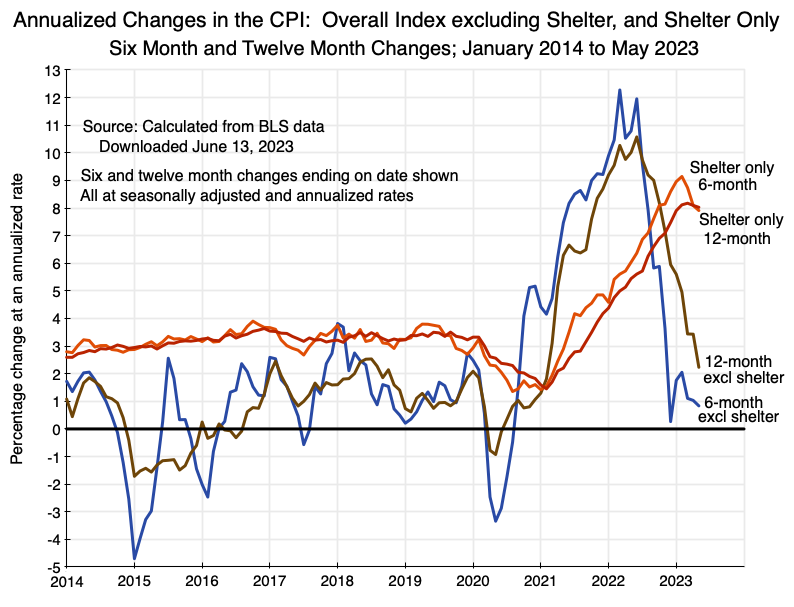

This is just a short update to my May 10 post on this blog to reflect newly released data. The Bureau of Labor Statistics released today its estimates for the Consumer Price Index for May 2023. I noted in the May 10 blog post (that had data through April 2023) that the pace of inflation when one excludes the shelter component had come down sharply over the past year. One sees this most clearly when one focuses on the change over rolling 6-month periods (annualized). The rolling 6-month change in the CPI excluding the shelter component peaked in early 2022 at an annualized rate of over 12%. But since late 2022, the 6-month rate has fluctuated in the range of just 0.3 to 2.0% (annualized), and it remains there. The May 2023 6-month figure was just 0.8%. The Fed’s target is to keep inflation at around 2%. These have been below that for half a year now.

This is just a short update to my May 10 post on this blog to reflect newly released data. The Bureau of Labor Statistics released today its estimates for the Consumer Price Index for May 2023. I noted in the May 10 blog post (that had data through April 2023) that the pace of inflation when one excludes the shelter component had come down sharply over the past year. One sees this most clearly when one focuses on the change over rolling 6-month periods (annualized). The rolling 6-month change in the CPI excluding the shelter component peaked in early 2022 at an annualized rate of over 12%. But since late 2022, the 6-month rate has fluctuated in the range of just 0.3 to 2.0% (annualized), and it remains there. The May 2023 6-month figure was just 0.8%. The Fed’s target is to keep inflation at around 2%. These have been below that for half a year now.

The most interesting new data point in the chart above is the most recent 12-month change in the CPI excluding the shelter component. It had hit a peak of over 10 1/2% in mid-2022, but had come down to a rate of 3.4% in March as well as in April. In the newly released data as of May, it had fallen further to just 2.2% on a 12-month basis. This is basically at the Fed target for inflation.

But the shelter component of the CPI of course matters. It has a 35% weight in the overall CPI index as it includes not only what people pay when they rent housing but also the rental equivalent cost of owner-occupied housing (which can only be estimated by observing what is being paid for rental units). As was explained in the May 10 post on this blog, the shelter component of the CPI can furthermore only be estimated by observations of what people are actually paying as they rent, and rental contracts in the US are normally set for a year. Thus even where there may be pressures to increase rental rates in some market, leading to higher rental rates being charged as contracts come up for renewal, those higher rents will only go into effect when rental contracts are in fact renewed. If you had renewed your rental contract recently, it might be close to a year before the rent you have to pay actually goes up. Since the Bureau of Labor Statistics interviewers ask the households what they are actually paying in rent at the time of the interview, inflationary pressures on rental rates will take up to a year to work their way through.

This long lag is seen in the orange and red lines in the chart above. The annualized rates rose throughout 2021 and 2022. But the 6-month rate peaked in early 2023, reaching a rate of 9.1% (annualized) as of February. As of May it has come down to 7.9%. The 12-month rate peaked at 8.2% in March and is now down slightly to 8.0%. While the news media and others normally focus on the 12-month rates, turning points will often be first revealed by examining shorter time periods. If too short (such as monthly), it may be difficult to isolate the trends from the statistical noise inherent in the monthly data. A 6-month rate is a reasonable compromise.

The cost of housing is still rising at too high a rate. But given the 12-month periods of most rental contracts, and the use of such observed rental rates to impute the rental-equivalent costs of owner-occupied housing, it will take some time for the shelter component of the CPI to return to the rates observed prior to the onset of the Covid crisis. The inflation rates are now coming down, but that cycle is not yet complete.

But excluding shelter, consumer inflation is already back to where it was before the disruptions due to the Covid crisis, with its lockdowns, supply-chain disruptions, and the massive fiscal relief packages passed into law under both Trump and Biden. Hopefully the Fed is paying attention to this.

You must be logged in to post a comment.