A. Introduction

A. Introduction

The US economy has just gone through an extraordinary period. The impacts are still being felt – and probably will be for several more years, including into the presidential election year of 2024. A key issue will be whether personal consumption expenditures will continue to grow – at least at some modest pace – as such expenditures are important not only in themselves, but also as they account for more than two-thirds of the demand side of GDP. And this consumption will depend, in turn, on what happens to household incomes and on the decisions households make on their savings.

Very briefly, we will find:

a) Personal Income before taxes and transfers (at the national level as measured in the GDP accounts, and where taxes and transfers are for all levels of government including state and local in addition to federal) fell during the Covid crisis but then recovered to where it was before by mid-2021. Since then, however, it has been relatively flat in real terms.

b) Personal Income after taxes and transfers (called Disposable Personal Income in the GDP accounts) rose during the Covid crisis due to the massive Covid relief packages, but returned to its previous trend path by mid-2021. But as the Covid relief programs wound down, Disposable Personal Income (in real terms) fell, and by October 2022 was almost 7% below its previous trend path.

This stagnation in Personal Income, and fall in Disposable Personal Income, may well explain the common view of many that the economy is not well, despite unemployment rates that have matched the lowest levels of more than the last half-century.

c) But while Disposable Personal Income fell below its trend path, Personal Consumption Expenditure (which had fallen during the Covid crisis) returned fully to its previous trend path by the Spring of 2021. It has since followed that trend path almost exactly.

d) This return of Personal Consumption to its previous trend path, while Disposable Personal Income fell well below its previous trend path, was only possible as households could draw on large savings balances that they had built up during the Covid crisis period.

e) Those savings balances are finite, however, and are being drawn down. While only a crude estimate is possible, calculations based on the savings rates that prevailed before the Covid crisis and then extrapolation based on the pace of the drawdown in 2022, suggest that the excess savings balances will be depleted sometime in 2024.

This may have significant implications, both economically and politically. The Fed is currently raising interest rates aggressively in order to reduce investment spending and hence aggregate demand, with the objective of reducing inflation. Federal fiscal spending has also been falling, with a reduction expected in FY2023 of a further about 1% of GDP. Many analysts (including myself) have felt that a reduction in consumer expenditures in 2023 (as the excess savings balances built up during the Covid crisis run out) should be expected on top of this. But based on the calculations discussed below, those balances might last into 2024. That makes 2024 a complicated year economically, and 2024 is a presidential election year.

The possible macro consequences will be discussed in the concluding section of this post. They are necessarily more speculative. But first we will look at what happened to the savings rate during and following the Covid crisis (the chart at the top of this post), and then what happened to Personal Incomes, Disposable Personal Incomes, and Personal Consumption Expenditures – both in terms of their levels and relative to their previous trend paths. The penultimate section will then provide an estimate of how much excess savings was built up during the Covid crisis period, the pace at which it is now being drawn down, and how long such balances might last before being used up.

A note on usage: When terms such as personal incomes or personal consumption expenditures are capitalized, they are referring to the specific concepts as measured in the published GDP accounts (or more properly, the National Income and Product Accounts, or NIPA). Terms that are not capitalized refer to the concepts more generally. And I made one modification: “Personal Current Transfer Receipts” is defined in the NIPA accounts as net of social insurance (Social Security and Medicare) taxes paid. I instead include such taxes in the category of Personal Current Taxes (i.e. together with individual income taxes), and Personal Transfers are then just the gross transfers (from Social Security, etc.).

B. The Personal Savings Rate

The personal savings rate jumped sharply with the onset of the Covid crisis in March 2020. From a rate of between 6 and 8% of disposable incomes for most of the period between 2013 and 2019, and reaching 9% in 2019 and early 2020, the rate jumped to 14% in March and then 34% in April 2020. Such a jump is unprecedented in peacetime. The only time there has been anything similar was during World War II.

