A. Introduction

The Bureau of Economic Analysis (BEA) released on July 27 its initial estimate of GDP growth in the second quarter of 2018 (what it technically calls its “advance estimate”). It was a good report: Its initial estimate is that GDP grew at an annualized rate of 4.1% in real terms in the quarter. Such growth, if sustained, would be excellent.

But as many analysts noted, there are good reasons to believe that such a growth rate will not be sustained. There were special, one-time, factors, such as that the second quarter growth (at a 4.1% annual rate) had followed a relatively modest rate of growth in the first quarter of 2.2%. Taking the two together, the growth was a good, but not outstanding, rate of 3.1%.

More fundamentally, with the economy now at full employment, few (other than Trump) expect growth at a sustained rate of 4% or more. Federal Reserve Board members, for example, on average expect GDP growth of 2.8% in 2018 as a whole, with this coming down to a rate of 1.8% in the longer run. And the Congression Budget Office (in forecasts published in April) is forecasting GDP growth of 3.0% in 2018, coming down to an average rate of 1.8% over 2018 to 2028. The fundamental issue is that the population is aging, so the growth rate of the labor force is slowing. As discussed in an earlier post on this blog, unless the productivity of those workers started to grow at an unprecedented rate (faster than has ever been achieved in the post-World War II period), we cannot expect GDP to grow for a sustained period going forward at a rate of 3%, much less 4%.

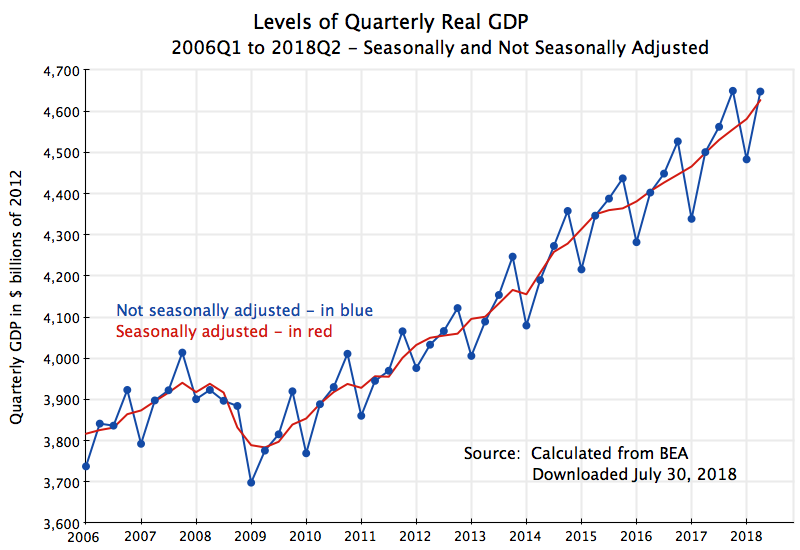

But there will be quarter to quarter fluctuations. As seen in the chart at the top of this post covering the period just since 2006, there have been a number of quarters in recent years where GDP grew at an annualized rate of 4% or more. Indeed, growth reached 5.1% in the second quarter of 2012, with this followed by an also high 4.9% rate in the next quarter. But it then came back down. And there were also two quarters (setting aside the period of the 2008/09 recession) which had growth of a negative 1.0%. On average, GDP growth was around 2% (at an annual rate) during Obama’s two terms in office (2.2% annually from the end of the recession in mid-2009).

Seen in this context, the 4.1% rate in the initial estimate for the second quarter of 2018 was not special. There have been a number of such cases (and with even substantially higher growth rates for a quarter or even two) in the recent past, even though average growth was just half that. The quarterly rates bounce around. But it is of interest to examine why they bounce around so much, and that is the purpose of this blog post.

