A. Introduction

President Trump is repeatedly asserting that the economy under his presidency (in contrast to that of his predecessor) is booming, with economic growth and jobs numbers that are unprecedented, and all a sign of his superb management skills. The economy is indeed doing well, from a short-term perspective. Growth has been good and unemployment is low. But this is just a continuation of the trends that had been underway for most of Obama’s two terms in office (subsequent to his initial stabilization of an economy, that was in freefall as he entered office).

However, and importantly, the recent growth and jobs numbers are only being achieved with a high and rising fiscal deficit. Federal government spending is now growing (in contrast to sharp cuts between 2010 and 2014, after which it was kept largely flat until mid-2017), while taxes (especially for the rich and for corporations) have been cut. This has led to standard Keynesian stimulus, helping to keep growth up, but at precisely the wrong time. Such stimulus was needed between 2010 and 2014, when unemployment was still high and declining only slowly. Imagine what could have been done then to re-build our infrastructure, employing workers (and equipment) that were instead idle.

But now, with the economy at full employment, such policy instead has to be met with the Fed raising interest rates. And with rising government expenditures and falling tax revenues, the result has been a rise in the fiscal deficit to a level that is unprecedented for the US at a time when the country is not at war and the economy is at or close to full employment. One sees the impact especially clearly in the amounts the US Treasury has to borrow on the market to cover the deficit. It has soared in 2018.

This blog post will look at these developments, tracing developments from 2008 (the year before Obama took office) to what the most recent data allow. With this context, one can see what has been special, or not, under Trump.

First a note on sources: Figures on real GDP, on foreign trade, and on government expenditures, are from the National Income and Product Accounts (NIPA) produced by the Bureau of Economic Analysis (BEA) of the Department of Commerce. Figures on employment and unemployment are from the Bureau of Labor Statistics (BLS) of the Department of Labor. Figures on the federal budget deficit are from the Congressional Budget Office (CBO). And figures on government borrowing are from the US Treasury.

