A. Introduction

A. Introduction

Stock market performance is often taken to be a good measure of how the economy as a whole is performing. But it is not. For most Americans it is simply irrelevant, as the overwhelming share of investments in the stock markets are held by only a small segment of the population (the wealthy). And its track record as a broader indicator of how the economy is performing is imperfect at best.

Still, many do focus on stock market returns, and Trump brags that the performance of the market during his term in office has been spectacular.

That is not the case. This post will look at how the stock market has performed during Trump’s term in office thus far, and compare it to what that performance was under presidents going back to Reagan up to the same point in their terms.

First, however, we will briefly discuss to what extent one should expect stock market prices to reflect actions a president might be taking. And the answer is some, but there is much more going on.

B. Presidential Policies and the Stock Market

Owning shares of a firm entitles the owner to a share of the profits generated by that firm, both now and into the future. And while there are many complications, a simple metric commonly used to assess the price of a share in a firm, is the price/earnings ratio. If earnings (profits) go up, now and into the future, then for a given price/earnings ratio the price of the stock would go up in proportion.

Economic policies affect profits. And in a thriving economy, profits will also be rising. The policies of a presidential administration will affect this, and although the link is far from a tight one (with important lags as well), policies that are good for the economy as a whole will generally also lead to a rising stock market.

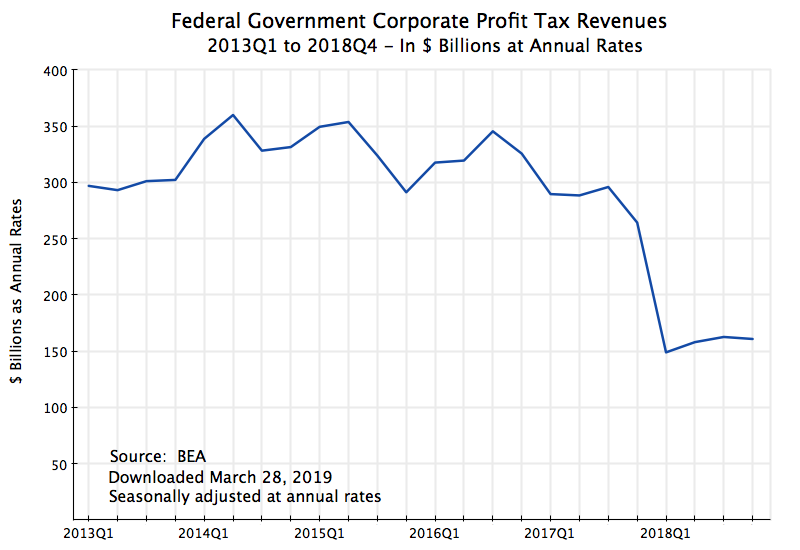

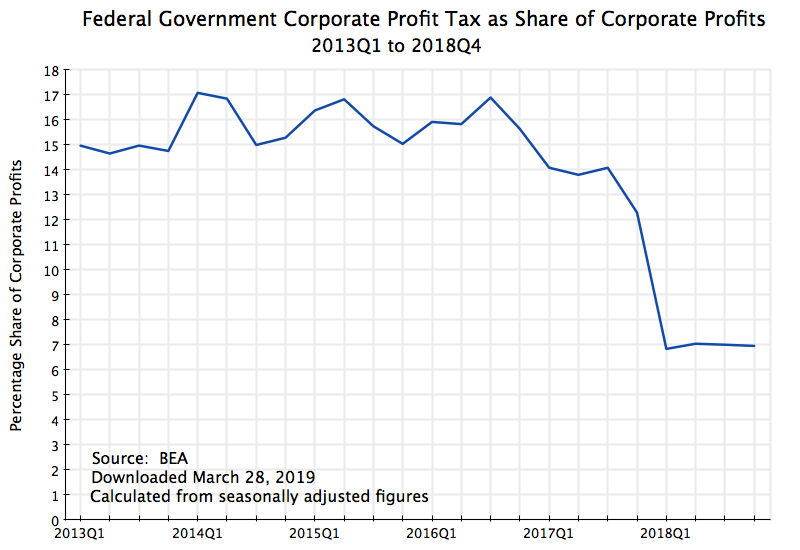

But there is also a more specific link to policy. What accrues to the shareholders are not overall profits, but profits after taxes. And this changed significantly as a result of the new tax law pushed through Congress by Trump and the Republicans in December 2017. It resulted in the effective corporate profits (income) tax being cut by more than half:

This chart is an update of one prepared for an earlier post on this blog (where one can see a further discussion of what lies behind it). It shows corporate profit taxes at the federal level as a share of corporate profits (calculated from figures in the national income accounts issued by the BEA). While Trump and the Republicans in Congress asserted the 2017 tax bill would not lead to lower corporate profit taxes being paid (as loopholes would be closed, they asserted), in fact they did. And dramatically so, with the effective corporate tax rate being slashed by more than half – from around 15 to 16% prior to 2017, to just 7% or so since the beginning of 2018 (and to just 6.3% most recently).

This chart is an update of one prepared for an earlier post on this blog (where one can see a further discussion of what lies behind it). It shows corporate profit taxes at the federal level as a share of corporate profits (calculated from figures in the national income accounts issued by the BEA). While Trump and the Republicans in Congress asserted the 2017 tax bill would not lead to lower corporate profit taxes being paid (as loopholes would be closed, they asserted), in fact they did. And dramatically so, with the effective corporate tax rate being slashed by more than half – from around 15 to 16% prior to 2017, to just 7% or so since the beginning of 2018 (and to just 6.3% most recently).

This cut therefore led to a significant increase in after-tax profits for any given level of before-tax profits, which has accrued to the shareholders. Note that this would not be due to the corporations becoming more productive or efficient, but rather simply from taxing profits less and shifting the tax burden then on to others (i.e. a redistributive effect). And based on a reduction in the taxes from 16% of corporate profits to 7%, after-tax profits would have gone from 84% of profits to 93%, an increase of about 11%. For any given price/earnings ratio, one would then expect stock prices, for this reason alone, to have gone up by about 11%.

[Side note: Technically one should include in this calculation also the impact of taxes on profits by other government entities – primarily those of state and local governments. These have been flat at around 3 1/2% of profits, on average. With these taxes included, after-tax profits rose from 80 1/2% of before-tax profits to 89 1/2%, an increase that is still 11% within round-off.]

One should therefore expect that stock prices following this tax cut (or in anticipation of it) would have been bumped up by an additional 11% above what they otherwise would have been. Other things equal, the performance of the stock market under Trump should have looked especially good as a result of the shift in taxes away from corporations onto others. But what has in fact happened?

C. Trump vs. Obama

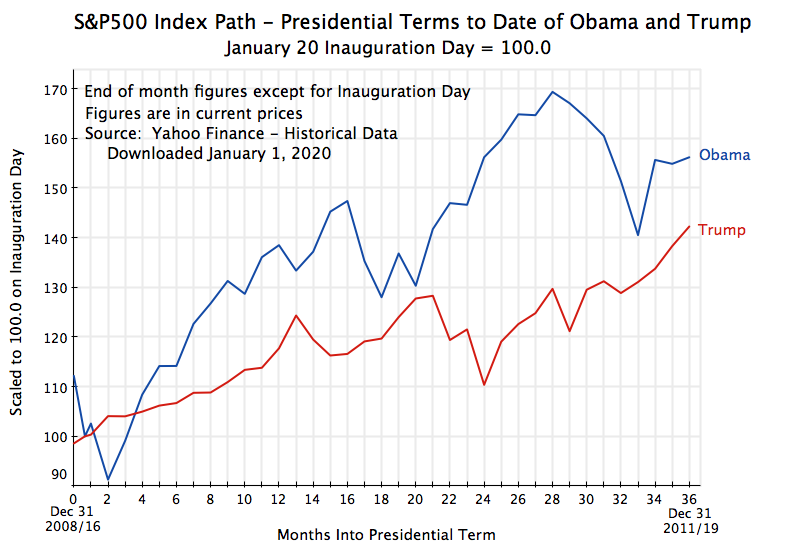

The chart at the top of this post compares the performance of the stock market during Trump’s term in office thus far (through December 31, 2019) to that under Obama to the same point in his first term in office. The difference is clear. Other than during Obama’s first few months in office, when he inherited from George W. Bush an economy in freefall, stock market performance under Obama was always better than it has been under Trump. Even after slashing corporate profit taxes by more than half, the stock market under Trump did not do exceptionally well.