The data for this chart (and those below) were calculated from data published by the Bureau of Economic Analysis (BEA) as part of the National Income and Product Accounts. And while the GDP estimates themselves are only presented on a quarterly basis, the BEA provides monthly estimates for Personal Income, its sources (wages, etc.), Personal Taxes paid and Transfers received, and how the income thus derived is then used for consumption expenditures and other outlays, and residually for Personal Savings. See in particular Table 2.6 in the NIPA accounts. All the figures used here are seasonally adjusted and (where relevant) at annual rates.

The Personal Savings rate is defined as Personal Savings as a share of Disposable Personal Income, where Disposable Personal Income is Personal Income as received in the market (from wages; interest, dividends, and rents received; and income from unincorporated businesses) less Personal Taxes paid plus Personal Transfers received. These Personal Transfers include that received from Social Security, Medicare, Medicaid, Veterans’ benefits, unemployment compensation, and other such programs, but during the Covid crisis there were also major transfers from the various Covid relief bills (the direct stimulus checks, the paycheck protection program, grants to small as well as large businesses, and much more) as well as from a large jump in unemployment compensation.

The series of Covid relief measures were huge. The total appropriated under the six packages passed for Covid relief (five while Trump was president and one early in the Biden administration) sums to $5.7 trillion. To put this in perspective, the total paid in federal individual income taxes each year is only about $2.6 trillion. Spread over two years, the $5.7 trillion came to 12.8% of the GDP of 2020 and 2021 together. A bit more than two-thirds of that money was appropriated under the bills signed into law by Trump, and a bit less than one-third by Biden. And while the appropriations were passed by Congress with bipartisan (indeed often unanimous) support while Trump was president, the American Rescue Plan signed by Biden on March 11, 2021, received zero votes from Republicans in Congress.

The Covid relief bills provided massive transfers to households (in addition to massive transfers to the corporate sector as well). But especially with the lockdowns, and then continuing to a lesser extent once the lockdowns were lifted due to Covid concerns (thus leading to less travel, less eating out at restaurants, etc.), consumption expenditures by households fell. Much of the transfers received under the Covid relief bills hence ended up accumulating in savings balances (including regular bank accounts). One can see in the chart at the top of this post the peaks in April 2020, January 2021, and March 2021. These coincided with when what is commonly referred to as the “stimulus checks” – of $1,200, $600, and $1,400 respectively – were sent out.

As conditions normalized, the savings rate came down as the Covid relief measures wound down and as consumption recovered. But then the savings rate continued to fall to levels well below those of 2019 and before. The next section will review what was behind this.

C. Personal Incomes, Personal Disposable Income, and Consumption

The paths followed for Personal Income and its components, from 2013 through to October 2022, are shown in the following chart:

