A. Introduction

A. Introduction

The Bureau of Labor Statistics (BLS) released its regular monthly “Employment Situation” report, for November 2021, on Friday, December 3. The report is always eagerly awaited. It provides estimates for the net number of new jobs created in the most recent month, as well as figures on the unemployment rate, certain wage measures, and much else.

The initial reaction to the report by the media was negative. Net job growth, estimated at 210,000 in the month, was viewed as disappointing. This was down from 546,000 net new jobs in October, and was well below Wall Street expectations (based on a survey of Wall Street firms by Dow Jones) that the figure for November would come to 573,000. While it was noted that the unemployment rate also fell – to just 4.2% – the negative reaction contributed to a significant decline in the stock market that day, with the S&P 500 index, for example, down by over 2% at one point.

But the November jobs report was actually pretty solid. In this post, we will look at what was reported and some factors to take into account when examining such figures.

B. Monthly Job Gains in 2021

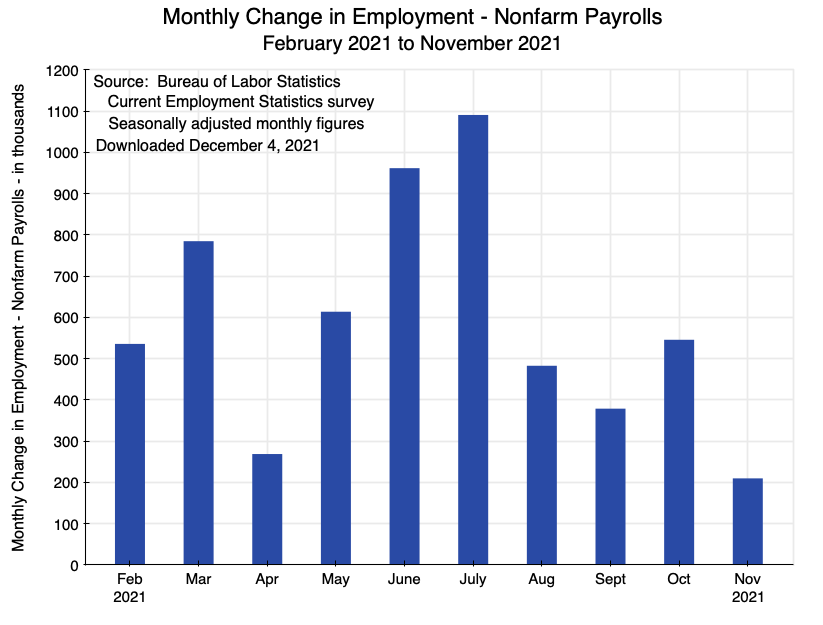

The chart at the top of this post shows the current BLS estimates of monthly net job growth this year, starting in February to cover the period of Biden’s presidency The estimates are based on a survey of establishments by the BLS, that asks (along with much else) the number of employees on their payroll as of the middle week of each month. Hence the January numbers would have been for before Biden’s January 20 inauguration. The news reports following the release by the BLS of the November jobs report were often accompanied by charts such as this one, with the November figure showing a substantial reduction in the number of net new jobs compared to what was seen in earlier months. The question of interest is whether this was significant.

A number of factors should be taken into account. One is simply that there is substantial month to month variation, as seen in the chart. This may be in part due to fluctuations in the economy, but may also be due to idiosyncratic factors (such as how the weather was in the week of the survey) and to statistical noise. The figures are based on surveys, and surveys are never perfect. Examined in context, the change in the November figure from the prior month is similar to the changes seen in other months this year. Indeed, it was less than in several.

There will, however, always be limitations with any single estimate, and in part for this reason the BLS provides in its published document a few different estimates for employment growth. The measure shown in the chart at the top is rightly considered the best one. It is based on a monthly survey (called the Current Employment Statistics, or CES, survey) of business and other establishments (including government entities as well as non-profits such as universities and hospitals) – whoever employs workers. The sample size is huge: 144,000 different businesses and government entities, at almost 700,000 different worksites. The BLS indicates this “sample” covers approximately one-third of all such jobs in the US.