B. Reasons for this Volatility

There are a number of reasons why one should not be surprised that these quarter to quarter growth rates in GDP vary as they do. I will present several here. And note that these reasons are not mutually exclusive. Several of them could be acting together and be significant factors in any given quarter.

a) There may have been actual changes in growth:

To start, and to be complete, one should not exclude the possibility that the growth in the quarter (or the lack of it) was genuine. Perhaps output did speed up (or slow down) as estimated. Car plants might go on extra shifts (or close for a period) due to consumers wanting to buy more cars (or fewer cars) in the period for some reason. There might also be some policy change that might temporarily spur production (or the opposite). For example, Trump’s recent trade measures, and the response to them from our trading partners, may have brought forward production and trade that would have been undertaken later in the year, in order to avoid tariffs threatened to be imposed later. This could change quarterly GDP even though GDP for the year as a whole will not be affected positively (indeed the overall impact would likely be negative).

[Side note: But one special factor in this past quarter, cited in numerous news reports (see, for example, here, here, here, here, and here), was that a jump in exports of soybeans was a key reason for the higher-than-recently-achieved rate of GDP growth. This was not correct. Soybean exports did indeed rise sharply, with this attributed to the response threatened by China and others to the new tariffs Trump has imposed. China and others said they would respond with higher tariffs of their own, targeted on products such as soybeans coming from the US. There was thus a rush to export soybeans in the period between when China first announced they would impose such retaliatory tariffs (in late March) and when they were then imposed (ultimately on July 6).

But while soybean exports did indeed increase sharply in the April to June quarter, soybeans are a crop that takes many months to grow. Whatever increase in shipments there was had to come out of inventories. An increase in exports would have to be matched by a similar decrease in inventories, with this true also for corn and other such crops. There would be a similar issue for any increase in exports of Kentucky bourbon, also a target of retaliatory tariffs. Any decent bourbon is aged for at least three years.

One must keep in mind that GDP (Gross Domestic Product) is a measure of production, and the only production that might have followed from the increased exports of soybeans or similar products would have been of packing and shipping services. But packing and shipping costs are only a relatively small share of the total value of the products being exported.

Having said that, one should not then go to the opposite extreme and assume that the threatened trade war had no impact on production and hence GDP in the quarter. It probably did. With tariffs and then retaliatory tariffs being threatened (but to be imposed two or three months in the future), there were probably increased factory orders to make and ship various goods before such new tariffs would enter into effect. Thus there likely was some impact on GDP, but to an extent that cannot be quantified in what we see in the national level accounts. And with such factory orders simply bringing forward orders that likely would have been made later in the year, one may well see a fallback in the pace of GDP growth in the remainder of the year. But there are many other factors as well affecting GDP growth, and we will need to wait and see what the net impact will be.]

So one should not exclude the possibility that the fluctuation in the quarterly growth rate is real. But it could be due to many other factors as well, as we will discuss below.

b) Change at an Annualized Rate is Not the Change in a Quarter:

While easily confused, keep in mind also that in the accounts as normally published and presented in the US, the rates of growth of GDP (and of the other economic variables) are shown as annual equivalent rates. The actual change in the quarter is only about one-fourth of this (a bit less due to compounding). That is, in the second quarter of 2018, the BEA estimated that GDP (on a seasonally adjusted basis, which I will discuss below as a separate factor) grew by 1.00% (and yes, exactly 1.00% within two significant digits). But at an annualized rate (some say “annual rate”, and either term can be used), this would imply a rate of growth of 4.06% (which rounded becomes 4.1%). It is equal to slightly more than 4.0% due to compounding. [Technically, 1% growth in the quarter means 1.00 will grow to 1.01, and taking 1.01 to the fourth power yields 1.0406, or an increase of 4.06%.]

Thus it is not correct to say that “GDP grew by 4.1% in the second quarter”. It did not – it grew by 1.0%. What is correct is to say that “GDP grew at an annualized rate of 4.1% in the second quarter”.

