A. Introduction

In his State of the Union speech last month, President Obama called for a rise in the federal minimum wage from the current $7.25 per hour to a new rate of $9.00 per hour. This would be a 24% increase, but would still mean that someone working full time, 40 hours per week, 52 weeks a year (no vacation), would earn only $18,720 a year. Such a full time worker would still be earning well less than the current federal poverty line for a family of four of $23,050 per year. The proposed increase is modest.

Republican leaders nonetheless immediately denounced the proposal, asserting that raising the minimum wage would hurt, not help, the poor, as they would lose their jobs. They assert that instead of seeing an increase in their wage, the minimum wage workers would be fired. And unlike in many other areas (such as the impact of fiscal policies) the Republican leadership here is making an argument that one would find in an introductory economics course. Elementary economics would indeed argue that in perfectly competitive markets, an increase in the minimum wage would lead to such workers losing their jobs rather than being paid more.

B. Have Increases in the Minimum Wage Led to Higher Unemployment of Such Workers in the Past?

But what is the evidence? If increases in the minimum wage lead to such workers being fired, one would see higher unemployment among such workers very quickly in the months following each increase in the minimum wage in the past. The graphs above show what in fact has happened.

The first graph shows the federal mandated minimum wage since 1950, in real inflation adjusted terms (using the CPI), plus the unemployment rates for all workers and separately for workers aged 16 to 24. The data comes from the Bureau of Labor Statistics, but was downloaded for convenience from FRED, the Federal Reserve Economic Data web site maintained by the Federal Reserve Bank of St. Louis. The unemployment rate for workers aged 16 to 24 is shown separately as one would expect that increases in the minimum wage would increase unemployment especially sharply in that group, if the assertion is correct that increases in the minimum wage lead to such workers losing their jobs. Approximately 51% of the hourly wage workers earning the minimum wage are in this 16 to 24 age group.

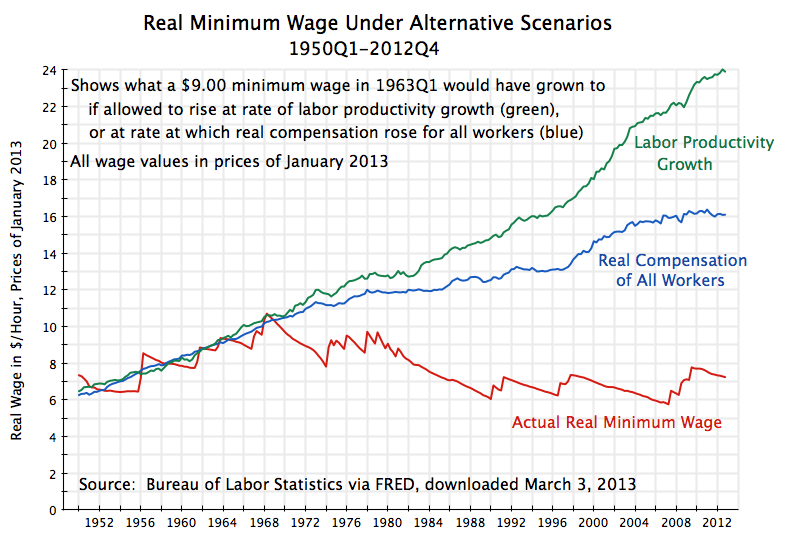

First of all, it is worth noting that the minimum wage, when adjusted to reflect general inflation, is a good deal lower now than a half century ago. It reached a high (in prices of January 2013) of $10.82 in February 1968, and lows of $6.02 in March 1990 and $5.75 in June 2007. It averaged close to $9.00 an hour over the twenty-five years of 1957-81 (inclusive), and is only $7.25 currently (almost 20% less). The Obama proposal is modest, as he has only asked Congress to bring it back to that $9.00 an hour, the rate of a half century ago.

But does one see in the history that increases in the minimum wage lead to a jump in unemployment rates, particularly of the young (and decreases in the minimum wage leading to lower unemployment rates)? Actually, no. Unemployment rates do fluctuate a good deal, as they depend on macro conditions in the economy. But it is hard to see any obvious jump in unemployment rates in the months following the sporadic increases in the real minimum wage we have had over the last more than 60 years.

It is also worth noting that due to the politics of the minimum wage, and the resistance of conservatives and businessmen to higher rates, increases in the minimum wage have been generally infrequent and then relatively large in percentage terms. This thus provides good material for a test of whether increases in the minimum wage lead quickly to jumps in the unemployment rate (particularly of the young). Yet one does not see it.

Any relationship might be hard to recognize in part because of the independent rises and falls in unemployment rates due to macro conditions. The second graph therefore charts the real minimum wage along with a line that shows the ratio of the unemployment rate of those aged 16 to 24 to the unemployment rate for the entire labor force. This ratio exploits the fact that a relatively high share (about 51%, as noted above) of minimum wage workers are young. Thus, if it is in fact true that increases in the minimum wage will lead those making the minimum wage to become unemployed, the higher share of such workers in the ages 16 to 24 category will lead to an increase in that ratio.