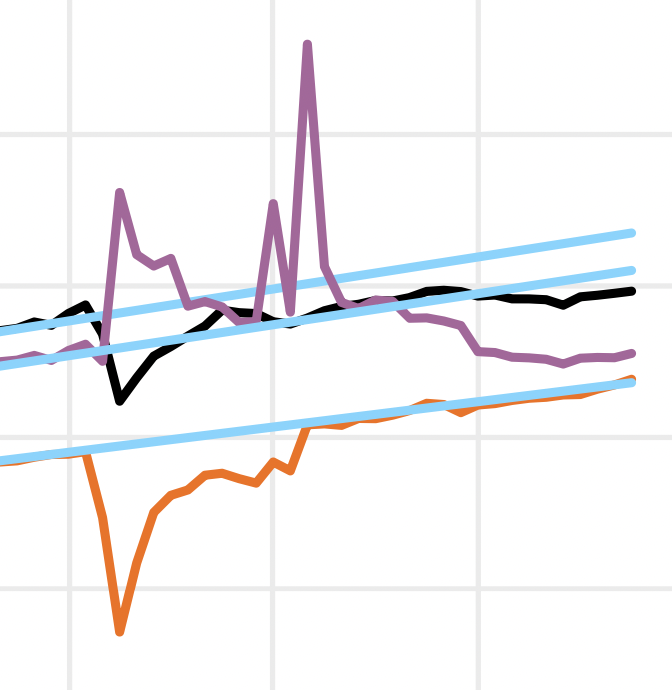

The top three curves show the levels (in constant 2012 dollars) of Personal Income before Taxes and Transfers (in black), Disposable Personal Income (in purple), and Personal Outlays (in orange). Personal Outlays are in essence almost the same as Personal Consumption Expenditures, but not quite. Personal Consumption Expenditures accounted for almost all of Personal Outlays consistently throughout this period (never less than 96.0% nor more than 97.1%), but Personal Outlays also include non-mortgage interest payments (mortgage interest is included in housing expenditures) and small amounts of transfers of households to the rest of the world (i.e. overseas, probably mostly to family) and to government. But since Personal Outlays are almost entirely Personal Consumption Expenditures, and their paths almost identical (just shifted slightly due to the steady 96 to 97% share), we will use the two concepts interchangeably for the purposes here.

The top three curves show the levels (in constant 2012 dollars) of Personal Income before Taxes and Transfers (in black), Disposable Personal Income (in purple), and Personal Outlays (in orange). Personal Outlays are in essence almost the same as Personal Consumption Expenditures, but not quite. Personal Consumption Expenditures accounted for almost all of Personal Outlays consistently throughout this period (never less than 96.0% nor more than 97.1%), but Personal Outlays also include non-mortgage interest payments (mortgage interest is included in housing expenditures) and small amounts of transfers of households to the rest of the world (i.e. overseas, probably mostly to family) and to government. But since Personal Outlays are almost entirely Personal Consumption Expenditures, and their paths almost identical (just shifted slightly due to the steady 96 to 97% share), we will use the two concepts interchangeably for the purposes here.

The light blue lines on top of each are the simple linear regression lines of the paths from January 2013 to February 2020 – a period where each of the paths were extraordinarily stable – and with each then extrapolated at that same trend pace through to October 2022. Not only was there little fluctuation in the paths between January 2013 and February 2020, but it was the same path through both the second term of Obama and the first three years of Trump (followed by the crash in Trump’s fourth year). Indeed, the paths were so stable that the light blue lines of the linear regressions almost obscure the black, purple, and orange paths of the underlying data – up to February 2020.

This then changed abruptly in March 2020 with the onset of the Covid crisis. But before getting to that, we should discuss the three additional curves in the lower part of the chart. Shown are the amounts paid in Personal Current Taxes (in red), Personal Current Transfers (in green), and Personal Savings (in brown). Personal Savings will equal Disposable Personal Income less Personal Outlays (which, as noted above, are basically Personal Consumption Expenditures).

Starting in March 2020, Personal Savings shot upward. This was due to a combination of the far higher transfers (in green – under the first of the major Covid relief packages), the lower Personal Outlays (in orange – due to the lockdowns and general caution in going out to spend money due to the spread of the virus that causes Covid), and, to a lesser extent, lower taxes paid (in red – as the Covid relief measures included allowing tax payments to be deferred). With a good deal of volatility (as a consequence of the timing of the major Covid relief packages), this continued through 2020 and to roughly the spring of 2021.

The resulting impacts on Personal Incomes (before and after taxes and transfers) and on Personal Outlays are shown in the upper right of the chart. A blow-up of this section of the chart may make this easier to follow:

Personal Incomes (before taxes and transfers) recovered quickly, albeit only partially, as the lockdowns were lifted in 2020. They then continued to rise, although at a slower pace, to the latter part of 2021 as the general economy recovered. Since then, they have been largely flat. By October 2022, they were 4.6% below where they would have been had they continued to follow their light-blue regression line for their path prior to March 2020.