B. The Growth in GDP and in the Number Employed, and the Unemployment Rate

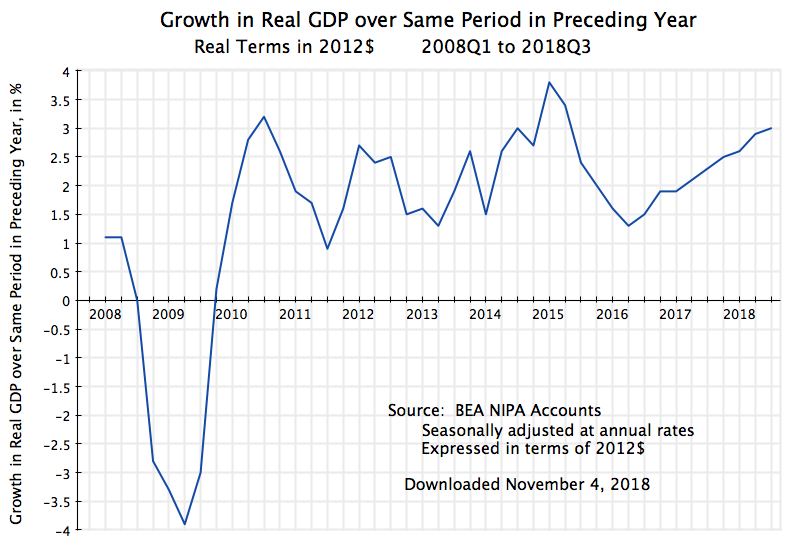

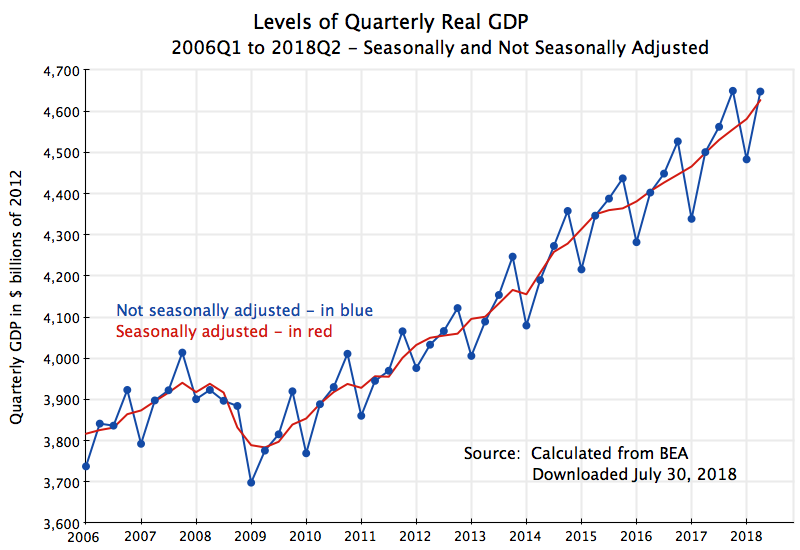

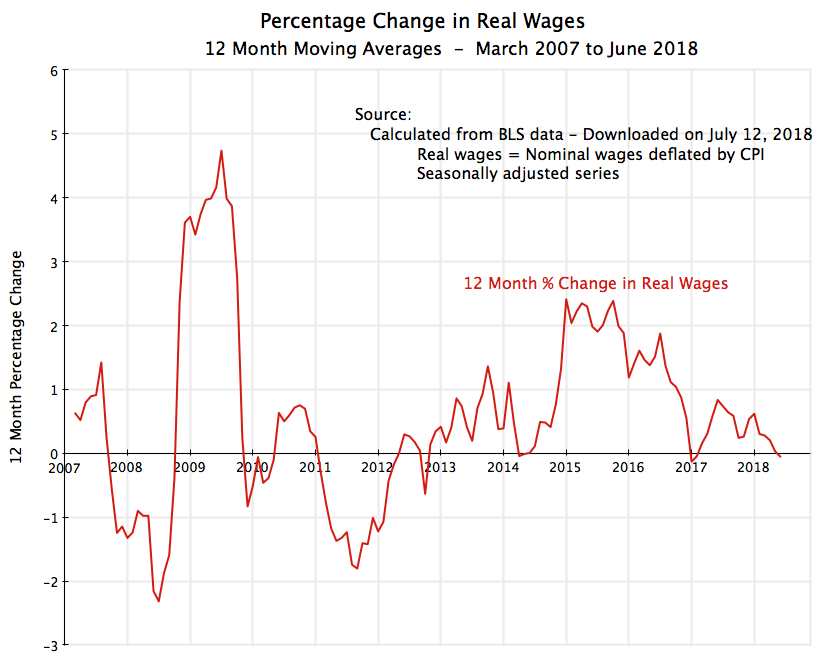

First, what has happened to overall output, and to jobs? The chart at the top of this post shows the growth of real GDP, presented in terms of growth over the same period one year before (in order to even out the normal quarterly fluctuations). GDP was collapsing when Obama took office in January 2009. He was then able to turn this around quickly, with positive quarterly growth returning in mid-2009, and by mid-2010 GDP was growing at a pace of over 3% (in terms of growth over the year-earlier period). It then fluctuated within a range from about 1% to almost 4% for the remainder of his term in office. It would have been higher had the Republican Congress not forced cuts in fiscal expenditures despite the continued unemployment. But growth still averaged 2.2% per annum in real terms from mid-2009 to end-2016, despite those cuts.

GDP growth under Trump hit 3.0% (over the same period one year before) in the third quarter of 2018. This is good. And it is the best such growth since … 2015. That is not really so special.