The numbers are specifically for nonfarm payroll jobs, and hence exclude those employed on farms (which is now small in the US – about 1.4% of workers based on figures from other surveys) and more importantly the self-employed (about 6% of the labor force). Given the large sample size, and also recognizing that those in the sample include not only small firms but also large entities employing thousands of workers, statistical noise is limited. However, even with such a large sample size, the BLS states that the 90% confidence interval on the month to month changes in employment is +/- 110,000. At the more commonly accepted 95% confidence interval it would be wider.

Finally, the figures for the prior two months in each report are preliminary and subject to change as more complete data comes in. The November report, for example, indicated the estimate of net new jobs in October had been revised up by 15,000, and for September by 67,000. And the October report last month indicated that its earlier estimate for September had been revised up by 118,000. That is, the initial estimate for September had been 194,000 net new jobs, but this was revised up a month later to 312,000 net new jobs, and then revised again in the estimates published this month to 379,000. Such revisions are routine, and one should expect that the initial estimate for November of 210,000 net new jobs will likely be revised in the coming months as more complete data becomes available. While the revisions can in principle be positive or negative, in an expanding job market (as now) they are likely to be positive.

The figures in the chart are also seasonally adjusted. This is done via standard algorithms that estimate the normal annual pattern of employment changes in any given month based on historical data. Employment growth is normally higher in certain months of the year (such as June, following the end of the school year) and normally lower in other months (such as January). Analysts will therefore usually focus on the seasonally adjusted figures to see whether certain trends are developing outside of the normal seasonal fluctuations.

This is indeed appropriate. However, it is also worth recognizing that due to Covid, with the resulting lockdowns, opening-ups, quite prudent changes in consumer behavior due to the health risks from Covid-19 even with all the protective measures taken that can be taken, and the truly historic fiscal relief measures provided through the government budget to support households in the light of all these disruptions, seasonal patterns this year (and last) are likely to be not at all similar to what they have been historically. It is therefore of interest also to look at the underlying employment estimates, before the seasonal adjustment algorithms are run, to see what those numbers might be saying.

The next section will look at this, along with other measures of the change in employment.

C. Alternative Measures, and Long-Term Limits on What Employment Growth Could Be

As noted, the BLS makes available in its monthly Employment Situation report several measures of how employment is estimated to have changed in the month, in addition to the one discussed above. These additional measures should not be seen as better measures (at least in normal circumstances) than the seasonally adjusted measure based on the findings from the huge CES survey of establishments. Rather, it is best to see them as supplementary measures, or alternative measures, that together help us understand what may be going on in terms of employment. There is always uncertainty in any individual measure, as they are all estimates. It is better to look at several, to see what the overall story might be.

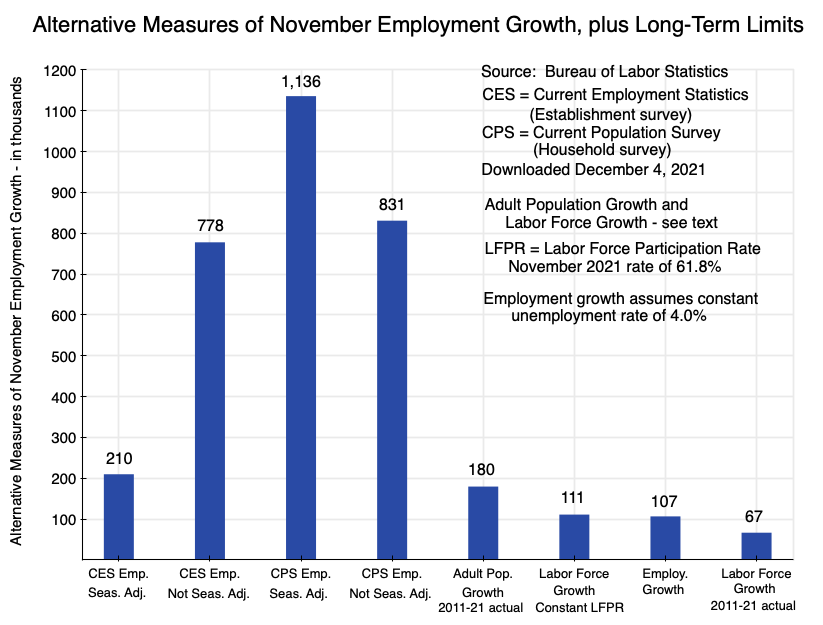

The estimated change in employment in November (or, more precisely, the change in nonfarm payroll), based on figures from the CES survey of establishments, was 210,000 after seasonal adjustment. But three alternative estimates for employment growth in November were far higher, as depicted in this chart:

