2019 and it rose just one foot. They then took it to one meter two days later on April 5. The first untethered flight was in July 2019 to 20 meters, and the final test was in August 2019 when it rose to 150 meters and moved sideways for a short distance before returning to land softly on the ground.

There were then a series of seven tests of what became increasingly similar to the Orbital Starship starting just one year later, between August 2020 and May 2021. The test vehicle had just one Raptor engine for the first two tests (rising just to 150 meters, and then landing) and then three Raptors in the subsequent tests (where it rose to a height of up to 12.5 km before returning to the pad to try to land). After a few spectacular crashes and explosions, the Starship had a clean landing at the pad on the seventh and hence final flight. There were modifications made following each test flight, fixing what went wrong, and they got it right by the seventh such flight.

The iterative SpaceX approach is in sharp contrast to that used by NASA in its development of the far more costly SLS. As noted before, there has not yet been even one flight test of the SLS design, with the first now scheduled for February 2022 but most likely until sometime later due to recent issues being discovered. Yet it has been under development since 2011, and arguably from before as the SLS design has many similarities with the Ares V rocket that at that time was under development (but then superseded by the SLS). And the SLS design is based on existing rocket components, with the four main engines the same as those on the Space Shuttle (the Ares V would have had five of those engines, but otherwise the same). The two solid-fuel side boosters are also taken from the Space Shuttle (and indeed make use of ones left over from the Space Shuttle program for the initial several SLS boosters to be built – but each with five segments rather than four). And the second stage of the initial SLS is taken from that used on recent Delta IV rockets.

Drawing from existing rocket components is not necessarily wrong, as it should have led to lower costs and a shorter development period. It is thus particularly difficult to understand why it has taken so long – with no flight test even after ten years – and why the cost has been so high. In contrast to SpaceX, NASA has followed an approach where great care (and expense) is taken to try to ensure the full and final design is completely right, with few tests of the overall system. Indeed just one test flight is planned for the SLS. If this test fails, it is possible the total program will end. It will depend on whether they can determine whether the cause of the failure can be found and relatively easily fixed. A failure would in any case cause major delays of probably years. A second SLS will not be available for two years (in the current schedule), and it could take longer depending on what they determine was the cause of the failure on the first test. That is a lot riding on just one test, for a program expected to cost over $32 billion.

C. Starship as a System to Land Astronauts on the Moon

1) Introduction

The decision by NASA in April 2021 to select the SpaceX proposal to ferry astronauts from lunar orbit to the surface of the Moon and back was highly significant for several reasons. First, and importantly, it was a clear vote of confidence by NASA management and its technical staff that the Starship system would not only work but would work soon. NASA teams had thoroughly reviewed the proposal of SpaceX (as well as the two competing proposals, from Blue Origin and Dynetics) for more than a year, with full access to the technical teams at SpaceX. As a critical, outside, reviewer seeking to find any holes that there might be in the SpaceX plans, NASA’s conclusion that the SpaceX proposal was doable is of great significance.

Second, the use of Starship for this purpose illustrates well the capabilities Starship will have, once it is operational, for not only such lunar missions but more broadly. It is therefore of interest to examine in some detail what SpaceX is now being contracted to do, how it would work, and what Starship might then be used for, in particular in support of NASA’s goal to return to the Moon and establish a base there. Contrasting the SpaceX proposal for what NASA is calling its “Human Landing System” (or HLS) with the two competing proposals that NASA considered is also of interest as it highlights how uniquely capable the Starship system is in comparison to the best that others can offer.

2) Lunar Starship – The SpaceX Proposal for the HLS

NASA has contracted SpaceX for its Human Landing System, where it would serve as one component of the system NASA would use to return men (and as NASA repeatedly emphasizes in its PR materials, also women and a person of color) to the Moon. Other major components of that system include the Orion spacecraft to carry crew from the Earth to lunar orbit, a “Lunar Gateway” that would be a modest-sized space station in permanent orbit around the Moon and serve as a waystation to transfer crew and cargo to the vehicles that would bring them to the lunar surface, and the SLS rocket that would carry the crew and possibly cargo to lunar orbit from the Earth.

NASA developed this basic plan to return to the Moon in the mid-2010s, with a goal of a first landing back on the Moon by 2028. This time frame was then greatly compressed in 2019 by the Trump administration, with NASA charged with accomplishing this by 2024. Vice President Mike Pence (in his capacity as head of the National Space Council) made the announcement, but stated this was “at the direction of the President”. While the reason for the choice of 2024 was never officially stated, few failed to notice that 2024 would have been the final year of a second Trump term in office, had he not lost the election in 2020.

NASA then modified its plans in accordance with this new mandated schedule. While the new schedule was never realistic, the revised, compressed, schedule did have real impacts on the mission designs and on contracts signed. And while NASA has now finally acknowledged that the 2024 target will not be possible, it is still officially following the plans as drawn up during the Trump presidency. The only change is the first landing on the Moon with a crew would not take place in 2024, as planned before, but in 2025 (which is still far from realistic – several more years should be added). The new NASA Administrator Bill Nelson announced the 2025 date during a press conference in November 2021, and blamed the delay on the seven months lost due to the litigation by Blue Origin protesting the award of the HLS contract to SpaceX (which will be further discussed below). Bill Nelson is a former Democratic Senator from Florida who has long been closely involved with NASA space programs, flew on the Space Shuttle in 1986 as a member of Congress, and was one of the key Senators (along with Republican Senator Shelby of Alabama and others) who wrote into legislation in 2010 the requirement that NASA develop the SLS (discussed further below).