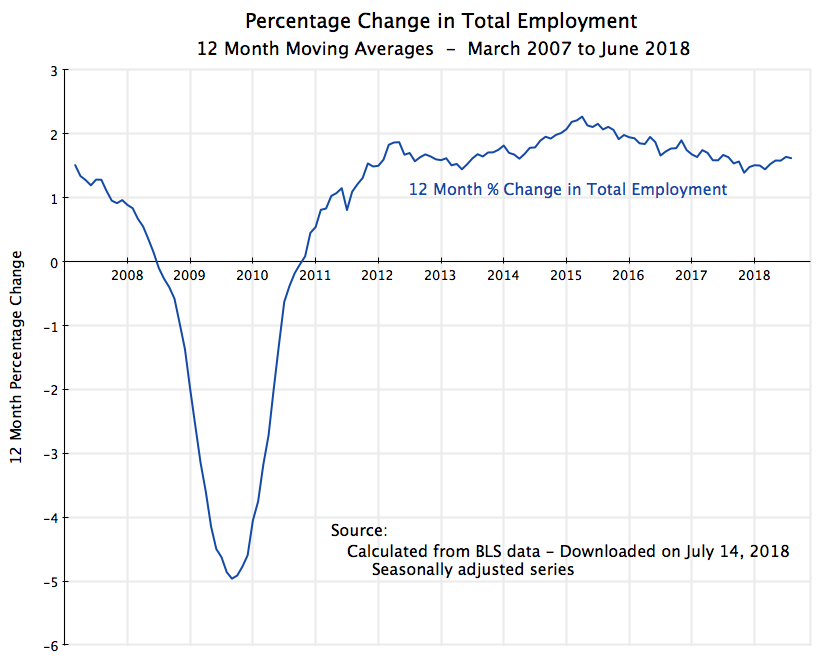

Net job growth has followed the same basic path as GDP:

Jobs were collapsing when Obama took office, he was quickly able to stabilize this with the stimulus package and other measures (especially by the Fed), and job growth resumed. By late 2011, net job growth (in terms of rolling 12-month totals (which is the same as the increase over what jobs were one year before) was over 2 million per year. It went to as high as 3 million by early 2015. Under Trump, it hit 2 1/2 million by September 2018. This is pretty good, especially with the economy now at or close to full employment. And it is the best since … January 2017, the month Obama left office.