The S&P500 Index is being used as the measure of the US stock market. Most professionals use this index as the best indicator of overall stock market performance, as it is comprehensive and broad (covering the 500 largest US companies as measured by stock market value, with the companies weighted in the index based on their market valuations). The data were downloaded from Yahoo Finance, where it is conveniently available (with daily values for the index going back to 1927), but can be obtained from a number of sources. The chart shows end-of-month figures, starting from December 31 of the month before inauguration, and going through to December 31 of their third year in office. The index is scaled to 100.0 on exactly January 20 (with this presented as “month” 0.65).

So if one wants to claim “bragging rights” for which president saw a better stock market performance, Obama wins over Trump, at least so far in their respective terms.

D. Trump vs. All Presidents Since Reagan

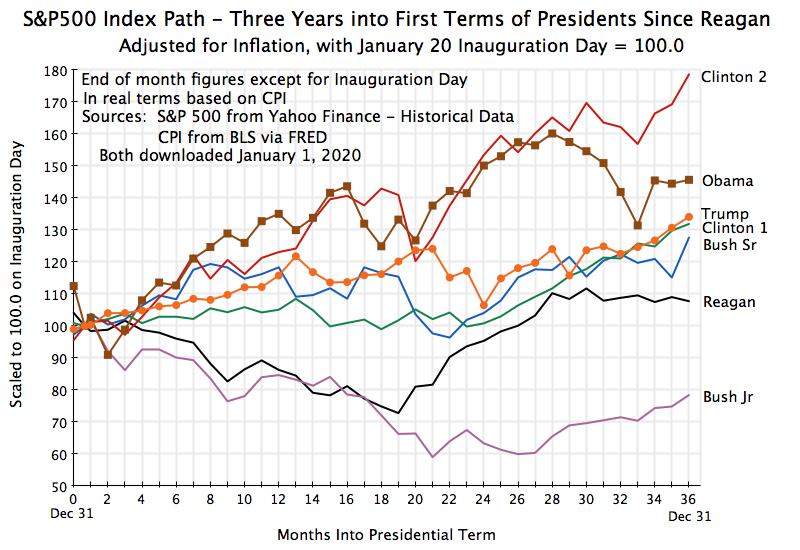

A comparison to just one president is limited. How does the performance under Trump compare to that under other US presidents up to the same points in their terms in office? Trump is roughly in the middle:

This chart tracks the performance under each president since Reagan up through the third year of their first terms in office. I have adjusted here for inflation (using the CPI), as inflation was substantially higher during the Reagan and Bush Sr. terms in office than it has been since. (I left the chart at the top of this post of just Obama vs. Trump in nominal terms as inflation in recent years has been steady and low. But for those interested in the impact of this, one can see the Obama and Trump numbers in real terms in the current chart.) I have included in this chart only the first terms of each president (with one exception) as the chart is already cluttered and was even more so when I had all the presidential terms.

The exception is that I included for perspective the stock market performance during Clinton’s second term in office. The stock market rose over that period by close to 80% in real terms, which was substantially higher than under any other president since at least before Reagan in either their first or second terms. The performance in Obama’s first term (of 146% in real terms) was the second-highest. There was then a set of cases which, at the three-year mark, showed surprising uniformity in performance, with increases of between 32% and 34% in the second Reagan term, the first Clinton term, the second Obama term, and Trump’s term so far. Bush Sr. was not far behind this set with an increase of 28%.

The worst performances were under Bush Jr. ( a fall of 22% to the third-year point in his first term), and Reagan (an increase of just 8% to that point in his first term).