Based on these still official NASA plans (albeit slightly delayed to 2025), NASA would organize the return to the Moon through a series of missions that it has labeled the Artemis program (where Artemis was the twin sister of Apollo in Greek mythology). Specifically:

a) Artemis I: This would be the first, uncrewed, test flight of the SLS together with the Orion capsule, with a scheduled launch date (until recently) of February 2022. It has been repeatedly delayed. The original plan (in 2011) was that the SLS would have flown no later than 2017. And while a new official launch date has not yet been set as I write this, no one expects that it will launch in February, this time due to new problems recently found in a malfunctioning computer for the SLS engines.

When the launch does take place, the SLS would send the unmanned Orion capsule first into Earth orbit and then to the Moon, passing just 60 miles above the lunar surface before entering into a high orbit of 38,000 miles above the Moon. It would spend several days there and then return to Earth, passing again 60 miles from the lunar surface, and then testing its heat shield in the high-speed re-entry to Earth. The entire mission would take several weeks.

b) Artemis II: This would be the first crewed launch of the SLS and Orion. Until recently the official plan was for it to go in 2023, but with the acknowledgment that the first crewed landing on the Moon will not be before 2025, it has been pushed to May 2024. This is still unrealistic. And as the Office of the Inspector General of NASA noted in a recent assessment of the Artemis program, sending a crew on a mission around the Moon on the first flight of the Orion capsule with life support systems in place is an “operational and safety risk”. The life support system has not been included in the Orion capsule being tested on the Artemis I mission to save on cost (and maybe time).

Artemis II would be a ten-day mission, with the SLS first launching the Orion into a high Earth orbit, during which the Orion and its life support systems would be monitored to see whether all is working properly. After about two days it would then be launched to the Moon, but not into lunar orbit. Rather, it would be sent on a fly-by trajectory where it would use lunar gravity to swing around the Moon, in a large figure-8, and then return directly to Earth.

c) Artemis III: This would be the first crewed landing on the Moon, with about one week to be spent on the lunar surface and the whole mission taking about two weeks. The Orion would be launched on the SLS and would go to a very high lunar orbit (what they call a “Near Rectilinear Halo Orbit”, or NRHO). The NRHO will have an apogee of 43,500 miles and a perigee of 1,900 miles, and just one orbit will take seven Earth days.

The original plan was that the Lunar Gateway would have been prepositioned in this orbit to serve as a staging area where the Orion would unload its crew and cargo, with the HLS then loaded with the crew and cargo from it to take them to the lunar surface. But while there may be some components of the Lunar Gateway system ready in lunar orbit by then, there are skeptics on whether it will be ready by whenever Artemis III might be launched. In that case, the transfers of crew and cargo would be done directly from the Orion to the HLS. This of course calls into question why it is needed at all. There might be a quite valid scientific justification for such a facility in orbit around the Moon, but so far the rationale given has been its role in the Artemis missions.

SpaceX won the contract for the HLS. Under its proposal, a version of the Orbital Starship would be developed which would operate solely in the space environment to ferry crew and cargo back and forth to the lunar surface. It would never re-enter the Earth’s atmosphere and hence would not need the heat shield. Nor would there be a need for the large wing flaps and tail that on the Orbital Starship are required for aerodynamic control on re-entry to the Earth. And while I have not seen this written in any of the limited plans that have been made publicly available (details on the Artemis plans that have been made public are surprisingly sketchy), it is not at all clear that the Lunar Starship would require all six of the Raptor engines that are on the Orbital Starship.

Three of those Raptor engines are optimized for operation in the vacuum of space (Vacuum Raptors), and three (Sea-Level Raptors) are optimized to operate in the atmosphere near sea-level for the return and soft-landing on Earth. I have not been able to find in any reports whether all six are needed for the initial launch into Earth orbit, but with three designed for operation at sea-level, it is not clear that all six are. Furthermore, the Lunar Starship itself would be lighter than an Orbiter Starship (due to no heat shield nor flaps) so less thrust would be needed. It is therefore not clear whether the three Sea-Level Raptor engines would be needed, and if not this would also save a good deal of weight. And with three Raptor engines sufficient for a landing on Earth, one would assume that three would more than suffice to land in the far lower gravity of the Moon. Indeed, while full details have not been made public, the final phase of the landing of the Lunar Starship on the Moon would not use the Raptor engines at all, but rather a large number (possibly 24) of medium-sized thrusters positioned in the mid-body of the Lunar Starship for the final landing. This is so that the Raptor engines at the bottom do not blow out an excessive amount of debris as they land.

Keep in mind also that once a vehicle is in orbit, the thrust required in order to, say, launch the craft on to a trans-lunar trajectory (TLI) from Earth orbit to the Moon (or vice versa) does not have to be all that strong. The power required comes from the combination of thrust times the duration of the burn, so a set of engines with a lower overall thrust could achieve the velocity required by having the engines stay on for a longer period of time. This is in contrast to a launch from the Earths’s surface, where a high thrust is needed to escape the pull of gravity. Once in orbit, one does not need to rush this. So again, it is not clear that one would need to keep all six Raptor engines on the Lunar Starship. The only issue is whether the initial launch of the Lunar Starship into Earth requires all six Raptors, even though only three are optimized for operation in a vacuum.

