A. Introduction

A. Introduction

The televised debate held October 15 between twelve candidates for the Democratic presidential nomination covered a large number of issues. Some were clear, but many were not. The debate format does not allow for much explanation or nuance. And while some of the positions taken refected sound economics, others did not.

In a series of upcoming blog posts, starting with this one, I will review several of the issues raised, focussing on the economics and sometimes the simple arithmetic (which the candidates often got wrong). And while the debate covered a broad range of issues, I will limit my attention here to the economic ones.

This post will look at the concern that was raised (initially in a question from one of the moderators) that the US will soon be facing a massive loss of jobs due to automation. A figure of “a quarter of American jobs” was cited. All the candidates basically agreed, and offered various solutions. But there is a good deal of confusion over the issue, starting with the question of whether such job “losses” are unprecedented (they are not) and then in some of the solutions proposed.

A transcript of the debate can be found at the Washington Post website, which one can refer to for the precise wording of the questions and responses. Unfortunately it does not provide pages or line numbers to refer to, but most of the economic issues were discussed in the first hour of the three hour debate. Alternatively, one can watch the debate at the CNN.com website. The discussion on job losses starts at the 32:30 minute mark of the first of the four videos CNN posted at its site.

B. Job Losses and Productivity Growth

A topic on which there was apparently broad agreement across the candidates was that an unprecedented number of jobs will be “lost” in the US in the coming years due to automation, and that this is a horrifying prospect that needs to be addressed with urgency. Erin Burnett, one of the moderators, introduced it, citing a study that she said concluded that “about a quarter of American jobs could be lost to automation in just the next 10 years”. While the name of the study was not explicitly cited, it appears to be one issued by the Brookings Institution in January 2019, with Mark Muro as the principal author. It received a good deal of attention when it came out, with the focus on its purported conclusion that there would be a loss of a quarter of US jobs by 2030 (see here, here, here, here, and/or here, for examples).

[Actually, the Brookings study did not say that. Nor was its focus on the overall impact on the number of jobs due to automation. Rather, its purpose was to look at how automation may differentially affect different geographic zones across the US (states and metropolitan areas), as well as different occupations, as jobs vary in their degree of exposure to possible automation. Some jobs can be highly automated with technologies that already exist today, while others cannot. And as the Brookings authors explain, they are applying geographically a methodology that had in fact been developed earlier by the McKinsey Global Institute, presented in reports issued in January 2017 and in December 2017. The December 2017 report is most directly relevant, and found that 23% of “jobs” in the US (measured in terms of hours of work) may be automated by 2030 using technologies that have already been demonstrated as technically possible (although not necessarily financially worthwhile as yet). And this would have been the total over a 14 year period starting from their base year of 2016. This was for their “midpoint scenario”, and McKinsey properly stresses that there is a very high degree of uncertainty surrounding it.]

The candidates offered various answers on how to address this perceived crisis (which I will address below), but it is worth looking first at whether this is indeed a pending crisis.

The answer is no. While the study cited said that perhaps a quarter of jobs could be “lost to automation” by 2030 (starting from their base year of 2016), such a pace of job loss is in fact not out of line with the norm. It is not that much different from what has been happening in the US economy for the last 150 years, or longer.

Job losses “due to automation” is just another way of saying productivity has grown. Fewer workers are needed to produce some given level of output, or equivalently, more output can be produced for a given number of workers. As a simple example, suppose some factory produces 100 units of some product, and to start has 100 employees. Output per employee is then 100/100, or a ratio of 1.0. Suppose then that over a 14 year period, the number of workers needed (following automation of some of the tasks) reduces the number of employees to just 75 to produce that 100 units of output (where that figure of 75 workers includes those who will now be maintaining and operating the new machines, as well as those workers in the economy as a whole who made the machines, with those scaled to account for the lifetime of the machines). The productivity of the workers would then have grown to 100/75, or a ratio of 1.333. Over a 14 year period, that implies growth in productivity of 2.1% a year. More accurately, the McKinsey estimate was that 23% of jobs might be automated, and with this the increase in productivity would be to 100/77 = 1.30. The growth rate over 14 years would then be 1.9% per annum.