Personal Incomes (before taxes and transfers) recovered quickly, albeit only partially, as the lockdowns were lifted in 2020. They then continued to rise, although at a slower pace, to the latter part of 2021 as the general economy recovered. Since then, they have been largely flat. By October 2022, they were 4.6% below where they would have been had they continued to follow their light-blue regression line for their path prior to March 2020.

Disposable Personal Incomes (i.e. after taxes and transfers) rose during the Covid crisis due to the Covid relief packages – as these more than offset the reduction in Personal Incomes during the crisis (when GDP fell and unemployment rose). But by mid-2021, Disposable Personal Incomes had come down to the level of Personal Incomes before taxes and transfers, and then continued to fall as the Covid packages wound down. By October 2022, Disposable Personal Incomes were almost 7% below where they would have been had they continued to follow their light-blue regression line for their path prior to March 2020.

In sharp contrast to Personal Incomes (before or after taxes and transfers), Personal Outlays (or Consumption Expenditures) returned to their previous path by March 2021, and since then have followed that previous path almost exactly. They could do this only because households could draw down on the high savings balances they had built up during the Covid crisis period. But there is only so much in those savings balances. How long might they last?

D. Excess Savings Balances

Savings rates shot up with the onset of the Covid crisis – due to the transfers received and the difficulties in spending – but the savings balances are now being drawn down. While the resulting growth in private consumption expenditures has accounted for much of the growth in the demand for GDP in 2021 and continuing into 2022, those excess savings balances cannot last forever.

A crude calculation can be made of how much might be in those savings balances and how long they might last. It can only be crude as one cannot know with any certainty how much would have been saved in the absence of the Covid crisis and all the impacts it had, nor can one know what returns might have been earned on those savings balances (returns that would depend on how they might have been invested – or not).

Savings rates were relatively stable between 2013 and early 2020 (as seen in the chart at the top of this post), and it is reasonable to assume savings rates would have been similar in the absence of the Covid crisis. For the purposes here, I looked at scenarios where the savings rate would have remained at its average over 2013 to 2019 (which was 7.3%), or at its somewhat higher average over 2017 to 2019 (of 7.9%). I also assumed, in part for simplicity, that there was no return earned on these excess savings balances. This is not unreasonable, as much of what was received under the Covid relief packages were left to accumulate in bank accounts where there was no return. Interest rates on CDs and such have also been very low for most of this period (and negative when adjusted for inflation). And to the extent the funds were invested in the stock market (or in bitcoins!), the returns will depend very much on precisely when the investments were made. The markets were going up for much of the period but now have come down – and sharply.

When the actual savings rates were higher than those assumed in the scenarios (of 7.3% or 7.9%), an excess savings balance was built up, and when the actual savings rates were below these benchmarks, these savings balances were brought down. Expressed as a share of GDP, the resulting excess balances were:

The balances grew, often rapidly, to March 2021 and then peaked in August 2021 at about 10 to 11% of GDP (depending on what base savings rate is assumed). Since then, those balances have come down. Based on the pace of their fall in the most recent six months, they could last for another 18 or 23 months – i.e. for another one and a half to two years – depending on the base savings rate assumed. That is, they would carry over into 2024, and possibly be all used up just prior to election day in 2024.

The balances grew, often rapidly, to March 2021 and then peaked in August 2021 at about 10 to 11% of GDP (depending on what base savings rate is assumed). Since then, those balances have come down. Based on the pace of their fall in the most recent six months, they could last for another 18 or 23 months – i.e. for another one and a half to two years – depending on the base savings rate assumed. That is, they would carry over into 2024, and possibly be all used up just prior to election day in 2024.

There is a good deal of uncertainty in any such forecast – in part due to the factors discussed above that make any such estimate of excess savings balances only approximate. But there are also issues in what might transpire going forward. The estimate that the balances might last for another year and a half to two years is based on a simple extrapolation of the extent to which such balances (as imperfectly estimated) have come down over the past half year. That pace might accelerate. For example, if Disposable Personal Income widens further from its trend path (this might have stopped in the last few months, but it is still early and hard to say), while Personal Consumption continues to rise according to its trend path, then Personal Savings will fall further and the pace at which the savings balances will be brought down will accelerate. On the other hand, if the economy weakens and unemployment rises, consumers may become more cautious and decide to conserve their savings balances.