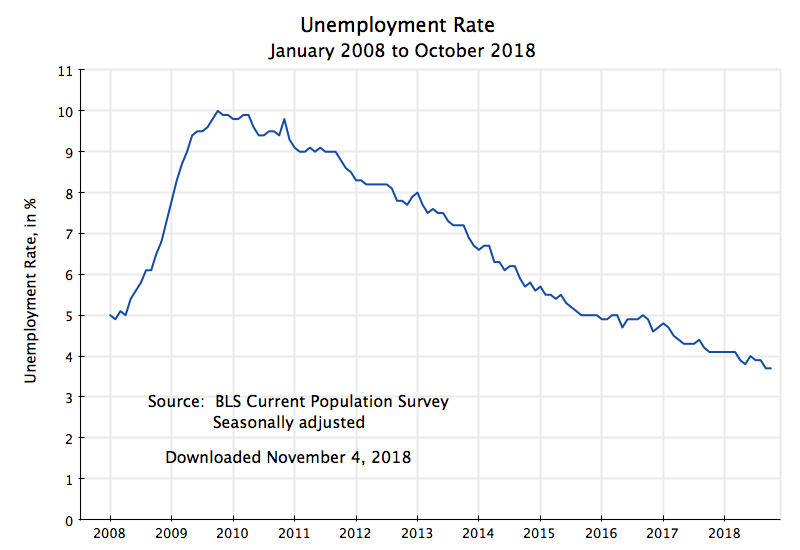

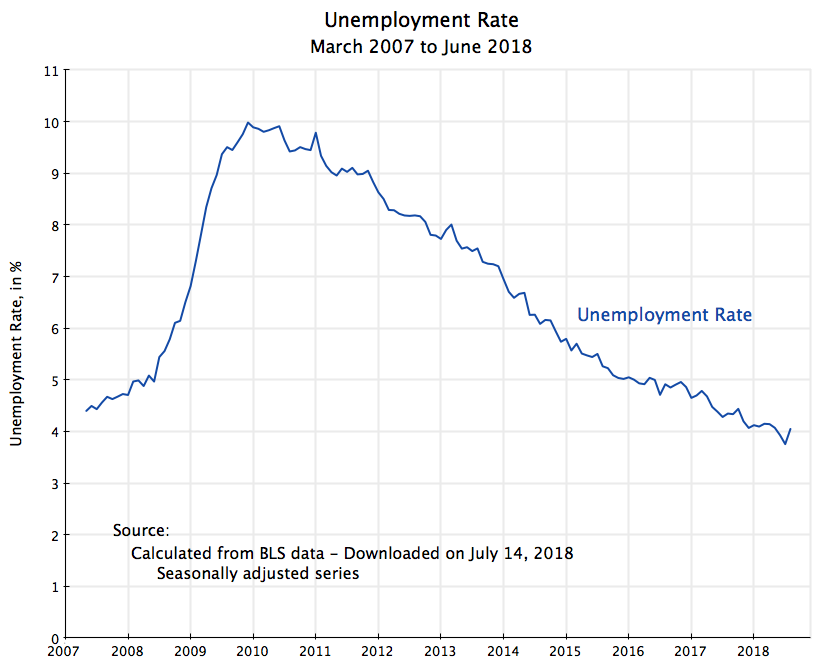

Finally, the unemployment rate:

Unemployment was rising rapidly as Obama was inaugurated, and hit 10% in late 2009. It then fell, and at a remarkably steady pace. It could have fallen faster had government spending not been cut back, but nonetheless it was falling. And this has continued under Trump. While commendable, it is not a miracle.

C. Foreign Trade

Trump has also launched a trade war. Starting in late 2017, high tariffs were imposed on imports of certain foreign-produced products, with such tariffs then raised and extended to other products when foreign countries responded (as one would expect) with tariffs of their own on selected US products. Trump claims his new tariffs will reduce the US trade deficit. As discussed in an earlier blog post, such a belief reflects a fundamental misunderstanding of how the trade balance is determined.

But what do we see in the data?:

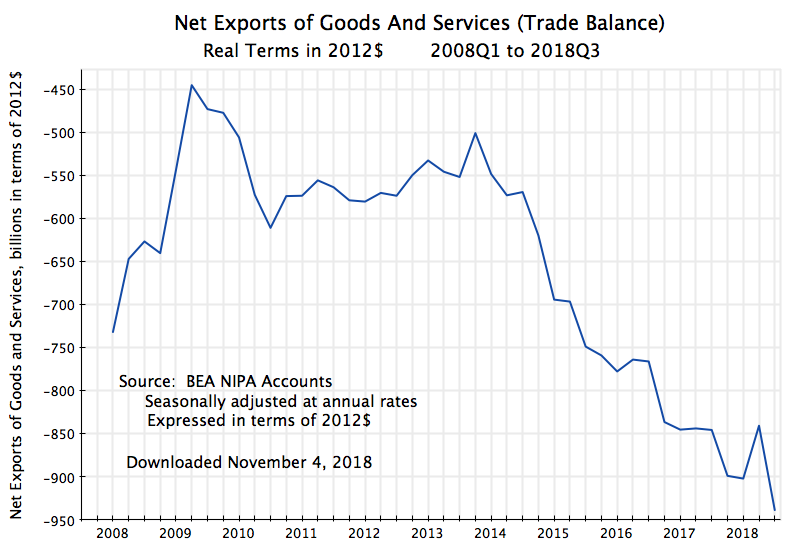

The trade deficit has not been reduced – it has grown in 2018. While it might appear there had been some recovery (reduction in the deficit) in the second quarter of the year, this was due to special factors. Exports primarily of soybeans and corn to China (but also other products, and to other countries where new tariffs were anticipated) were rushed out in that quarter in order arrive before retaliatory tariffs were imposed (which they were – in July 2018 in the case of China). But this was simply a bringing forward of products that, under normal conditions, would have been exported later. And as one sees, the trade balance returned to its previous path in the third quarter.

