As is well known, the Social Security Trust Fund will run out in about 2034 (plus or minus a year) if nothing is done. “Running out” means that the past accumulated stock of funds paid in through Social Security taxes on wages, plus what is paid in each year, will not suffice to cover what is due to be paid out that year to beneficiaries. If nothing is done, Social Security payments would then be scaled back by 23% (in 2034, rising to 27% by 2091), to match the amount then being paid in each year.

This would be a disaster. Social Security does not pay out all that much: An average of just $15,637 annually per beneficiary for those in retirement and their survivors, and an average of just $12,452 per beneficiary for those on disability (all as of August 2017). But despite such limited amounts, Social Security accounts for almost two-thirds (63%) of the incomes of beneficiaries age 65 or older, and 90% or more of the incomes of fully one-third of them. Scaling back such already low payments, when so many Americans depend so much on the program, should be unthinkable.

Yet Congress has been unwilling to act, even though the upcoming crisis (if nothing is done) has been forecast for some time. Furthermore, the longer we wait, the more severe the measures that will then be necessary to fix the problem. It should be noted that the crisis is not on account of an aging population (one has pretty much known for 64 years how many Americans would be reaching age 65 now), nor because of a surprising jump in life expectancies (indeed, life expectancies have turned out to be lower than what had been forecast). Rather, as discussed in an earlier post on this blog, the crisis has arisen primarily because wage income inequality has grown sharply (and unexpectedly) since around 1980, and this has pulled an increasing share of wages into the untaxed range above the ceiling for annual earnings subject to Social Security tax ($127,200 currently).

But Congress could act, and there are many different approaches that could be taken to ensure the Social Security Trust Fund remains adequately funded. This post will discuss just one. And that would be not to approve the Trump proposal for what he accurately calls would be a huge cut in taxes, and use the revenues that would be lost under his tax plan instead to shore up the Social Security Trust Fund. As the chart at the top of this post shows (and as will be discussed below), this would more than suffice to ensure the Trust Fund would remain in surplus for the foreseeable future. There would then be no need to consider slashing Social Security benefits in 2034.

The Trump tax plan was submitted to Congress on September 27. It is actually inaccurate to call it simply the Trump tax plan as it was worked out over many months of discussions between Trump and his chief economic aides on one side, and the senior Republican leadership in both the Senate and the Congress on the other side, including the chairs of the tax-writing committees. This was the so-called “Gang of Six”, who jointly released the plan on September 27, with the full endorsement of all. But for simplicity, I will continue to call it the Trump tax plan.

The tax plan would sharply reduce government revenues. The Tax Policy Center (TPC), a respected bipartisan nonprofit, has provided the most careful forecast of the revenue losses yet released. They estimated that the plan would reduce government revenues by $2.4 trillion between 2018 and 2027, with this rising to a $3.2 trillion loss between 2028 and 2037. The lost revenue would come to 0.9% of GDP for the 2018 to 2027 period, and 0.8% of GDP for the 2028 to 2037 period (some of the tax losses under the Trump plan are front-loaded), based on the GDP forecasts of the Social Security Trustees 2017 Annual Report (discussed below). While less than 1% of GDP might not sound like much, such a revenue loss would be significant. As we will see, it would suffice to ensure the Social Security Trust Fund would remain fully funded.

The chart at the top of this post shows what could be done. The curve in green is the base case where nothing is done to shore up the Trust Fund. It shows what the total stock of funds in the Social Security Trust Fund have been (since 1980) and would amount to, as a share of GDP, if full beneficiary payments would continue as per current law. Note that I have included here the trust funds for both Old-Age and Survivors Insurance (OASI) and for Disability Insurance (DI). While technically separate, they are often combined (and then referred to as OASDI).

The figures are calculated from the forecasts released in the most recent (July 2017) mandated regular annual report of the Board of Trustees of the Social Security system. Their current forecast is that the Trust Fund would run out by around 2034, as seen in the chart.