The Lunar Starship would be launched into Earth orbit on the Super Heavy booster, as would be standard. Some set of its own Raptor engines would also be fired for this. It would then be refueled in Earth orbit before launching to the Moon. This ability to refuel in orbit is a key ability of the Starship system, and is central to the flexibility that Starship allows in serving multiple objectives. Prior to the launch of the Lunar Starship, a Fuel Depot Starship would have been launched into Earth orbit, where it would have received fuel carried and then transferred to it from multiple Orbital Starship launches. The Fuel Depot Starship would essentially be a set of two large fuel tanks (one for liquid methane and one for liquid oxygen – the fuel plus oxidizer used by Starship) that has been well-insulated given the cryogenic temperatures the fuel and oxidizer need to be kept at. And since the Fuel Depot Starship would be kept in orbit and not land back on Earth, there would be no need for a heat shield nor the wing flaps (nor for all six of the Raptor engines I assume) on it either.

A fully-fueled Starship can hold 1,200 tons of fuel (or technically, fuel plus oxidizer). But each Starship launched from Earth would be able to carry 100 tons of cargo initially, with this expected to grow relatively soon to 150 tons. Assuming the 150-ton capacity, Elon Musk noted that eight Starship flights to the Fuel Depot Starship would provide the 1,200 tons needed to fill the tanks on a Lunar Starship. But how full the tanks would need to be will depend on how much the Lunar Starship would weigh (with no heat shield, wing flaps, nor possibly some of the Raptor engines), and how heavy of a payload would be taken to the lunar surface. Musk concluded that only four flights to deliver fuel might be sufficient.

Much of this is still not clear – at least in what has been made public – and the final answer will depend on how heavy a payload the Orbital Starship will be able to carry to low Earth orbit (100 tons or 150 tons or something in between), how much lighter the Lunar Starship might be than the regular Orbital Starship, and how heavy the payload to the Moon would be. And with differing payloads, the number of refueling flights needed might well differ from mission to mission. None of this has as yet been spelled out, and likely is not yet fully known to anyone given the factors that are still uncertain. But the key point is that the Starship system provides for flexibility where if additional flights are needed to lift the fuel required for refueling of the Lunar Starship in orbit, they can be carried out as needed.

Fully refueled, the Lunar Starship would then be sent to lunar orbit, to either the Lunar Gateway (if it has been built) or just to the similar orbit, to await the Orion capsule carrying the crew who would be launched on an SLS. The Lunar Starship would likely already have most or all of the cargo required, but if there is anything additional carried on the Orion it would be transferred along with the crew. The Lunar Starship would then carry the crew and cargo to the surface of the Moon and serve as a base for the crew during the time they spend on the lunar surface. On the first mission (Artemis III) the current NASA plan, as noted above, is that this would be one week. Also, the contract specifications NASA wrote for the HLS competition was that the initial mission to the Moon would be for two astronauts to land while two would remain in lunar orbit at either the Lunar Gateway (if available) or just in the Orion capsule. After the initial mission, NASA’s plan is that the HLS should be upgradable so as to be able to carry four astronauts to the surface and back. But given the extremely large capacity of the SpaceX Lunar Starship, it is likely that they will build in the capacity to carry a crew of four from the start. And if NASA keeps to its plan to use Orion to carry astronauts to lunar orbit from the Earth, then that will be the ceiling as the Orion can carry no more than four (other than in an emergency).

Once the Lunar Starship carries the crew back to the Orion capsule waiting in lunar orbit, the Orion with the crew would return to the Earth. The Lunar Starship, designed to be fully reusable for this role, would return on its own to Earth orbit where it could then be refueled by multiple regular Starship launches, stocked with any cargo desired, and then sent back to the Moon for the next NASA mission. And the cycle could keep repeating.

3) Comparison of the Three HLS Proposals: SpaceX, Blue Origin, and Dynetics

After an initial request for proposals for the HLS in 2019, NASA provided funding in May 2020 to three teams to develop their proposals further. The three chosen were Space X (with its Lunar Starship); a team that called themselves the “National Team” but which was led by Blue Origin and which is typically referred to as the Blue Origin proposal; and finally a team led by the not too well known aerospace firm Dynetics. The HLS vehicle of Dynetics is named “ALPACA” (an acronym for Autonomous Logistics Platform for All-Moon Cargo Access).

The three proposals differed radically, both in the approaches taken and in their size. Such diversity in approaches is certainly good and healthy, but at the same scale they would look like this:

Source: IEEE Spectrum, January 6, 2021

The mission plan using the Lunar Starship was described above. The plans are quite different for the Blue Origin and Dynetics proposals. A short description of each will be helpful before the three proposals are directly compared.

Blue Origin has worked in partnership with Lockheed Martin, Northrup Grumman, and Draper for its proposed lunar lander. Its design is the most traditional, with a broad similarity to the design of the lunar lander (the LEM) of the Apollo program. That is, there will be three separate components, with a descent stage (to be built by Blue Origin itself, and called the “Descent Element”), an ascent stage (to be built by Lockheed Martin, and called the “Ascent Element”), as well as a “Transfer Element” (to be built by Northrup Grumman) that is basically a rocket engine with fuel tanks that would take the proposed HLS from the high lunar NRHO orbit to a low lunar orbit where it would disconnect and the descent stage would take over. Draper (or Draper Labs) would be responsible for the descent guidance system and flight avionics.