In the CES estimate before the normal seasonal adjustment, the growth in net new jobs in November was 778,000. This difference between the seasonally adjusted and non-seasonally adjusted figures is substantially greater than what one has normally seen for November. Seasonal adjustment is complicated, but a simple average of the difference between the seasonally adjusted figures for November and the non-seasonally adjusted figures over the 20 years from 2000 to 2019, is 205,000. But in November 2021 it was 568,000, suggesting something unusual. If the November 2021 increase in the number of jobs was adjusted by 205,000 rather than the 568,000 estimated by the algorithms, then the “seasonally adjusted” change in the number of jobs would have been 573,000 (= 778,000 – 205,000). This is exactly what the pre-release expectation was on Wall Street (as noted at the start of this post). That it was exactly the same as the Wall Street forecast is just a coincidence, but the fact it was close at all might be significant. It may be suggesting that the standard seasonal adjustment calculations, built from patterns historically seen for the month, might not have captured well the circumstances in this highly unusual year.

Quite separately, the BLS also has an employment measure from the monthly survey of households conducted by the US Census Bureau (with BLS input on what is asked), called the Current Population Survey (CPS). This survey of a sample of 60,000 households is used by the BLS to determine how many are in the labor force (i.e. are working or are looking for work), whether they are employed (including self-employed and on farms), and thus the number unemployed (those in the labor force but not employed). The BLS uses this to determine the unemployment rate, but to get to that they have to first estimate, based on this survey, how many are employed.

The November estimates based on the CPS of net new employment were 1,136,000 for the seasonally adjusted figure and 831,000 for the figure before seasonal adjustment. Why the seasonal adjustment led to a reduction in the job growth estimate from the CPS while it led to an increase in the job growth estimate from the CES is not clear (seasonal adjustment is complicated), but in any case, both figures are relatively close to the 778,000 estimate from the CES estimate before seasonal adjustment. And all three are all well above the 210,000 seasonally adjusted estimate from the CES that we normally focus on. Together they suggest that the 210,000 estimate, while usually the most reliable one, might in this case be on the low side.

I have also included in the chart four figures for what I have termed the “long-term limits” on what monthly job growth might be for an economy at full employment. I included them on the same chart so that one can easily recognize the relative scale.

For an economy at full employment (with unemployment at frictional levels), employment growth cannot exceed the growth of the adult population. And indeed it will be less, as not all adults (defined by the BLS as all those in the population at age 18 and above) will be in the labor force – some will be retired, some will be students in college, some will have voluntarily left the labor force to raise children or provide care for others, and for other reasons. Examining what these limits are for the US will provide a sense of what monthly employment growth might be, on average, in the coming years.

First, on population: Population growth is relatively steady and predictable. For the ten-year period from November 2011 to November 2021, it averaged 180,000 per month in the US. It will be similar to this in the coming years, and it sets a (very) crude upper limit on what job growth could be in a steady state. But one can see even from this figure that it will not be possible to sustain forever monthly net new job growth of even 200,000. There will not be that many new adults available each month.

But 100% of the adult population are not in the labor force. As noted, some will be retired, some students, and so on. The labor force participation rate (LFPR) is the ratio of those who choose to be in the labor force (employed or looking for employment) to the adult population. In the November CPS figures, that LFPR was 61.8%. If one assumes that it will remain at that rate, then the monthly growth in the labor force will not be 180,000 (the growth in the adult population) but 61.8% of this, or 111,000. And if one assumes that unemployment will be something steady, at say 4% at full employment, then potential employment growth would be even less, at 107,000.

The implication is that if the labor force participation rate remains where it is now, one should not be surprised to see monthly figures on job growth of no more than roughly 100,000. This follows by simple arithmetic. It could be higher for some period (but not forever) if the labor force participation rate rises from the current 61.8%. This is possible, and perhaps even likely in the very near term, but probably not for long. The LFPR in fact rose in the November BLS report to 61.8% from 61.6% in the prior month. It normally changes only slowly over time. The disruption that followed from Covid-19 led to relatively wide swings at first, with the LFPR falling from 63.4% in January 2020 to 60.2% in April 2020 with the lockdowns. But by June 2020 it was back to 61.4% and since has fluctuated in a relatively narrow range before rising the 61.8% of November 2021.