But suppose that instead of enacting the Trump tax plan proposals, Congress decided to dedicate to the Social Security Trust Funds (OASDI) the revenues that would be lost as a consequence of those tax cuts? The curve in the chart shown in red is a forecast of what those tax revenue losses would be each year, as a share of GDP. These are the Tax Policy Center estimates, although extrapolated. The TPC forecasts as published showed the estimated year-by-year losses over the first ten years (2018 to 2027), but then only for the sum of the losses over the next ten years (2028 to 2037). I assumed a constant rate of growth from the estimate for 2027 sufficient to generate the TPC sum for 2028 to 2037, which worked out to a bit over 6.1%. I then assumed the revenue losses would continue to grow at this rate for the remainder of the forecast period.

Note this 6.1% growth is a nominal rate of growth, reflecting both inflation and real growth. The long-run forecasts in the Social Security Trustees report were for real GDP to grow at a rate of 2.1 or 2.2%, and inflation (in terms of the GDP price index) to grow at also 2.2%, leading to growth in nominal GDP of 4.3 or 4.4%. Thus the forecast tax revenue losses under the Trump plan would slowly climb over time as a share of GDP, reaching 2% of GDP by about 2090. This is as one would expect for this tax plan, as the proposals would reduce progressivity in the tax system. As I noted before on this blog and will discuss further below, most of the benefits under the Trump tax plan would accrue to those with higher incomes. However, one should also note that the very long-term forecasts for the outer years should not be taken too seriously. While the trends are of interest, the specifics will almost certainly be different.

If the tax revenues that would be lost under the Trump tax plan were instead used to shore up the Social Security Trust Fund, one would get the curve shown in blue (which includes the interest earned on the balance in the Fund, at the interest rates forecast in the Trustees report). The balance in the fund would remain positive, never dipping below 12% of GDP, and then start to rise as a share of GDP. Even if the TPC forecasts of the revenues that would be lost under the Trump plan are somewhat off (or if Congress makes changes which will reduce somewhat the tax losses), there is some margin here. The forecast is robust.

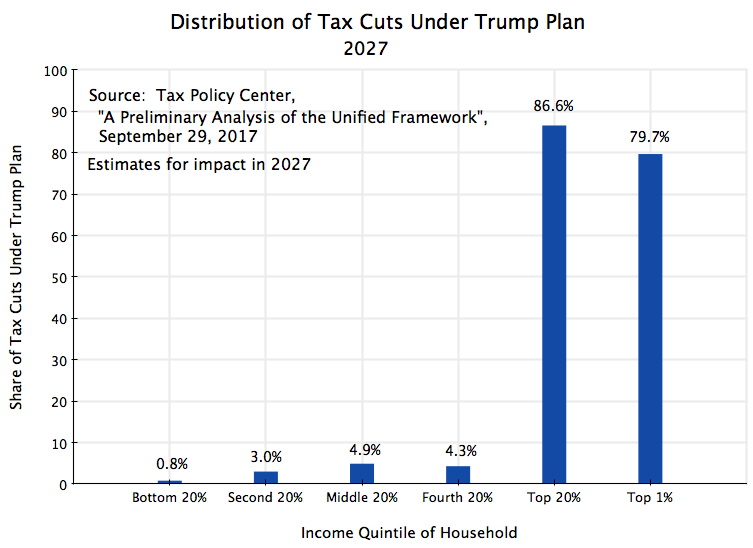

The alternative is to follow the Trump tax plan, and cut taxes sharply. As I noted in my earlier post on this blog on the Trump tax plan, the proposals are heavily weighted to provisions which would especially benefit the rich. The TPC analysis (which I did not yet have when preparing my earlier blog post) has specific estimates of this. The chart below shows who would get the tax cuts for the forecast year of 2027:

The estimate is that 87% of the tax revenues lost under the Trump plan would go to the richest 20% of the population (those households with an income of $154,900 or more in 2027, in prices of 2017). And indeed, almost all of this (80% of the overall total) would accrue just to the top 1%. The top 1% are already pretty well off, and it is not clear why tax cuts focused on them would spur greater effort on their part or greater growth. The top 1% are those households who would have an annual income of at least $912,100 in 2027, in prices of 2017. Most of them would be making more than a million annually.