Not all national statistical agencies present such figures in annualized terms. European agencies, for example, generally present the quarterly growth figures as simply the growth in the quarter. Thus, for example, Eurostat on June 7 announced that GDP in the eurozone rose by an estimated 0.4% in the first quarter of 2018. This 0.4% was the growth in the quarter. But that 0.4% growth figure would be equivalent to growth of 1.6% on an annualized basis (actually 1.61%, if the growth had been precisely 0.400%). Furthermore, the European agencies will generally also focus on the growth in GDP over what it had been a year earlier in that same quarter. In the first quarter of 2018, this growth over the year-earlier period was an estimated 2.5% according to the Eurostat release. But the growth since the year-earlier period is not the same as the growth in the current quarter at an annualized rate. They can easily be confused if one is not aware of the conventions used by the different agencies.

c) Don’t confuse the level of GDP with the change in GDP:

Also along the lines of how we might misleadingly interpret figures, one needs to keep in mind that while the quarterly growth rates can, and do, bounce around a lot, the underlying levels of GDP are really not changing much. While a 4% annual growth rate is four times as high as a 1% growth rate, for example, the underlying level of GDP in one calendar quarter is only increasing to a level of about 101 (starting from a base of 100 in this example) with growth at a 4% annual rate, versus to a level of 100.25 when growth is at an annual rate of 1%. While such a difference in growth rates matters a great deal (indeed a huge deal) if sustained over time, the difference in any one quarter is not that much.

Indeed, I personally find the estimated quarter to quarter levels of GDP in the US (after seasonal adjustment, which will be discussed below) to be surprisingly stable. Keep in mind that GDP is a flow, not a stock. It is like the flow of water in a river, not a stock such as the body of water in a reservoir. Flows can go sharply up and down, while stocks do not, and some may mistakenly treat the GDP figures in their mind as a stock rather than a flow. GDP measures the flow of goods and services produced over some period of time (a calendar quarter in the quarterly figures). A flow of GDP to 101 in some quarter (from a base of 100 in the preceding quarter) is not really that different to an increase to 100.25. While this would matter (and matter a good deal) if the different quarterly increases are sustained over time, this is not that significant when just for one quarter.

d) Statistical noise matters:

Moving now to more substantive reasons why one should expect a significant amount of quarter to quarter volatility, one needs to recognize that GDP is estimated based on surveys and other such sources of statistical information. The Bureau of Economic Analysis (BEA) of the US Department of Commerce, which is responsible for the estimates of the GDP accounts in the US (which are formally called the National Income and Product Accounts, or NIPA), bases its estimates on a wide variety of surveys, samples of tax returns, and other such partial figures. The estimates are not based on a full and complete census of all production each quarter. Indeed, such an economic census is only undertaken once every five years, and is carried out by the US Census Bureau.

One should also recognize that an estimate of real GDP depends on two measures, each of which is subject to sampling and other error. One does not, and cannot, measure “real GDP” directly. Rather, one estimates what nominal GDP has been (based on estimates in current dollars of the value of all economic transactions that enter into GDP), and then how much prices have changed. Price indices are estimated based on the prices of surveyed samples, and the components of real GDP are then estimated from the nominal GDP of the component divided by the relevant price index. Real GDP is only obtained indirectly.

There will then be two sets of errors in the measurements: One for the nominal GDP flows and one for the price indices. And surveys, whether of income flows or of prices, are necessarily partial. Even if totally accurate for the firms and other entities sampled, one cannot say with certainty whether those sampled in that quarter are fully representative of everyone in the economy. This is in particular a problem (which the BEA recognizes) in capturing what is happening to newly established firms. Such firms will not be included in the samples used (as they did not exist when the samples were set up) and the experiences of such newly established firms can be quite different from those of established firms.

And what I am calling here statistical “noise” encompasses more than simply sampling error. Indeed, sampling error (the fact that two samples will come up with different results simply due to the randomness of who is chosen) is probably the least concern. Rather, systemic issues arise whenever one is trying to infer measures at the national level from the results found in some survey. The results will depend, for example, on whether all the components were captured well, and even on how the questions are phrased. We will discuss below (in Section C, where we look at a comparison of estimates of GDP to estimates of Gross Domestic Income, or GDI, which in principle should be the same) that the statistical discrepancy between the estimates of GDP and GDI does not vary randomly from one quarter to the next but rather fairly smoothly (what economists and statisticians call “autocorrelation” – see Section C). This is an indication that there are systemic issues, and not simply something arising from sample randomness.