Together they call themselves the “National Team”, with Blue Origin in the lead. They have named their proposed lunar lander the “Integrated Lander Vehicle” (or ILV). The firms in the National Team basically come out of the traditional aerospace industry. While some might consider Blue Origin (owned by Jeff Bezos) as different – as a private, entrepreneurial, company more akin to SpaceX – it really isn’t. Much of the Blue Origin leadership has been drawn from traditional aerospace firms, and it has followed a development process more similar to that of traditional aerospace than that of SpaceX. Its CEO, Bob Smith, came to Blue Origin from Honeywell Aerospace, and had previously held senior positions at the United Space Alliance (a joint venture of Lockheed Martin and Boeing that managed aspects of the Space Shuttle program for NASA) and before that at The Aerospace Corporation.

The three components of the Blue Origin ILV would be flown to the NRHO lunar orbit on three flights of the United Launch Alliance (ULA) Vulcan Centaur rocket that is now under development. The United Launch Alliance is a 50/50 joint venture of Boeing and Lockheed, and the Vulcan Centaur would be a follow-on launcher that would replace ULA’s Atlas V and Delta IV boosters that are now being phased out. The Vulcan Centaur will use rocket engines (named “BE-4”) being developed by Blue Origin, but due to repeated delays in delivering those engines, ULA has had to postpone the first test flight of the vehicle. At one point it was supposed to have flown in 2020. Most recently, the formal plan is for a test flight in 2022, but some have noted that with the continuing delays at Blue Origin, the first test flight might not be until 2023.

Alternatively, instead of flying the three components of the Blue Origin ILV to the NRHO on three of the still-to-fly Vulcan Centaur launch vehicles (with the three components of the ILV then assembled together into one unit there), it could be flown to lunar orbit already assembled on one flight of the still-to-fly SLS. But additional SLS vehicles are not available, and would cost $2 billion each if they were. A single Vulcan Centaur launch is expected to cost perhaps $120 to $150 million.

After receiving the NASA crew and cargo in the NRHO lunar orbit, the Blue Origin ILV would then be taken to a low orbit around the Moon with the Northrup Grumman Transfer Element, after which it would disconnect and the Blue Origin Descent Element would take over for the final descent to the surface. Using the Transfer Element basically saves on the weight of the larger tanks (and associated hardware) that would otherwise be required if all of the trip from the NRHO to the lunar surface were powered by the Descent Element. And as discussed below, it might be possible to reuse the Transfer Element on subsequent missions, although this would require that the fuel it needs be brought to the lunar NRHO orbit in some way.

The habitable space in the ILS would be a pressurized cabin on the Ascent Element, and the crew would live there for the time they spend on the lunar surface (about a week on the initial mission). Cabin space would be tight, and only enough for a crew of two on the initial flights. NASA’s original plans for the return to the Moon was for a crew of four, but reducing this to two for the initial two flights was one of the simplifications NASA introduced (albeit at a greater overall cost in the long run) when the Trump administration instructed NASA to accelerate its plans and get a crew to the Moon by 2024. But the intention is for crews of four after the first two missions, and one of the criteria NASA indicated it would consider in the competition for the HLS contract was whether the proposed lander could be relatively easily scaled up to handle a crew of four. One factor NASA cited when it decided not to accept the Blue Origin proposal for the HLS was that such a scaling-up to accommodate a crew of four would be difficult with its design. A substantially larger cabin in the Ascent Element would be needed, which would weigh more as well as take more space, which would require not only a substantially redesigned Descent Element to handle the extra weight but also more powerful Ascent Element engines to return the crew to the NRHO lunar orbit.

Once the Ascent Element returns the crew to the NRHO orbit, the crew along with any cargo (lunar rocks) being brought back would transfer to the waiting Orion (or first to the Lunar Gateway, if it is there yet), and then return to Earth on the Orion.

What is not fully clear is what will then happen in terms of reusability of (portions of) the Blue Origin HLS. The Descent Element can clearly only be used once, as it would remain on the surface of the Moon. The Ascent Element might in principle be usable again (if designed for this), and possibly also the Transfer Element (if it is designed to hold sufficient fuel to bring it back to the NRHO orbit following its use for bringing the HLS to a low lunar orbit). However, each would then need to be refueled if they were to be used again, and probably two Vulcan Centaur launches would be required to bring those fuels (which are also different for each – liquid hydrogen and liquid oxygen for the Ascent Element and hypergolic fuels that ignite on contact for the Transfer Element). it is not clear whether much, if anything, would be saved by developing the tankers to bring those fuels to the NRHO and then transferring them to the Ascent and Transfer Elements. The tankers would then be thrown away as they could not be returned to Earth, and it is not clear whether much would be saved over just building new copies of the Ascent and Transfer Elements (along with the Descent Element) and then sending them fueled to the NRHO.

Dynetics has given the name ALPACA to its proposed HLS. Dynetics is a medium-sized aerospace firm, based in Huntsville, Alabama, that was acquired by the defense contractor Leidos just a few months before NASA announced in April 2020 that Dynetics would be one of the three HLS proposals it would fund for further development. While Dynetics would work with a number of subcontractors (the two most important being Sierra Nevada Corporation – an aerospace firm – and Draper once again for the avionics), the responsibility for the design is fully with Dynetics.

