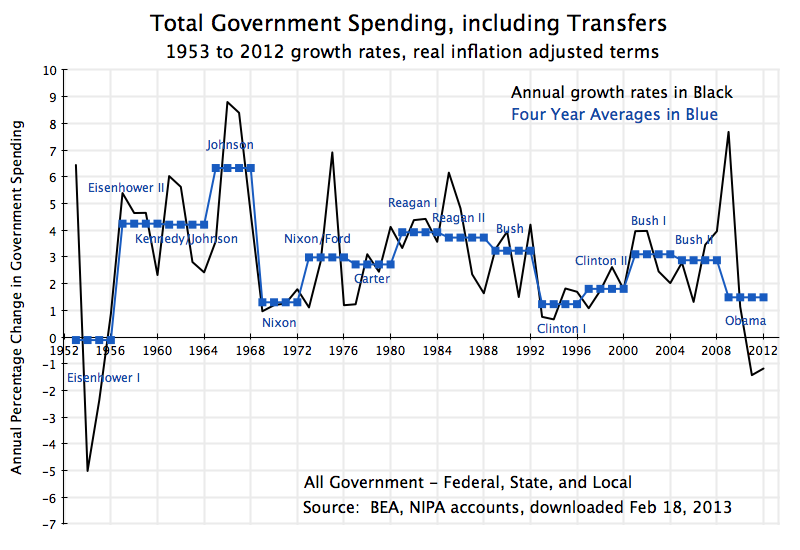

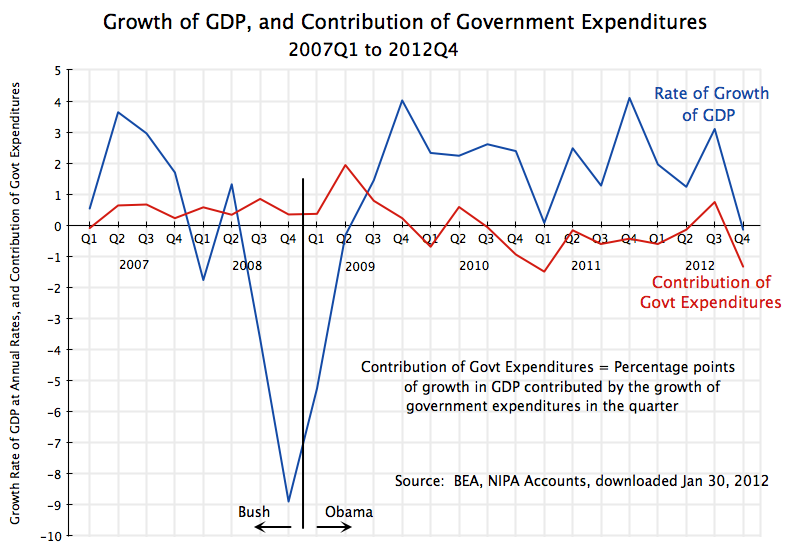

It appears increasingly likely that the Congressionally mandated severe and across-the-board budget cuts, known as the sequester, will begin on March 1. Serious negotiations are not underway, Congress is only back in session now after having been gone for most of the past two weeks, and public statements are not focused on negotiating an agreement but rather on shifting blame. Should the sequestration budget cuts go into effect, not only will critical federal functions be suspended, but the sudden cuts in spending levels will likely push the country back into recession. As was noted in an earlier posting on this blog, cuts in Government spending were already the primary cause for a fall in GDP in the fourth quarter of 2012 (according to the initial estimate, which may be revised). More broadly, had government spending been allowed to rise following the 2008 downturn as it had during the Reagan presidency following the 1981 downturn, we would now likely be at full employment.

The situation is serious, but the new assertion by the Republican leadership that the sequester is there only at the insistence of Obama is almost farcical. As part of this campaign, Speaker Boehner has staged events for the cameras such as that pictured above, behind a podium labeled with the hashtag “#Obamaquester”, and in front of a clock marked as “Countdown to #Obamaquester”. Boehner is now asserting that the sequester is only there due to “the president’s demand”, and he refers to the cuts as “the president’s sequester”.

Even some of Boehner’s Republican colleagues find it absurd to try to blame Obama for the sequester. For example, Representative Justin Amash, a conservative Republican from Michigan (who voted against the bill that set up the sequester mechanism) said: “I think it’s a mistake on the part of Republicans to try to pin the sequester on Obama. It’s totally disingenuous. The debt ceiling deal in 2011 was agreed to by Republicans and Democrats, and regardless of who came up with the sequester, they all voted for it. So, you can’t vote for something and, with a straight face, go blame the other guy for its existence in law.”

With these new assertions from Boehner and similar assertions from colleagues such as Congressman Paul Ryan (the Republican Chair of the Budget Committee in the House), it may be of interest to review briefly the history of how the sequester mechanism came to be:

- The sequester’s origin came from the strategic decision by the key Republicans in Congress in early 2011 to use the routinely required authorization to raise the public debt ceiling as leverage to force through drastic cuts in the budget. Eric Cantor, the then new Republican House Majority Leader, was the principal architect and proponent of the strategy, which he proposed in January 2011 at a closed-door retreat of Republican congressional members in Baltimore. He was soon stating publicly that the Republican controlled Congress should not approve an increase in the debt ceiling without drastic spending cuts.

- What this meant was that they would hold the economy hostage to their budget demands, as a refusal to raise the debt ceiling would force the US to default on its debt. While speeches and pontificating are routine whenever Congress has had to approve an increase in the nominal public debt ceiling, never before had such demands been attached to this approval.