So one should draw only broad conclusions. But the data does suggest that the excess savings balances built up during the Covid crisis remain significant, and could provide support to continued growth in Personal Consumption Expenditures for some time – perhaps a year or more. Many had assumed – including me before I looked at the data in this way – that the strong Personal Consumption Expenditures of the last two years would be diminishing soon, as excess savings balances were being used up. But this data suggests that strong consumption growth might persist for another year or more. What does this imply for the macro economy?

E. Macro Implications

Inflation has been high – at 6 to over 8% year-on-year by various measures. This is far in excess of the goal of the Fed of an inflation rate of around 2%. In response, the Fed has been aggressively raising the short-term interest rates it controls, as well as reducing its holdings of bonds on its balance sheet (with the aim of raising longer-term interest rates). Higher interest rates can be expected to reduce demand for investment (in particular in long-lived assets such as housing and other structures), and this lower demand will reduce pressures on prices.

Inflation had averaged around 2% – or even less – since the mid-1990s, but then rose as the economy recovered from the Covid crisis. As discussed above, Personal Consumption Expenditures recovered quickly and strongly, with this made possible by the high savings balances that had been built up following the series of Covid relief packages while consumption was limited. But the strong consumption expenditure demands that followed in 2021 and 2022 then faced often limited supplies due to supply chain difficulties as well as the cutbacks in production generally during the peak of the Covid crisis in 2020. And some items of production cannot be placed into an inventory to be sold later. For example, a restaurant produces meals for diners, but a meal that was not produced and sold during the Covid crisis cannot simply be kept somewhere and then sold later. The meal not produced is gone forever.

The result has been a classic “demand-pull” inflation. While the labor market is now tight, with unemployment the lowest it has been for more than a half-century, increases in nominal wages have fallen short of inflation. That is, real wages have been falling, and one cannot attribute the inflation observed as primarily stemming from cost-push factors.

The Fed is thus raising interest rates to limit investment demand, and hence aggregate demand. Whether it will be able to do this without sparking a general recession is the challenge it is facing. While not impossible, it will certainly be tricky. In addition, federal fiscal policy will also likely be acting in the direction of reducing demand. Federal fiscal expenditures fell sharply in FY2022, as the Covid relief packages wound down. As I write this, Congress has yet to approve a budget for FY2023, but the most recent forecast of the Congressional Budget Office (from July) was that federal fiscal expenditures would fall a further 1.2% of GDP in FY2023. And with Republicans controlling the House starting in January, it is not likely that fiscal spending will be allowed to respond should the need arise next year due to a downturn developing.

In this sensitive balance of policies – with the Fed seeking to constrain demand but not by too much, and fiscal expenditures unresponsive should conditions change – what will happen to personal consumption expenditures will be critical. A concern of many has been that such consumption expenditures might also be abruptly reduced once the excess in savings balances built up during the Covid crisis had become used up. Inflation might well then come down quickly, but possibly with the economy falling into a recession as well.

The analysis above suggests that personal consumption expenditures – growing as it has over the last year and a half – could still be sustained through 2023. If so, the likelihood of a recession in 2023 will be reduced (although still possible – depending on what the Fed does). But conditions in 2024 might well then become more difficult to manage. With the House controlled by the Republicans, who have said they will seek to force through cuts in the federal budget (as they did following their election win in 2010), a fiscal response to the changing conditions might not be forthcoming. The Fed may be forced to switch rapidly from raising interest rates to cutting them, in an effort to stem a downturn.

It will likely not be easy to manage. And with 2024 a presidential election year, there may well also be political factors complicating any response.

You must be logged in to post a comment.