The Dynetics design is quite radically different from any that have been considered before. As seen in the artist’s rendering above, the Dynetics ALPACA would be basically a crew cabin with rocket engines and their tanks on the two sides. Three launches on a Vulcan Centaur would be required to bring it to the NRHO lunar orbit – one for the empty ALPACA and two for the fuel and oxidizer (liquid methane and liquid oxygen). The fuels would then need to be transferred to the ALPACA in the NRHO lunar orbit, and NASA cited this as a concern when it reviewed the Dynetics proposal. The technology still has to be developed. While there would also be in-space transfers of the cryogenic fuel and oxidizer in the SpaceX Starship proposal – and in far greater volumes – this would be done in Earth orbit for the Starship instead of lunar orbit for the Dynetics ALPACA. If a problem arose, it could be more easily addressed if still in Earth orbit. Furthermore, development of this refueling ability is central to the Starship system, and hence SpaceX is devoting a good deal of attention to ensure it will be able to do this. Dynetics and its partners would not require this ability for anything other than their ALPACA.

Once fueled and ready, the Orion would be launched on the SLS, rendevous with the ALPACA in the NRHO lunar orbit for the transfer of the crew and cargo, and the ALPACA would then take the crew to the surface. NASA found an important issue during its review of the Dynetics proposal, however. Given the weight of ALPACA, the thrust of its engines, and the fuel that would be carried, NASA concluded that there would be insufficient fuel to keep ALPACA from crashing into the lunar surface, even with no crew or cargo at all. That is, its payload capacity would be negative. Dynetics conceded that this was indeed an issue with its current design, but was confident that they would be able to lighten ALPACA sufficiently so that it would be able to carry the crew and cargo and not crash. NASA, however, was skeptical. Such spacecraft normally increase in weight as they are further developed, as issues are found requiring modifications to resolve those issues. It is rare that there would be a reduction in their weight. And NASA’s bid specification was that the HLS had to be able to bring to the lunar surface a minimum of 865 kg (of crew and cargo, including the space suits needed to venture outside), with a preferred goal of 965 kg.

Assuming it could land, the ALPACA proposal had the significant positive in its design in that the crew cabin would be very close to the ground. In the Lunar Starship proposal, the habitable crew cabin would be far above the ground, and an elevator arrangement would be used to carry the crew back and forth from the surface. In the Blue Origin ILV, the crew cabin would also be far above the ground (although not as high up as on the Lunar Starship), but the crew would need to climb down and up a 12 meter (39 foot) ladder in their lunar spacesuits to reach the surface. That would be cumbersome and probably tiring despite the low lunar gravity (as the lunar spacesuits would be heavy and bulky), and possibly catastrophic should anyone slip and fall.

At the end of the stay, the Dynetics ALPACA would then fly the crew back to the NRHO orbit to link up with the Orion (or Lunar Gateway if it is there), where the crew and any returning cargo would be transferred for the return to Earth on the Orion. The ALPACA could then wait there, and if to be used on a subsequent mission, could be refueled with two launches of a Vulcan Centaur carrying fuel to it as would have been done on the initial mission.

The designs and mission plans are therefore radically different in the three proposals. The proposed costs, as well as the payload and other capacities of the resulting bids, also differed dramatically, as summarized here:

|

Lunar Starship |

Integrated Landing Vehicle (ILV) |

ALPACA |

|

|

Lead Firm |

SpaceX |

Blue Origin |

Dynetics |

|

Other Primary Firms |

none |

Lockheed Martin Northrup Grumman Draper |

Sierra_Nevada Draper |

|

Max Payload to Lunar Surface |

100 tons |

850 kg |

negative |

|

Habitable Volume |

1,000 m3 |

12.4 m3 |

14.5 m3 |

|

Floor Area |

325 m2 |

4.7 m2 |

5 m2 |

|

Max Crew Size |

Many (well more than 4 if desired) |

2 at first; redesign for 4 |

2 at first; later 4 |

|

NASA Development Award, April 2020 |

$139.6 m |

$479.7 m |

$239.7 m |

|

Final Bid Price, April 2021 |

$2.94 b |

$6.00 b |

$9.08 b |

Depending on the number of refueling flights of Starship to Earth orbit, the Lunar Starship could conceivably carry as much as 100 metric tons of cargo to the lunar surface. This dwarfs the estimated 850 kg that the Blue Origin ILV could bring (which is close to, but slightly below, the minimum NASA specification that it should be able to bring 865 kg to the surface). And as noted above, NASA does not believe the Dynetics ALPACA would be able to carry even itself to the surface without crashing into it.

The habitable volume of the Lunar Starship would also be enormous, at 1,000 cubic meters. This is larger than the entire habitable volume of the International Space Station (which is 916 cubic meters), and the ISS had to be slowly assembled in space over a period of 13 years. In sharp contrast, the habitable volume of the Blue Origin ILV would be just 12.4 cubic meters, which it says would be enough for a crew of two, but acknowledges would not be enough for a crew of four. Hence the need for an extensive redesign of the Blue Origin ILV if it were to be used for subsequent Artemis missions when they would need to accommodate a crew of four. And the Dynetics ALPACA would have a volume of 14.5 cubic meters – only a bit more than on the Blue Origin ILV – which it argues would be sufficient for a crew of four. Keep in mind that the habitable space for the crew is not simply for their landing on the lunar surface, but for their stay there of about one week on the first Artemis mission with this increasing to a planned 30 days on the following Artemis mission and even more later. Such accommodations would be tight, especially for a crew of four.