The Trump people, not surprisingly, do not accept this. They assert that the tax cuts will spur such a rapid acceleration in growth that tax revenues will not in fact be lost. Most economists do not agree. As discussed in earlier posts on this blog, the historical evidence does not support the Trumpian view (the tax cuts under Reagan and Bush II did not lead to any such acceleration in growth; what they did do is reduce tax revenues); the argument that tax cuts will lead to more rapid growth is also conceptually confused and reveals a misunderstanding of basic economics; and with the economy having already reached full employment during the Obama years, there is little basis for the assertion that the economy will now be able to grow at even 3% a year on average (over a mulit-year period) much less something significantly faster. Tax cuts have in the past led to cuts in tax revenues collected, not to increases, and there is no reason to believe this time will be different.

Thus Congress faces a choice. It can approve the Trump tax plan (already endorsed by the Republican leadership in both chambers), with 80% of the cuts going to the richest 1%. Or it could use those revenues to shore up the Social Security Trust Fund. If the latter is done, the Trust Fund would not run out in 2034, and Social Security would be able to continue to pay amounts owed to retired senior citizens and their survivors, as well as to the disabled, in accordance with the commitments it has made.

I would favor the latter. If you agree, please call or write your Senator and Member of Congress, and encourage others to do so as well.

————————————————————————

Update, October 22, 2017

The US Senate passed on October 19 a budget framework for the FY2018-27 period which would allow for $1.5 trillion in lost tax revenues over this period, and a corresponding increase in the deficit, as a consequence of new tax legislation. It was almost fully a party line vote (all Democrats voted against it, while all Republicans other than Senator Rand Paul voted in favor). Importantly, this vote cleared the way (under Senate rules) for it to pass a new tax law with losses of up to $1.5 trillion over the decade, and pass this with only Republican votes. Only 50 votes in favor will be required (with Vice President Pence providing a tie-breaking vote if needed). Democrats can be ignored.

The loss in tax revenues in this budget framework is somewhat less than the $2.4 trillion that the Tax Policy Center estimates would follow in the first decade under the Trump tax plan. But it is still sizeable, and it is of interest to see what this lesser amount would achieve if redirected to the Social Security Trust Fund instead of being used for tax cuts.

The chart above shows what would follow. It still turns out that the Social Security Trust Fund would be saved from insolvency, although just barely this time.

One has to make an assumption as to what would happen to tax revenues after 2027, as well as for what the time pattern would be for the $1.5 trillion in losses over the ten years from FY2018 to 27. With nothing else available, I assumed that the losses would grow over time at the same rate as what is implied in the Tax Policy Center estimates for the losses in the second decade of the Trump tax plan as compared to the losses in the final year of the first decade. As discussed above, these estimates implied a nominal rate of growth of 6.1% a year. I assumed the same rate of growth here, including for the year to year growth in the first decade (summing over that decade to $1.5 trillion).

The result again is that the Social Security Trust Fund would remain solvent for the foreseeable future, although now just marginally. The Trust Fund (as a share of GDP) would just touch zero in the years around 2080, but would then start to rise.

We therefore have a choice. The Republican-passed budget framework has that an increase in the fiscal deficit of $1.5 trillion over the next decade is acceptable. It could be used for tax cuts that would accrue primarily to the rich. Or it could be used to ensure the Social Security system will be able, for the foreseeable future, to keep to its commitments to senior citizens, to their survivors, and to the disabled.

You must be logged in to post a comment.