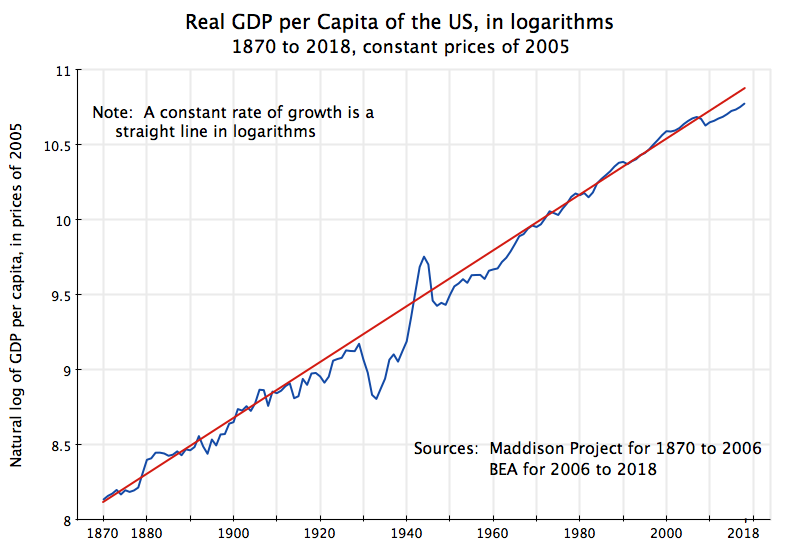

Such an increase in productivity is not outside the norm for the US. Indeed, it matches what the US has experienced over at least the last century and a half. The chart at the top of this post shows how GDP per capita has grown since 1870. The chart is plotted in logarithms, and those of you who remember their high school math will recall that a straight line in such a graph depicts a constant rate of growth. An earlier version of this chart was originally prepared for a prior post on this blog (where one can find further discussion of its implications), and it has been updated here to reflect GDP growth in recent years (using BEA data, with the earlier data taken from the Maddison Project).

What is remarkable is how steady that rate of growth in GDP per capita has been since 1870. One straight line fits it extraordinarily well for the entire period, with a growth rate of 1.9% a year (or 1.86% to be more precise). And while the US is now falling below that long-term trend (since around 2008, from the onset of the economic collapse in the last year of the Bush administration), the deviation of recent years is not that much different from an earlier such deviation between the late 1940s to the mid-1960s. It remains to be seen whether there will be a similar catch-up to the long-term trend in the coming years.

One might reasonably argue that GDP per capita is not quite productivity, which would be GDP per employee. Over very long periods of time population and the number of workers in that population will tend to grow at a similar pace, but we could also look at GDP per employee:

This chart is based on BEA data, the agency which issues the official GDP accounts for the US, for both real GDP and the number of employees (in full time equivalent terms, so part-time workers are counted in proportion to the number of hours they work). The figures unfortunately only go back to 1929, the oldest year for which the BEA has issued estimates. Note also that the rise in GDP during World War II looks relatively modest here, but that is because measures of “real” GDP (when carefully estimated using standard procedures) can deviate more and more as one goes back in time from the base year for prices (2012 here), coupled with major changes in the structure of production (such as during a major war). But the BEA figures are the best available.

This chart is based on BEA data, the agency which issues the official GDP accounts for the US, for both real GDP and the number of employees (in full time equivalent terms, so part-time workers are counted in proportion to the number of hours they work). The figures unfortunately only go back to 1929, the oldest year for which the BEA has issued estimates. Note also that the rise in GDP during World War II looks relatively modest here, but that is because measures of “real” GDP (when carefully estimated using standard procedures) can deviate more and more as one goes back in time from the base year for prices (2012 here), coupled with major changes in the structure of production (such as during a major war). But the BEA figures are the best available.

Once again one finds that the pace of productivity growth was remarkably stable over the period, with a growth rate here of 1.74% a year. It was lower during the Great Depression years, but then recovered during World War II, and was then above the 1929 to 2018 trend from the early 1950s to 1980. And the same straight line (meaning a constant growth rate) then fit extremely well from 1980 to 2010.

Since 2010 the growth in labor productivity has been more modest, averaging just 0.5% a year from 2010 to 2018. An important question going forward is whether the path will return to the previous trend. If it does, the implication is that there will be more job turnover for at least a temporary period. If it does not, and productivity growth does not return to the path it has been on since 1929, the US as a whole will not be able to enjoy the growth in overall living standards the economy had made possible before.