Finally, even if that statistical error was small enough to allow one to be confident that we measured real GDP within an accuracy of just, say, +/- 1%, one would not then be able to say whether GDP in that quarter had increased at an annualized rate of about 4%, or decreased by about 4%. A small quarterly difference looms large when looked at in terms of annualized rates.

I do not know what the actual statistical error might be in the GDP estimates, and it appears they are well less than +/- 1% (based on the volatility actually observed in the quarter to quarter figures). But a relatively small error in the estimates of real GDP in any quarter could still lead to quite substantial volatility in the estimates of the quarter to quarter growth.

e) Seasonal adjustment is necessary, but not easy to do:

Economic activity varies over the course of the year, with predictable patterns. There is a seasonality to holidays, to when crops are grown, to when students graduate from school and enter the job market, and much much more. Thus the GDP data we normally focus on has been adjusted by various statistical methods to remove the seasonality factor, making use of past data to estimate what the patterns are.

The importance of this can be seen if one compares what the seasonally adjusted levels of GDP look like compared to the levels before seasonal adjustment. Note the level of GDP here is for one calendar quarter – it will be four times this at an annual rate:

There is a regular pattern to GDP: It is relatively high in the last quarter of each year, relatively low in the first quarter, and somewhere in between in the second and third quarters. The seasonally adjusted series takes account of this, and is far smoother. Calculating quarterly growth rates from a series which has not been adjusted for seasonality would be misleading in the extreme, and not of much use.

But adjusting for seasonality is not easy to do. While the best statisticians around have tried to come up with good statistical routines to do this, it is inherently difficult. A fundamental problem is that one can only look for patterns based on what they have been in the past, but the number of observations one has will necessarily be limited. If one went back to use 20 years of data, say, one would only have 20 observations to ascertain the statistical pattern. This is not much. One could go back further, but then one has the problem that the economy as it existed 30 or 40 years ago (and indeed even 20 years ago) was quite different from what it is now, and the seasonal patterns could also now be significantly different. While there are sophisticated statistical routines that have been developed to try to make best use of the available data (and the changes observed in the economy over time), this can only be imperfect.

Indeed, the GDP estimates released by the BEA on July 27 incorporated a number of methodological changes (which we will discuss below), one of which was a major update to the statistical routines used for the seasonal adjustment calculations. Many observers (including at the BEA) had noted in recent years that (seasonally adjusted) GDP growth in the first quarter of each year was unusually and consistently low. It then recovered in the second quarter. This did not look right.

One aim of the update to the seasonal adjustment statistical routines was to address this issue. Whether it was fully successful is not fully clear. As seen in the chart at the top of this post (which reflects estimates that have been seasonally adjusted based on the new statistical routines), there still appear to be significant dips in the seasonally adjusted first quarter figures in many of the years (comparing the first quarter GDP figures to those just before and just after – i.e. in 2007, 2008, 2010, 2011, 2014, and perhaps 2017 and 2018. This would be more frequent than one would expect if the residual changes were now random over the period). However, this is an observation based just on a simple look at a limited sample. The BEA has looked at this far more carefully, and rigorously, and believes that the new seasonal adjustment routines it has developed have removed any residual seasonality in the series as estimated.

f) The timing of weekends and holidays may also enter, and could be important:

The production of the goods and services that make up the flow of GDP will also differ on Saturdays, Sundays, and holidays. But the number of Saturdays, Sundays, and certain holidays may differ from one year to the next. While there are normally 13 Saturdays and 13 Sundays in each calendar quarter, and most holidays will be in the same quarter each year, this will not always be the case.

For example, there were just 12 Sundays in the first quarter of 2018, rather than the normal 13. And there will be 14 Sundays in the third quarter of 2018, rather than the normal 13. In 2019, we will see a reversion to the “normal” 13 Sundays in each of the quarters. This could have an impact.