What no one knows is what will happen to the LFPR now. It might rise a bit more, but the long term trend has been downward. It peaked in the year 2000, with a steady increase up until then following from a rising participation rate of women in the labor force. But since 2000 the participation rate for women has moved down, paralleling (but about 20% below) the slow downward trend seen for men since the mid-1950s. (The factors behind this are discussed in some detail in this earlier blog post.) It is due to this downward trend over the period of 2011 to 2021 that actual labor force growth over this period was just 67,000 per month (as depicted in the chart above) even though adult population growth was 180,000 per month over this same period.

The current 61.8% LFPR is in fact close to what a simple extrapolation of the trend since 2000 suggests it would be in November 2021. While the LFPR has behaved unusually since 2016 (when it flattened out for several years and indeed then rose a bit until the start of 2020, before collapsing and then partially recovering in the spring of 2020 due to the Covid-19 crisis), it is now back roughly to what one would find by a simple extrapolation of the trend since the year 2000.

There may well be surprises in what now happens to labor force participation. After the disruptions of the Covid-19 crisis, it may never revert to where it was just before the crisis. Those who retired early may mostly choose to stay retired. And many of those in low-paying jobs, particularly in cases of one spouse in a couple with young children, may have discovered during the Covid-19 crisis that one spouse dropping out of the labor force is not all that costly, and in a two-earner household they may be able to manage financially.

There is therefore a substantial degree of uncertainty on what will now happen to the LFPR. If it goes up, with a substantial number of adults re-entering the labor force, there will be a transition period when the labor force (and hence the number employed) could rise by significantly more than the 107,000 per month that one would see at a constant LFPR. Monthly changes in employment during this transition period could be substantial. For example (and again, this is simple arithmetic), if the LFPR were to increase from the current 61.8% by one percentage point to 62.8% (which would put it back to where it was in much of 2016 through 2018), then the number in the labor force would increase by 2.5 million over what would follow from regular population growth. Possible employment growth would be about the same 2.5 million if unemployment stays where it is now. Thus there could be a transition period of five months during which employment could potentially grow by 600,000 per month (a fifth of the extra 2.5 million in the labor force under this scenario, on top of about 100,000 per month from natural population growth). Or the transition period could be shorter or longer depending on the number of new jobs each month.

But the point is that even if the LFPR should rise, the impact would be a transitory one, after which one should expect employment growth each month of no more than 100,000 or so. And as noted before, the trend over the last 20 years has been that the LFPR has been moving downward, not upward.

D. Conclusion

The November jobs report was interpreted by many as disappointing, as the estimated number of net new jobs (based on the estimate normally used – and rightly so) was 210,000. This was seen as low, and the stock market fell. However, the report was in fact a pretty strong one, and analysts may have recognized this once they started to look at it more closely. While one never knows with any certainty why the stock market moves as it does (and there will always be other factors as well), the S&P 500, after falling by over 2% at one point on December 3, started to recover partially by the end of the day. And it then rose strongly on the next two trading days.

There are reasons to believe the estimate of 210,000 net new jobs in November may have been low. Seasonal adjustment factors mattered more than normally, and other measures of job growth were significantly higher. But even at 210,000, analysts need to recognize that as the economy returns to more normal conditions, monthly job growth will likely be a good deal less than that. While monthly job growth during Biden’s presidency from February to November has so far averaged over a half-million per month (588,000 per month to be more precise), this was only possible because the unemployment rate could come down. But unemployment is now low – it reached 4.2% in November – and cannot go much lower. If the labor force participation rate stays where it is now, possible employment growth will only be around 107,000 per month. If the LFPR rises, then this could go up for some transition period, but that transition period is limited in time and when it is over employment growth will then have to revert to something close to 100,000.

What is more likely is that the LFPR will now return to the longer-term trend seen since it reached its peak in the year 2000, and will fall slowly over time. Monthly employment growth would then be less, at something less than 100,000 per month (where how much less depends on the pace at which the LFPR falls).

Expectations have to be reset. Other than during a transition period should the labor force participation rate rise above where it is now, monthly net new jobs growth of 100,000 per month or so is likely to be the limit of what one will see. But that would be a good performance in an economy that remains at full employment. Only if unemployment shoots up due to some future downturn could one then see – during a recovery from that downturn – something more.

You must be logged in to post a comment.