The McKinsey numbers for what productivity growth might be going forward, of possibly 1.9% a year, are therefore not out of line with what the economy has actually experienced over the years. It matches the pace as measured by GDP per capita, and while the 1.74% a year found for the last almost 90 years for the measure based on GDP per employee is a bit less, they are close. And keep in mind that the McKinsey estimate (of 1.9% growth in productivity over 14 years) is of what might be possible, with a broad range of uncertainty over what will actually happen.

The estimate that “about” a quarter of jobs may be displaced by 2030 is therefore not out of line with what the US has experienced for perhaps a century and a half. Such disruption is certainly still significant, and should be met with measures to assist workers to transition from jobs that have been automated away to the jobs then in need of more workers. We have not, as a country, managed this very well in the past. But the challenge is not new.

What will those new jobs be? While there are needs that are clear to anyone now (as Bernie Sanders noted, which I will discuss below), most of the new jobs will likely be in fields that do not even exist right now. A careful study by Daron Acemoglu (of MIT) and Pascual Restrepo (of Boston University), published in the American Economic Review in 2018, found that about 60% of the growth in net new jobs in the US between 1980 and 2015 (an increase of 52 million, from 90 million in 1980 to 142 million in 2015) were in occupations where the specific title of the job (as defined in surveys carried out by the Census Bureau) did not even exist in 1980. And there was a similar share of those with new job titles over the shorter periods of 1990 to 2015 or 2000 to 2015. There is no reason not to expect this to continue going forward. Most new jobs are likely to be in positions that are not even defined at this point.

C. What Would the Candidates Do?

I will not comment on all the answers provided by the candidates (some of which were indecipherable), but just a few.

Bernie Sanders provided perhaps the best response by saying there is much that needs to be done, requiring millions of workers, and if government were to proceed with the programs needed, there would be plenty of jobs. He cited specifically the need to rebuild our infrastructure (which he rightly noted is collapsing, and where I would add is an embarrassment to anyone who has seen the infrastructure in other developed economies). He said 15 million workers would be required for that. He also cited the Green New Deal (requiring 20 million workers), as well as needs for childcare, for education, for medicine, and in other areas.

There certainly are such needs. Whether we can organize and pay for such programs is of course critical and would need to be addressed. But if they can be, there will certainly be millions of workers required.

Sanders was also asked by the moderator specifically about his federal jobs guarantee proposal (and indeed the jobs topic was introduced this way). But such a policy proposal is more problematic, and separate from the issue of whether the economy will need so many workers. It is not clear how such a jobs guarantee, provided by the federal government, would work. The Sanders campaign website provides almost no detail. But a number of questions need to be addressed. To start, would such a program be viewed as a temporary backstop for a worker, to be used when he or she cannot find another reasonable job at a wage they would accept, or something permanent? If permanent, one is really talking more of an expanded public sector, and that does not seem to be the intention of a jobs guarantee program. But if a backstop, how would the wage be set? If too high, no workers would want to leave and take a different job, and the program would not be a backstop. And would all workers in such a program be paid the same, or different based on their skills? Presumably one would pay an engineer working on the design of infrastructure projects more than someone with just a high school degree. But how would these be determined? Also, with a job guarantee, can someone be fired? Suppose they often do not show up for work?

So there are a number of issues to address, and the answers are not clear. But more fundamentally, if there is not a shortage of jobs but rather of workers (keep in mind that the unemployment rate is now at a 50 year low), why does one need such a guarantee? It might be warranted (on a temporary basis) during an economic downturn, when unemployment is high, but why now, when unemployment is low? [October 28 update: The initial version of this post had an additional statement here saying that the federal government already had “something close to a job guarantee”, as you could always join the Army. However, as a reader pointed out, while that once may have been true, it no longer is. So that sentence has been deleted.]

Andrew Yang responded next, arguing for his proposal of a universal basic income that would provide every adult in the country with a grant of $1,000 per month, no questions asked. There are many issues with such a proposal, which I will address in a subsequent blog post, but would note here that his basic argument for such a universal grant follows from his assertion that jobs will be scarce due to automation. He repeatedly asserted in the debate that we have now entered into what has been referred to as the “Fourth Industrial Revolution”, where automation will take over most jobs and millions will be forced out of work.