Assume, just for the sake of illustration, that production of what goes into GDP is only one-half as much on a Saturday, Sunday, or holiday, than it is on a regular Monday through Friday workday. It will not be zero, as many stores, as well as certain industrial plants, are still open, and I am just using the one-half for illustration. Using this, and based on a simple check of the calendars for 2018 and 2019, one will find there were 62 regular, Monday through Friday, non-holiday workdays in the first quarter of 2018, while there will be 61 such regular workdays in the first quarter of 2019. The number of Saturdays, Sundays, and holidays were 28 in the first quarter of 2018 (equivalent to 14 regular workdays in terms of GDP produced, assuming the one-half figure), while the number of Saturdays, Sundays, and holidays will be 29 in the first quarter of 2019 (equivalent to 14.5 regular workdays). Thus the total regular work-day equivalents will be 76 in 2018 (equal to 62 plus 14), falling to 75.5 in 2019 (equal to 61 plus 14.5). This will be a reduction of 0.7% between the periods in 2018 and 2019 (75.5/76), or a fall of 2.6% at an annualized rate. This is not small.

The changes due to the timing of holidays could matter even more, especially for certain countries around the world. Easter, for example, was celebrated in March (the first quarter) in 2013 and 2016, but came in April (the second quarter) in 2014, 2015, 2017, and 2018. In Europe and Latin America, it is customary to take up to a week of vacation around the Easter holidays. The change in economic activity from year to year, with Easter celebrated in one quarter in one year but a different one in the next, will make a significant difference to economic activity as measured in the quarter.

And in Muslim countries, Ramadan (a month of fasting from sunrise to sunset), followed by the three-day celebration of Eid al-Fitr, will rotate through the full year (in terms of the Western calendar) as it is linked to the lunar cycle.

Hence it would make sense to adjust the quarterly figures not only for the normal seasonal adjustment, but also for any changes in the number of weekends and holidays in some particular calendar quarter. Eurostat and most (but not all) European countries make such an adjustment for the number of working days in a quarter before they apply the seasonal adjustment factors. But I have not been able to find how the US handles this. The adjustment might be buried somehow in the seasonal adjustment routines, but I have not seen a document saying this. If no adjustment is made, then this might explain part of the quarterly fluctuations seen in the figures.

g) There have been, and always will be, updates to the methodology used:

As noted above, the GDP figures released on July 27 reflected a major update in the methodology followed by the BEA to arrive at its GDP estimates. Not only was there extensive work on the seasonal adjustment routines, but there were definitional and other changes. The accounts were also updated to reflect the findings from the 2012 Economic Census, and prices were changed from a previous base of 2009 to now 2012. The July 27 release summarized the changes, and more detail on what was done is available from a BEA report issued in April. And with the revisions in definitions and certain other methodological changes, the BEA revised its NIPA figures going all the way back to 1929, the first year with official GDP estimates.

The BEA makes such changes on a regularly scheduled basis. There is normally an annual change released each year with the July report on GDP in the second quarter of the year. This annual change incorporates new weights (from recent annual surveys) and normally some limited methodological changes, and the published estimates are normally then revised going back three and a half years. See, for example, this description of what was done in July 2017.

On top of this, there is then a much larger change once every five years. The findings from the most recent Economic Census (which is carried out every five years) are incorporated, seasonal adjustment factors are re-estimated, and major definitional or methodological changes may be incorporated. The July 2018 release reflected one of those five-year changes. It was the 15th such comprehensive revision to the NIPA accounts undertaken by the BEA.

I stress this to make the point that the GDP figures are estimates, and as estimates are always subject to change. The professionals at the BEA are widely admired around the world for the quality of their work, and do an excellent job in my opinion. But no estimates will ever be perfect. One has to recognize that there will be a degree of uncertainty surrounding any such estimates, and that the quarter to quarter volatility observed will derive at least in part from the inherent uncertainty in any such estimates.

C. Estimates of GDP versus Estimates of GDI

One way to develop a feel for how much the changes in quarterly GDP may be due to the inherent uncertainty in the estimates is to compare it to the estimated quarterly changes in Gross Domestic Income (GDI). GDP (Gross Domestic Product) measures the value of everything produced. GDI measures the value of all incomes (wages, profits, rents, etc.) generated. In principle, the totals should be the same, as the value of whatever is produced accrues to someone as income. They should add up to the same thing.