Resting on the lunar surface, where there is gravity and not simply the weightlessness of a vehicle in orbit, the floor area will also matter. For the Lunar Starship, the floor area (on several different floor levels) would come to 325 square meters (3,500 square feet). That would be the floor area of a very substantial house in the US. In contrast, the floor area on the Blue Origin ILV would be just 4.7 square meters, and only slightly more at 5 square meters on the Dynetics ALPACA. Five square meters for a crew of two for a week is not much, and especially not for a crew of four for a month or more on the lunar surface.

NASA announced in April 2020 it would provide funding to the three competitors for them to develop more concretely their proposals. But the dollar amounts provided were not equal. NASA was relatively quite generous with providing almost $480 million to the Blue Origin team, but just half this (almost $240 million) to Dynetics for its ALPACA proposal. And to SpaceX the grant was just below $140 million. One cannot argue that NASA was unfairly favoring SpaceX in its grants for the further development of the proposals.

Finally, the price SpaceX bid for the contract – at $2.94 billion – was less than half the $6.00 billion price Blue Origin offered, and less than one-third the price of $9.08 billion Dynetics said it would need. The price includes the development of the vehicle, a test flight where it would go through the full mission sequence (including landing on and then returning from the lunar surface) but without a crew, and then the Artemis III mission itself with a crew of two.

Based on all this, it should not be difficult to see why NASA chose the SpaceX proposal. Basic feasibility is of course key, and NASA certainly paid close attention to this. It found, for example, that by its calculations, the Dynetics ALPACA would not be able to land on the Moon with any payload at all.

But after its detailed review of the SpaceX plans during the year it was funding the more concrete development of those plans, and with full access to all the SpaceX technical teams and the work they had done, NASA engineers concluded the SpaceX proposal was feasible. As noted before, this in itself was a tremendous vote of confidence in the still-to-fly Starship. And NASA also concluded that SpaceX would be able to deliver on these plans quite soon. While I personally have strong doubts that this will be possible by 2024 (or even 2025), this time frame is of interest as it implies that NASA engineers believe the basic Starship system will be flying successfully very soon, i.e. by sometime in 2022. It implies that they have concluded that the current Starship design is basically doable, and that a major redesign will not be necessary for it to be successful.

Despite the clear superiority of the SpaceX proposal over those of Blue Origin and Dynetics, the latter companies did not see it that way. Soon after NASA’s decision was announced in April 2021, both Blue Origin and Dynetics appealed to the US Government Accountability Office (GAO), arguing that NASA had not properly followed government procurement procedures. Such appeals are not uncommon, and sometimes lead to reversals. But the GAO concluded, in a report issued on July 30, that NASA had followed the proper procedures and was justified in making the award to SpaceX.

While Dynetics accepted this and moved on, Blue Origin decided then to file a court case protesting NASA’s decision. This was frustrating to many, as NASA could not grant the award to SpaceX nor work with SpaceX on the contract while an appeal was underway. Both sides (NASA and Blue Origin) agreed, however, to expedited court procedures where the judge would make a decision (without a jury) and would do so by early November. The judge’s decision was then announced on November 4, rejecting Blue Origin’s claims. The full decision was released on November 18, after Blue Origin had been given the chance to make redactions of commercially confidential information in that judicial opinion.

4) The Possibilities with Lunar Starship

The mission profiles discussed above follow what NASA has set out for its Artemis plans to return to the Moon. That is, NASA set how the HLS chosen would be used, and the missions are based on use of an Orion to take the astronauts to the high NRHO lunar orbit and an SLS to launch them there (along with, possibly, use of the Lunar Gateway in the NRHO orbit to serve as a staging area). The Lunar Starship would then take the crew from the lunar orbit to the surface of the Moon and back. The Starship would have been launched into Earth orbit, refueled there, then flown to the NRHO orbit, and following the delivery of the crew back at the NRHO would be flown back to Earth orbit for refueling after which it could be used again for the next lunar mission.

But if a Lunar Starship can do all this, there is the obvious question of why one needs the Orion, the SLS, and the Lunar Gateway, at all. The Lunar Starship will have all the life support systems, seats, and other equipment required to carry the astronauts to a lunar landing and then to support them there for extended periods (one week on the first mission, a month on the second, and more later). It will also have lots of space and an ability to carry a cargo load far in excess (more than 100 times as large) of what NASA set in its minimum requirements. Forcing the four astronauts to squeeze into the Orion capsule (with a habitable volume of just 9 cubic meters) for the multi-day flight to lunar orbit, while the Lunar Starship (with a habitable volume of 1,000 cubic meters) would fly there empty, seems absurd. It would be similar to forcing a group of four to squeeze into a Volkswagon Beetle for a drive across the US, while a luxury bus drove the same route, but empty, only to be used for a final short segment at the end of the journey.

I fully acknowledge that there will be technical issues to work through. Fuel loads would have to be calculated and would need to suffice. But the flexibility in the Starship system, where additional in-orbit refuelings could be provided if there is a need, combined with a scaling back, if need be, of the payload to be lifted (a 100-ton capacity means there is a lot of room for adjustment), means that if a Lunar Starship in the NASA HLS role is feasible, then it should certainly be for this expanded role as well.

The mission plan would then be that once there is a fully fueled Lunar Starship in Earth orbit (with whatever number of refueling flights to the Fuel Depot Starship that might require, with the Lunar Starship then fueled from what has been stored in the Fuel Depot Starship), the NASA crew of four (or even a substantially higher number, as there would be plenty of room) would be flown to transfer to the vehicle while it is still in Earth orbit. They could be flown there on a regular Orbital Starship flight or even on one or more flights of a Falcon 9 with the now well-tested Crew Dragon capsule. They would then be flown on the Lunar Starship directly to the lunar surface, or possibly first to a lunar orbit and then to the surface.