But as noted above, what we have seen in the US over the last 150 years (at least) is not that much different from what is now forecast for the next few decades. Automation will reduce the number of workers needed to produce some given amount, and productivity per worker will rise. And while this will be disruptive and lead to a good deal of job displacement (important issues that certainly need to be addressed), the pace of this in the coming decades is not anticipated to be much different from what the country has seen over the last 150 years.

A universal basic income is fundamentally a program of redistribution, and given the high and growing degree of inequality in the US, a program of redistribution might well be warranted. I will discuss this is a separate blog post. But such a program is not needed to provide income to workers who will be losing jobs to automation, as there will be jobs if we follow the right macro policies. And $12,000 a year would not nearly compensate for a lost job anyway.

Elizabeth Warren’s response to the jobs question was different. She argued that jobs have been lost not due to automation, but due to poor international trade policies. She said: “the data show that we have had a lot of problems with losing jobs, but the principal reason has been bad trade policy.”

Actually, this is simply not true, and the data do not support it. There have been careful studies of the issue, but it is easy enough to see in the numbers. For example, in an earlier post on this blog from 2016, I examined what the impact would have been on the motor vehicle sector if the US had moved to zero net imports in the sector (i.e. limiting car imports to what the US exports, which is not very much). Employment in the sector would then have been flat, rather than decline by 17%, between the years 1967 and 2014. But this impact would have been dwarfed by the impact of productivity gains. The output of the motor vehicle (in real terms) was 4.5 times higher in 2014 than what it was in 1967. If productivity had not grown, they would then have required 4.5 times as many workers. But productivity did grow – by 5.4 times. Hence the number of workers needed to produce the higher output actually went down by the 17% observed. Banning imports would have had almost no effect relative to this.

D. Summary and Conclusion

Automation is important, but is nothing new. The Luddites destroyed factory machinery in the early 1800s in England due to a belief that the machines were taking away their jobs and that they would then be left with no prospects. And data for the US that goes back to at least 1870 shows such job “destroying” processes have long been underway. They have not accelerated now. Indeed, over the past decade the pace has slowed (i.e. less job “destruction”). But it is too soon to tell whether this deceleration is similar to fluctuations seen in the past, where there were occasional deviations but then always a return to the long-term path.

Looking forward, careful studies such as those carried out by McKinsey have estimated how many jobs may be exposed to automation (using technologies that we know already to be technically feasible). While they emphasize that any such forecasts are subject to a great deal of uncertainty, McKinsey’s midpoint scenario estimates that perhaps 23% of jobs may be substituted away by automation between 2016 and 2030. If so, such a pace (of 1.9% a year) would be similar to what productivity growth has been historically in the US. There is nothing new here.

But while nothing new, that does not mean it should be ignored. It will lead, just as it has in the past, to job displacement and disruption. There is plenty of scope for government to assist workers in finding appropriate new jobs, and in obtaining training for them, but the US has historically never done this all that well. Countries such as Germany have been far better at addressing such needs.

The candidate responses did not, however, address this (other than Andrew Yang saying government supported training programs in the US have not been effective). While Bernie Sanders correctly noted there is no shortage of needs for which workers will be required, he has also proposed a jobs guarantee to be provided by the federal government. Such a guarantee would be more problematic, with many questions not yet answered. But it is also not clear why it would be needed in current circumstances anyway (with an economy at full employment).

Andrew Yang argued the opposite: That the economy is facing a structural problem that will lead to mass unemployment due to automation, with a Fourth Industrial Revolution now underway that is unprecedented in US history. But the figures show this not to be the case, with forecast prospects similar to what the US has faced in the past. Thus the basis for his argument that we now need to do something fundamentally different (a universal basic income of $1,000 a month for every adult) falls away. And I will address the $1,000 a month itself in a separate blog post.

Finally, Elizabeth Warren asserted that the problem stems primarily from poor international trade policy. If we just had better trade policy, she said, there would be no jobs problem. But this is also not borne out by the data. Increased imports, even in the motor vehicle sector (which has long been viewed as one of the most exposed sectors to international trade), explains only a small fraction of why there are fewer workers needed in that sector now than was the case 50 years ago. By far the more important reason is that workers in the sector are now far more productive.

A. How Fast is GDP Growing?

A. How Fast is GDP Growing?

You must be logged in to post a comment.