But the BEA arrives at its estimates of GDP and of GDI by different routes. As a consequence, the estimates of the totals will then differ. The differences are not huge in absolute amount, nor have they grown over time (as a share of GDP or of GDI). That is, on average the estimates match each other over time, with the same central tendency. But they differ by some amount in any individual quarter, and hence the quarter to quarter growth rates will differ. And for the reasons reviewed above, those slight changes in the levels in any individual quarter can translate into often major differences in the growth rates from one quarter to the next. And these differences may appear to be particularly large when the growth rates are then presented in annualized terms.

For the period since 2006, the two sets of growth rates were (where the initial estimate for the second quarter of 2018 will not be available until the end-August figures come out):

As is seen, the alternative estimates of growth in any individual quarter can be quite different. There was an especially large difference in the first quarter of 2012, when the estimated growth in GDP was 3.2% at an annual rate, while the estimated growth in GDI was a giant 8.7%.

Which is correct? Was the growth rate in the first quarter of 2012 3.2% (as found with the GDP estimate) or 8.7% (as found with the GDI estimate)? The answer is we do not know, and indeed that probably neither is correct. What is most likely is that the true figure is probably somewhere in between.

Furthermore, and also moderating what the impact on the differences in the respective estimated growth rates will be, it is not the case that the estimates of GDP and GDI are statistically independent of each other, with the two bouncing around randomly with respect to each other. Rather, if one looks at what the BEA calls the “statistical discrepancy” (the difference between GDP and GDI), one finds that if, say, the estimate of GDP were above the estimate of GDI in one quarter, then it likely would also be above in the next quarter. Not by the same amount, and the differences would evolve over time, but moving more like waves than as balls ricocheting around. Economists and statisticians refer to this as “autocorrelation”, and it indicates that there is some systemic error in the estimates of GDP and of GDI, which carries over from one quarter to the next. What the source of that is, we do not know. If we did know, then it would be eliminated. But the fact such autocorrelation exists tells us that there is some source of systemic error in the measures of GDP and GDI, and we have not been able to discover the source.

Estimates are estimates. We need to recognize that there will be statistical uncertainty in any such figures. Even if they even out over time, the estimated growth from one quarter to the next will reflect such statistical volatility. The differences seen in the estimated rates of growth in any one quarter for total output (estimated by way of GDP versus by way of GDI) provides a useful benchmark for how to judge the reported changes seen in growth for GDP in any individual quarter. The true volatility (for purely statistical reasons) is likely to be at least as much, if not more.

D. Conclusion

There are many reasons, then, to expect the quarterly growth figures to bounce around. One should not place too much weight on the estimates from any individual quarter. It is the longer term trends that matter. The estimated figure for growth in GDP of 4.1% in the second quarter was not out of line with what has been seen in a number of quarters in recent years. But growth since mid-2009 has only been about one half as much on average, despite several quarters when estimated growth was well in excess of 4.1%.

To conclude, some may find of interest three country cases I am personally familiar with which illustrate why one needs to exercise care, and with an understanding of the country context, when considering what is meaningful or not for reported figures on GDP growth. The countries are Japan, China, and an unidentified, but newly independent, former colony in the 1960s.

a) Japan: In the late 1990s / early 2000s, while holding a position within the World Bank Group, I was responsible for assessments of the prospects and risks of the countries of East Asia where the World Bank was active. This was not long after the East Asia crisis of 1997, and the countries were just beginning to recover. Japan was important, both as a trading partner to the others and because Japan itself had gone through a somewhat similar crisis following 1990, when the Japanese financial bubble burst.

As part of this, I followed closely the quarterly GDP growth figures for Japan. But as many analysts at the time noted, the quarter to quarter figures behaved in ways that were difficult to understand. Components went up when one would have thought they would go down (and vice versa), the quarterly changes were far more extreme than seen elsewhere, and in general the quarter to quarter fluctuations were difficult to make sense of. The volatility in the figures was far greater than one would have expected for an economy such as Japan’s.

This view among analysts was such a common one that the government agency responsible for the estimates felt it necessary to issue a news release in June 2000 defending its work and addressing a number of the concerns that had been raised.