So the performance of the market under Trump is in the middle – not the worst, but well below the best.

E. Single Year Increases in the S&P500 from 1946 to 2019

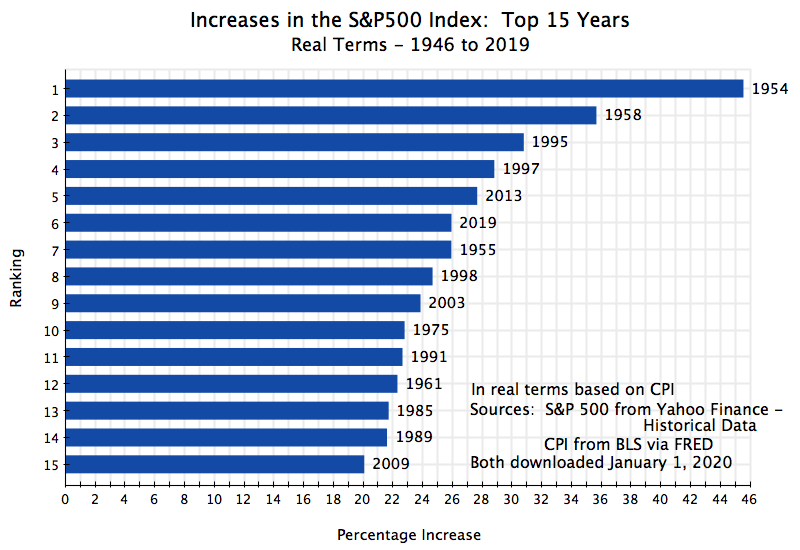

Finally, was the increase under Trump in his best single year so far (2019) a record? No, it was not. Looking at the single year performances (in real terms) since 1946, the top 15 were:

The increase in 2019, of 25.9%, was good, but only the sixth-highest of the 74 years between 1946 and 2019 (inclusive). The stock market rose by more in 2013 during Obama’s term in office (by 27.7%), and in 1997 (28.8%) and 1995 (30.8%) which were both Clinton years. And the highest increases were in 1958 (35.7%) and 1954 (45.6%) when Eisenhower was president.

The market also rose substantially in 2017, in Trump’s first year in office, by 16.9%. But it then fell by 8.0% in 2018, in Trump’s second year in office. Overall, the average rank (out of the 74 years from 1946 to 2019) of the individual year performances over the three years Trump has been in office so far, would place Trump in the middle third. Not the worst, but also far from the best. And comparing the three-year average while Trump has been president to rolling three-year averages since 1946, Trump’s average (of 11.6%) is well below the best. The highest was an average return of 25.3% in 1995-97 during Clinton’s term in office. And the three-year average return was also higher at 16.7% in 2012-14 during Obama’s term.

F. Summary and Conclusion

Trump likes to brag that the performance of the stock market during his term in office has been exceptional. But despite a slashing of corporate profit taxes (which, other things being equal would be expected to increase stock prices by 11%), the performance of the market during Trump’s term in office would put him in the middle. Specifically:

a) The market rose by more during the first three years of Obama’s term in office than it has under Trump;

b) Compared to the first three years in office of all presidents since Reagan (whether first terms only, or first and second terms) would place Trump in the middle. Indeed, the increase under Trump so far was almost exactly the same as the increases seen (at the three-year point) in Obama’s second term, in Reagan’s second term, and in Clinton’s first term. And the return under Trump was well below that seen in Obama’s first term, and especially far below that in Clinton’s second term.

c) The individual year performances during Trump’s three years have also not been exceptional. While the performance in 2019 was good, it was below that of a number of other years since World War II, and below that of individual years during Obama’s and Clinton’s terms in office.

But as noted at the start of this post, stock market returns should not be over-emphasized. An increase in the stock market does little for those who do not have the wealth to have substantial holdings in the stock market, and as a broader indicator of how the overall economy is performing, stock market returns are imperfect at best.

Still, one should be accurate in one’s claims. And as on many things, Trump has not been.

You must be logged in to post a comment.