The growing trade imbalance is a concern. For 2018, it is on course for reaching 5% of GDP (when measured in constant prices of 2012). But as was discussed in the earlier blog post on the determination of the trade balance, it is not tariffs which determine what that overall balance will be for the economy. Rather, it is basic macro factors (the balance between domestic savings and domestic investment) that determine what the overall trade balance will be. Tariffs may affect the pattern of trade (shifting imports and exports from one country to another), but they won’t reduce the overall deficit unless the domestic savings/investment balance is changed. And tariffs have little effect on that balance.

And while the trend of a growing trade imbalance since Trump took office is a continuation of the trend seen in the years before, when Obama was president, there is a key difference. Under Obama, the trade deficit did increase (become more negative), especially from its lowest point in the middle of 2009. But this increase in the deficit was not driven by higher government spending – government spending on goods and services (both as a share of GDP and in constant dollar terms) actually fell. That is, government savings rose (dissavings was reduced, as there was a deficit). Private domestic savings was also largely unchanged (as a share of GDP). Rather, what drove the higher trade deficit during Obama’s term was the recovery in private investment from the low point it had reached in the 2008/09 recession.

The situation under Trump is different. Government spending is now growing, as is the government deficit, and this is driving the trade deficit higher. We will discuss this next.

D. Government Accounts

An increase in government spending is needed in an economic downturn to sustain demand so that unemployment will be reduced (or at least not rise by as much otherwise). Thus government spending was allowed to rise in 2008, in the last year of the Bush administration, in response to the downturn that began in December 2007. This continued, and was indeed accelerated, as part of the stimulus program passed by Congress soon after Obama took office. But federal government spending on goods and services peaked in mid-2010, and after that fell. The Republican Congress forced further expenditure cuts, and by late 2013 the federal government was spending less (in real terms) than it was in early 2008:

This was foolish. Unemployment was over 9 1/2% in mid-2010, and still over 6 1/2% in late-2013 (see the chart of the unemployment rate above). And while the unemployment rate did fall over this period, there was justified criticism that the pace of recovery was slow. The cuts in government spending during this period acted as a major drag on the economy, holding back the pace of recovery. Never before had a US administration done this in the period after a downturn (at least not in the last half-century where I have examined the data). Government spending grew especially rapidly under Reagan following the 1981/82 downturn.

Federal government spending on goods and services was then essentially flat in real terms from late 2013 to the end of Obama’s term in office. And this more or less continued through FY2017 (the last budget of Obama), i.e. through the third quarter of CY2018. But then, in the fourth quarter of CY2017 (the first quarter of FY2018, as the fiscal year runs from October to September), in the first full budget under Trump, federal government spending started to rise sharply. See the chart above. And this has continued.

There are certainly high priority government spending needs. But the sequencing has been terribly mismanaged. Higher government spending (e.g. to repair our public infrastructure) could have been carried out when unemployment was still high. Utilizing idle resources, one would not only have put people to work, but also would have done this at little cost to the overall economy. The workers were unemployed otherwise.

But higher government spending now, when unemployment is low, means that workers hired for government-funded projects have to be drawn from other activities. While the unemployment rate can be squeezed downward some, and has been, there is a limit to how far this can go. And since we are close to that limit, the Fed is raising interest rates in order to curtail other spending.

One sees this in the numbers. Overall private fixed investment fell at an annual rate of 0.3% in the third quarter of 2018 (based on the initial estimates released by the BEA in late October), led by a 7.9% fall in business investment in structures (offices, etc.) and by a 4.0% fall in residential investment (homes). While these are figures only for one quarter (there was a deceleration in the second quarter, but not an absolute fall), and can be expected to eventually change (with the economy growing, investment will at some point need to rise to catch up), the direction so far is worrisome.