But the graph does not show such a relationship. While the real minimum wage has seen many sudden changes, the ratio of unemployment rates often does not then change, and in fact sometimes moves in a direction that is the opposite of what those opposed to increases in the minimum wage would predict. The one possible exception appears to be a blip seen following the February 1968 increase in the minimum wage. But this blip occurs in fact four months later (in June 1968; the time scale is compressed as the chart covers 63 years) and then drops back. But one also sees that the steady decline in the real minimum wage during the 1980s in the Reagan years was accompanied by a rise in the ratio (the opposite of what they would predict), and that the ratio then declined (instead of rising) when the minimum wage was finally moved up in 1990 and 1991. Similarly, increases in 2007-09 were accompanied by a decline in the ratio. One could pick out other examples, but basically what is shown is that there is no systematic pattern.

C. More Rigorous Work on the Impact on Employment from Raising the Minimum Wage Also Shows No Harm

Graphs such as these are, however, simplistic. While looking at the history is of interest, and should show at least some indication that increases in the minimum wage will lead to higher unemployment (especially of the young) if the minimum wage critics were correct, there is much more going on in the economy which should be taken into account. Fortunately there have been rigorous studies that do this, and they too have found that the impact of increases in the minimum wage (of the magnitude historically seen) on unemployment rate is either non-existent or small. Some studies have indeed found that increases in the minimum wage have reduced unemployment.

The seminal paper that launched the modern literature on the impact of the minimum wage was co-authored by economists David Card (of University of California, Berkeley) and Alan Krueger (then of Princeton, and now Chairman of the Council of Economic Advisors in the White House). Card and Krueger controlled for extraneous effects that might be going on in the economy at the time a minimum wage is increased, by exploiting the fact that states may have separate minimum wage requirements from the federal requirements, and that states change their minimum wages at different times. Specifically, they looked at employment in fast food establishments along the border between New Jersey and Pennsylvania on an occasion when New Jersey raised its minimum wage while there was no change in Pennsylvania. They found no negative employment impact from New Jersey’s action. Indeed, there might have been a small positive impact on employment following the increase in New Jersey’s minimum wage.

The Card and Krueger study, while rigorous, was limited as it looked at only one instance of a change in the minimum wage, and the impact on only one industry. But more recent studies, following a similar approach, have extended the Card-Krueger work to many more cases. A particularly comprehensive recent example is a paper by the economists Arindrajit Dube, William Lester, and Michael Reich. Like Card-Krueger, they too found that increases in the minimum wage that have been periodically enacted in the US at the state level have not had a negative impact on employment of minimum wage workers. And since changes at the state level would presumably have a bigger impact than changes at the national level (as jobs could in principle shift across state lines), there is no reason to believe the impact of a federally mandated change would be negative.

There is of course much more work on this issue, and a paper by John Schmitt issued last month provides a good summary of where the literature stands. Less technical reviews of the issues and what economists have found are available here and here. There are, of course, economists who would disagree, but the preponderance of the work done so far has found little or no evidence that increases in the minimum wage that we have seen in the past have led to decreases in employment of such workers. Indeed, some studies have found that increases in the minimum wage increases employment.

D. Why Does Standard Economic Theory Get This Wrong?

The real world evidence matters more than the theory. But why would standard elementary economic theory appear to have gotten this wrong? The truth is that there are many matters in the real world that do not behave as one might predict based purely on an economic abstraction. Unemployment exists, for example, even though economic theory would predict that in a world of perfect competition, with full information and no transactions costs, and many other conditions, we should only see full employment. But the assumptions of abstract economic models might well not apply in critically important ways once one faces the specifics of a particular issue. That is why real world testing is important, as well as examination of the underlying assumptions and abstractions.

In the case of employment of workers at or close to the minimum wage, there are many reasons why the predictions of pure economic theory might well not apply. Such labor markets are far from the perfect competition ideal. There is a different balance of bargaining and other power between the employer and the potential minimum wage employee; the information available to each side of the transaction (on how productive the worker might be, and what his or her alternatives are) will differ; workers once they are in a job gain a good amount of job specific knowledge and abilities (not only on how to do the specific job, but also how best to work in a team with the specific colleagues there, where things are kept, and a million other details); that due to such job specific knowledge and imperfect information on who else might be available in the market, there will be substantial transactions costs incurred when an employee quits a job or is fired and a new one must be hired; and more. Standard theory predicts that workers (in a perfect market) will be paid the value of their marginal product, but it can be difficult even to know what the marginal product of a specific worker might be when they work, as they typically do, in a team with others. And one finds in the real world that wages are typically paid according to seniority and according to some hierarchy, rather than according to some strictly measured marginal productivity.

Good economists are therefore not surprised that markets in the real world can act quite differently from how the simple models might predict. And they therefore accept as quite possible the finding of the real world empirical studies that increases in the minimum wage, such as those observed in the past, might well not have led to jumps in unemployment of workers earning the minimum wage.

E. Conclusion

Full time workers in minimum wage jobs are poor, despite their evident willingness to work. Even if the minimum wage is raised to $9.00 an hour from the current $7.25 an hour, as Obama has proposed, these working poor will still be earning well less than poverty line income. And bringing the minimum wage to $9.00 an hour will only bring it back to where it was more than a half century ago. Real GDP per capita has more than doubled over this period. Yet minimum wage workers are currently earning 20% less.

Rigorous empirical studies do not show that increasing the minimum wage by an amount such as this will lead to an increase in unemployment of such workers. Nor does one see such an increase in unemployment in a more casual examination of the evidence, such as in the graphs above. While the poor need more assistance than just from this, increasing the minimum wage as Obama has proposed would certainly be an important help.

You must be logged in to post a comment.