Furthermore, given its vast size the Lunar Starship could in effect be an instant base on the Moon. There would be no need to bring to the Moon via a series of separate flights all the components that would otherwise be needed to build such a base. NASA’s long-term Artemis plans had envisaged this following the first two Artemis landing missions (at least in the plans set before Lunar Starship was chosen). A permanent, habitable, structure (“Artemis Base Camp”) would have been built on the lunar surface to house the crews, with this slowly expanded in size as additions are brought on subsequent missions. With the available space in the Lunar Starship, there would be no need. And the Lunar Starship would also have the space needed, as well as the cargo capacity, for the lunar rovers that NASA has planned.

The Lunar Starship as a lunar base would also have the rather unique capability of being packed up, lifting off, and then flown to a new location, if there is any desire to do this. There might be value in exploring various sites around the Moon – in a search for frozen waters supplies, for example. One would just have to ensure that adequate reserves of fuel were brought along. And if, as some believe likely, significant amounts of frozen carbon dioxide along with frozen water are found on the Moon (most likely near the South Pole, which is why this has been chosen for the early missions and the planned Artemis Base Camp), then it would be possible to produce the liquid methane fuel the Starship uses along with the liquid oxygen, and refuel the Lunar Starship while it is there.

If there is a need for additional cargo, one could also design a version of the Lunar Starship to carry cargo only. It would fly there on its own (which is now a standard technology – indeed under the NASA HLS contract the Lunar Starship would be required to complete an entire unmanned flight as it would under Artemix III, including landing on the Moon, as a test of the entire system before any crew is put aboard). If it was not then to be returned to the Earth and thus not need the fuel to do so, but rather remain on the surface as a permanent addition to a growing lunar base, such a cargo flight could bring a load of as much as 200 tons. This is huge. The weight (mass really) of the entire International Space Station is, after all the additions over the years, now 420 tons.

And the possibilities the Starship system would open up are not just limited to the Moon. Very recently, a group of prominent planetary scientists issued a White Paper arguing that with the availability of Starship, the traditional approach taken to planetary exploration missions should be radically re-thought. With the capacity of the Starship, along with its low cost, planetary missions could become not simply far more frequent but also simplified in design. Rather than spend a good deal of money and a good deal of time in refining the spacecraft to reduce its weight by a few ounces or its dimensions to fit into the limited capacity of the existing rockets that are used, one could simply use off-the-shelf equipment when Starship is used to send it on its way. Finally, there is of course the missions to Mars for which the Starship system has been designed. But all this goes beyond what I intended to cover in this already long post.

Finally, flying the lunar missions on Starship rather than with the Orion, SLS, and associated systems would be far cheaper. As an extremely rough calculation: Assume that each Starship launch will cost $20 million (ten times the $2 million Elon Musk has said it will ultimately cost) and that 10 Starship launches would be required for each mission (for refueling in orbit – note that the Lunar Starship and the Fuel Depot Starship would remain in space following their initial launch and would be reused), for a total cost of $200 million for the launches. For simplicity, assume all the other costs of the launches and then for carrying out the mission would be similar and hence the total cost would be $400 million to carry out the mission. While crude, this estimate almost certainly errs on the high side. The actual cost is likely to be lower, but take $400 million for the purposes here.

In contrast, the Office of the Inspector General (OIG) of NASA in a recent (November 15, 2021) report assessing NASA’s Management of the Artemis Missions estimated that the cost of a single SLS launch with an Orion capsule for an Artemis mission would come to $4.1 billion. The SLS itself (none of which is reusable – all is thrown away in each launch) would cost $2.2 billion. This is similar to, but 10% more than, the estimated $2.0 billion cost per launch for the SLS made by the White House Office of Management and Budget (OMB) and released in a letter to Congress in 2019.

The NASA OIG estimated that the cost of an Orion crew vehicle, including the cost of the Service Module being built by the European Space Agency, would total $1.3 billion, of which $300 million would be for the Service Module. In my earlier blog post, I used the contracted amount NASA would pay for the third through the fifth Orion vehicles ($900 million each), but the earlier ones would be higher and the $1.0 billion estimate of the OIG is consistent. Interestingly, I had thought in my earlier blog post that the European Space Agency would be covering the cost of the $300 million Service Module they are making for the Orion, but the OIG report clarifies that this will not really be the case. While the Europeans will be paying the contractor that will build the module, NASA will then not charge the Europeans $300 million (per Orion) for costs incurred on behalf of the Europeans at the International Space Station. That is, this is a barter agreement, so NASA is in fact paying that $300 million cost, but indirectly. By including it in the ISS budget, where it is not broken out in what is made publicly available, one cannot determine the true cost of the complete Orion vehicle without access to unpublished information.

Finally, the NASA OIG also includes in the cost of an SLS launch the pro-rated share of what it costs to maintain the ground facilities (the launch pad, etc.) needed for an SLS launch. Since there will be only (at most) one SLS launch per year, this will be the annual budget for maintaining and then using (once) that capacity, which the NASA OIG estimates to be $568 million per launch.

The NASA OIG therefore estimates the total cost per launch of the SLS with Orion will be $4.1 billion. This would be ten times the generously estimated cost of doing the same via Starship, and for far less capacity.