I have no doubt that the Japanese government officials responsible for the estimates were well-qualified and serious professionals. But it is not easy to estimate GDP and its components, the underlying data on which the statisticians relied might have had problems (including sample sizes that were possibly too small), and there may have been segments of the economy (in the less formal sectors) which might not have been captured well.

I have not followed closely in recent years, and do not know if the issues continue. But Japan’s case illustrates that even a sophisticated agency, with good professionals, can have difficulty in arriving at GDP estimates that behave as one would expect.

b) China: The case of China illustrates the mirror image problem of what was found in Japan. While the Japanese GDP estimates bounced around far too sharply from one quarter to the next, the GDP estimates for China showed remarkable, and not believable, stability.

Chinese growth rates have normally been presented as growth of GDP in the current period over what it was in the same period one year ago. Seasonal adjustment is then not needed, and indeed China only started to present seasonally adjusted figures in 2011. However, these estimates are still not fully accepted by many analysts. Comparing GDP in the current quarter to what it was in the same quarter a year before overcomes this, but at the cost that it does not present information on growth just in the quarter, as opposed to total growth over the preceding year.

And the growth rates reported over the same quarter in the preceding year have been shockingly smooth. Indeed, in recent years (from the first quarter of 2015 through to the recently released figures for the second quarter of 2018), China’s reported growth of its GDP over the year-earlier period has not been more than 7.0% nor less than 6.7% in each and every quarter. Specifically, the year on year GDP growth rates from the first quarter of 2015 through to the second quarter of 2018 were (in sequence): 7.0%, 7.0%, 6.9%, 6.8%, 6.7%, 6.7%, 6.7%, 6.8%, 6.9%, 6.9%, 6.8%, 6.8%, 6.8%, and 6.7% (one can find the figures in, for example, the OECD database). Many find this less than credible.

There are other problems as well in the Chinese numbers. For example, it has often been the case that the reported growth in provincial GDP of the 31 provincial level entities in China was higher in almost all of the 31 provinces, and sometimes even in all of the provinces, than GDP growth was in China as a whole. This is of course mathematically impossible, but not surprising when political rewards accrue to those with fast reported growth.

With such weak credibility, analysts have resorted to coming up with proxies to serve as indicators of what quarter to quarter might have been. These might include electricity consumption, or railway tonnage carried, or similar indicators of economic production. Indeed, there is what has been labeled the “Li index”, named after Li Keqiang (who was vice premier when he formulated it, and later China’s premier). Li said he did not pay much attention to the official GDP statistics, but rather focused on a combination of electricity production, rail cargo shipments, and loan disbursements. Researchers at the Federal Reserve Bank of San Francisco who reproduced this and fitted it through some regression analysis found that it worked quite well.

And the index I found most amusing is calculated using nighttime satellite images of China, with an estimation of how much more night-time illumination one finds over time. This “luminosity” index tracks well what might be going on with China’s GDP.

c) An unidentified, newly independent, former colony: Finally, this is a story which I must admit I received third hand, but which sounds fully believable. In the mid-1970s I was working for a period in Kuala Lumpur, for the Government of Malaysia. As part of an economic modeling project I worked closely with the group in the national statistical office responsible for estimating GDP. The group was led by a very capable, and talkative, official (of Tamil origin), who related a story he had heard from a UN consultant who had worked closely with his group in the early 1970s to develop their system of national accounts.

The story is of a newly independent country in the mid-1960s (whose name I was either not told or cannot remember), and its estimation of GDP. An IMF mission had visited it soon after independence, and as is standard, the IMF made forecasts of what GDP growth might be over the next several years. Such forecasts are necessary in order to come up with estimates for what the government accounts might be (as tax revenues will depend on GDP), for the trade accounts, for the respective deficits, and hence for what the financing needs might be.

Such forecasts are rarely very good, especially for a newly independent country where much is changing. But something is needed.

As time passed, the IMF received regular reports from the country on what estimated GDP growth actually was. What they found was that reported GDP growth was exactly what had been forecast. And when asked, the national statisticians responded that who were they to question what the IMF officials had said would happen!

You must be logged in to post a comment.