- And default on the US public debt would be serious. US Treasury Bonds are held as risk-free assets both in the US and around the world, and are indeed the foundation of the modern international monetary system. The impact of default on such assets cannot be predicted with certainty, as it has never happened before, but the consequences could quite possibly throw the global economy into a downturn that would make the 2008 collapse look mild.

- [As an aside: While I am not a lawyer, the constitutionality of a refusal by Congress to raise the debt ceiling (and hence force a default on the public debt) looks to me to be questionable. The Fourteenth Amendment to the Constitution (passed in 1866, following the American Civil War) reads in its Section 4: “The validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned.” In their oath of office, Congressmen pledge to uphold the Constitution. They cannot then take actions (or defer taking action) which would violate the Constitution by forcing a direct default on the public debt. However, as noted above, I am not a lawyer, and obtaining such Congressional approval for increases in the debt ceiling has been customary since substantial borrowing needs developed during World War I.]

- As the country was coming increasingly close to breaching the existing debt ceiling in July 2011, negotiations were underway at many levels in Washington. I will not try to review them all here, but the most senior were direct negotiations between Obama and Speaker Boehner. These talks broke up when Boehner was not able to convince his Republican congressional colleagues to support an approach that included even a relatively small share of revenue increases along with larger expenditure cuts. In fact, Boehner had to reverse himself twice from tentative agreements he had reached with the President, as he could not get backing from sufficient numbers of his Republican colleagues in Congress. At the time, Boehner stated publicly that the President had negotiated in good faith. But in his op-ed piece in the Wall Street Journal this month, Boehner now says the opposite, and asserts the talks failed because the President had reversed his position.

- As the deadlines approached and it became clear that agreement would not be possible on a specific set of spending cuts and revenue increases, Jack Lew, then the head of the Office of Management and Budget in the White House (and soon likely to be US Treasury Secretary), suggested consideration of a mechanism that had been used in the 1980s, in budgetary negotiations during the Reagan term. In its final form and as passed by Congress, the mechanism established a Joint Committee made up of 12 members of the Senate and Congress (split evenly between Republicans and Democrats), who would by a certain date (November 21, 2011) develop a plan to achieve $1.2 trillion in deficit reduction (over 9 years) through a combination of spending cuts and revenue increases. If the Joint Committee could not reach agreement, an automatic cut in spending of $109 billion per year over nine fiscal years (FY2013-21) would be required, split evenly between Defense and non-Defense programs. These automatic across-the-board cuts were known as the “sequester”, and were deliberately crude and draconian to serve as an inducement to the Joint Committee to reach an agreement on more palatable means to achieve a similar reduction in the deficit.

- The mandate of the Joint Committee was to reach agreement on measures that would reduce the deficit by $1.2 trillion over ten years. Such measures could include both spending reductions and revenue increases. And the revenue increases could be achieved not only by raising tax rates, but also by closing tax loopholes, cutting expenditures that are implemented via tax subsidies, and/or broadening the tax base. But the Joint Committee never reached an agreement, as Republicans refused to agree to any revenue measures at all.

- At the time, Boehner, Paul Ryan, and other Republicans praised the sequester mechanism as a means to force what they were seeking. Boehner famously said in a CBS interview on August 1, 2011, that he had gotten “98%” of what he wanted. Ryan emphasized and praised the sequester mechanism in an interview on Fox News on August 1. Following his recent reversal now to criticize the sequester, a YouTube video was even put together showing a series of Ryan statements over the years in favor of sequester mechanisms (including this one specifically) and statutory spending caps. And a Power Point presentation put together by Boehner when he made the case to his Republican colleagues to vote in favor of the bill that established the sequestration mechanism, makes clear his approval of it at the time.

- Obama, in sharp contrast, had always wanted a clean bill authorizing an increase in the public debt ceiling, without additional conditions added on. It is indeed rather absurd to think that Obama would want to see a bill passed that would deliberately tie his hands. Obama had proposed alternative approaches to reducing the deficit, including in his FY2013 budget (in great detail) and during the negotiations with Boehner. Obama still stands by these proposals. But while the Republicans assert that Obama has not offered any such plans, the issue is rather that the Republicans have rejected the plans Obama has offered.

- Jack Lew only suggested the option of the sequester mechanism as a fallback if no agreement is reached, late in the negotiations when it became clear that agreement on a specific set of spending cuts and revenue increases would not be possible. But Obama and Lew would have greatly preferred a clean bill without any such conditions. It is absurd to say, as Boehner now does, that the sequester mechanism is there only because it was something Obama “insisted upon in August 2011”.

The automatic sequester will cut government expenditures by $85.3 billion over the remainder of the fiscal year, from March 1 to September 30, 2013. If nothing is done, there would be further cuts of $109.3 billion in each of the next eight fiscal years to FY2021. The $85.3 billion cut over seven months would be equal to roughly 1% of the seven month GDP. With a multiplier of two, this would by itself drive down GDP by 2% from what it would be otherwise. The Congressional Budget Office estimates that the US economy is producing at about 5 1/2% below what it potentially could be producing at full employment. An additional 2% reduction would be significant.

Agreement is difficult in Washington, particularly in the current political environment. But if Boehner, Ryan, and others now hold to the view that the sequester is a bad idea, there is a simple solution. All that they would need to do would be to pass a simple bill which revokes it. Obama would certainly sign it. The budgetary mechanism would then revert to the standard process, and that standard process could be followed to determine whether certain public expenditures should be cut and by how much, and whether revenues should be increased by closing loopholes, cutting tax subsidies, raising rates, or some other approach.

But there is nothing that requires the sequester mechanism. If Boehner, Ryan, and the others do not want it, they can pass a simple bill to end it.

You must be logged in to post a comment.