D. Politics

Why then keep funding the SLS and Orion? In the near term, it might make sense. After all, despite all that has already been done to test and develop Starship, the testing is not yet complete and orbital testing is still to start. And while NASA technical staff concluded it should ultimately work, it might not. The key tests will be in the next year, however, and we should know by the end of 2022 (or before) whether Starship will work as planned. There will certainly be failures at first in the upcoming orbital tests. As discussed above, this is to be expected in the iterative development process used by SpaceX. But with iterative improvements, with solutions found to the problems uncovered, it will eventually work. We will only know that for sure, however, when it does.

Whether Starship will work should be known, however, by no later than the end of 2022. Provided Starship has demonstrated that it will indeed work, should one then expect to see NASA (with Congress) decide to close down the SLS and Orion funding and switch over to the far more capable and far less costly Starship system? The answer to that is: not likely.

First of all, it will be politically embarrassing to admit that it was a mistake. By the end of FY23, over $54 billion will have been spent ($32 billion for the SLS and $22 billion for the Orion). The fundamental error came when Congress in 2010 forced the Obama administration to start development immediately of a heavy-lift launcher that became the SLS. The Obama administration had recommended that NASA should first examine and test certain new technologies (in particular in-orbit refueling ability), with the results then used to determine how best then to design such a launcher. Congress, and in particular the Senate, insisted (and wrote into law in the 2010 NASA authorizing legislation) that the heavy-lift launcher be designed immediately and furthermore that it make use of the key components of the Space Shuttle (e.g. the engines) in that design. By mandating this, those in their states and districts who had been employed building such components for the Space Shuttle would remain employed. But with such requirements written into law, some wags have concluded the SLS should not stand for Space Launch System but rather Senate Launch System.

Republican Senator Shelby of Alabama (home of the NASA Marshall Space Flight Center in Huntsville – the center with the primary responsibility for the SLS) was a key advocate, as was Republican Senator Kay Bailey Hutchison of Texas (home of the NASA Johnson Space Center in Houston – responsible for manned space flight operations). Senators from Mississippi (home of the Stennis Space Center, where large rocket engines are tested), Louisiana (home of the Michoud Assembly Facility), and Utah (home of the company that builds the solid rocket boosters that are strapped on to the first stage) were also important advocates. As was one Democratic Senator – Bill Nelson of Florida (home of the Kennedy Space Center), who was the chair of the subcommittee that drafted the NASA Authorization Act of 2010 when Democrats controlled the Senate.

Former Senator Bill Nelson is now NASA Administrator. Canceling SLS and Orion would be an embarrassment for him, even if Starship demonstrates its full ability to carry out the nation’s lunar exploration plans – and do so far more effectively and at far lower cost. As NASA Administrator he has already signaled that NASA intends to continue to use the SLS, and for possibly 30 years or more. In October, NASA issued a “Request for Information” to the aerospace industry, requesting proposals from firms willing to produce, operate, and maintain the SLS rocket system until the 2050s, with the stated intention that this should reduce the “baseline per flight cost” of an SLS launch by “50% or more”. The NASA Request for Information did not say, however, what the current baseline cost was from which the 50% would be taken, and refused to respond to reporter queries on what NASA estimates that cost to be. But as noted above, the White House Office of Management and Budget indicated in a letter to Congress in 2019 that the cost was $2.0 billion per launch. A more recent estimate from the NASA OIG puts that cost at $2.2 billion.

But NASA itself has consistently refused to reveal what the per launch costs of the SLS will be. This is despite repeated recommendations over the years by oversight bodies that it should. For example, the Government Accountability Office (GAO), which is formally part of the legislative branch reporting to Congress, recommended NASA provide such an accounting in a 2017 report, when it was already clear that the SLS would be delayed and well over the original planned cost. More recently, the NASA OIG report of November 15, assessing the management of the Artemis program, recommended that NASA management provide such figures. But NASA management has continued to refuse. The NASA OIG report made nine recommendations, and NASA management accepted seven (two partially). But it rejected the two recommendations on the issue of being transparent on costs.

Congress has, however, not forced NASA to reveal those costs. While the overall budget of NASA is known year by year, as well as the budgets of major sub-aggregates of certain individual programs as NASA has organized them, one cannot work out from this the overall cost of a major program such as Artemis (with responsibilities for portions of the program spread across much of the agency) nor work out a separation between the cost of developing a new vehicle or system such as the SLS and the cost then of using that system on individual missions. There is a lack of transparency, although entities such as the GAO or the NASA OIG (as well as journalists and other outsiders) may try to come up with estimates.

Senators and Members of Congress may be quite comfortable, however, with this lack of transparency. It then does not draw attention to the overall costs (and how high those costs might have grown to) even though they still wish to see (and to publicize) how much is being spent in their particular districts. And NASA is glad to provide this. For examples, see here, here, here, here, here, and here. Spending more is seen not as a flaw but as a feature.

The SpaceX Starship, if it works, may have a cost of just $2 million per launch. Even if the cost turns out to be ten times that, it will still be dramatically less costly than an SLS alone, and even more so of an SLS plus Orion system. Furthermore, and importantly, it would be far more capable. It would enable far more to be achieved in meeting the stated national objectives of the space exploration program than would be possible with the SLS plus Orion system. It would be quite revolutionary. But it will only be used for this purpose if the American political system allows it.

You must be logged in to post a comment.