And note also that this fall in the pace of investment has happened despite the huge cuts in corporate taxes from the start of this year. Trump officials and Republicans in Congress asserted that the cuts in taxes on corporate profits would lead to a surge in investment. Many economists (including myself, in the post cited above) noted that there was little reason to believe such tax cuts would sput corporate investment. Such investment in the US is not now constrained by a lack of available cash to the corporations, so giving them more cash is not going to make much of a difference. Rather, that windfall would instead lead corporations to increase dividends as well as share buybacks in order to distribute the excess cash to their shareholders. And that is indeed what has happened, with share buybacks hitting record levels this year.

Returning to government spending, for the overall impact on the economy one should also examine such spending at the state and local level, in addition to the federal. The picture is largely similar:

This mostly follows the same pattern as seen above for federal government spending on goods and services, with the exception that there was an increase in total government spending from early 2014 to early-2016, when federal spending was largely flat. This may explain, in part, the relatively better growth in GDP seen over that period (see the chart at the top of this post), and then the slower pace in 2016 as all spending leveled off.

But then, starting in late-2017, total government expenditures on goods and services started to rise. It was, however, largely driven by the federal government component. Even though federal government spending accounted only for a bit over one-third (38%) of total government spending on goods and services in the quarter when Trump took office, almost two-thirds (65%) of the increase in government spending since then was due to higher spending by the federal government. All this is classical Keynesian stimulus, but at a time when the economy is close to full employment.

So far we have focused on government spending on goods and services, as that is the component of government spending which enters directly as a component of GDP spending. It is also the component of the government accounts which will in general have the largest multiplier effect on GDP. But to arrive at the overall fiscal deficit, one must also take into account government spending on transfers (such as for Social Security), as well as tax revenues. For these, and for the overall deficit, it is best to move to fiscal year numbers, where the Congressional Budget Office (CBO) provides the most easily accessible and up-to-date figures.

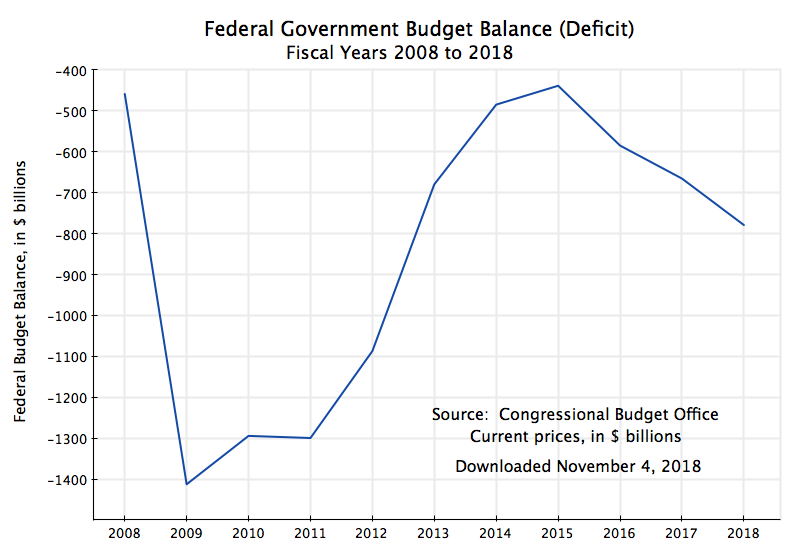

Tracing the overall federal fiscal deficit, now by fiscal year and in nominal dollar terms, one finds:

The deficit is now growing (the fiscal balance is becoming more negative) and indeed has been since FY2016. What happened in FY2016? Primarily there was a sharp reduction in the pace of tax revenues being collected. And this has continued through FY2018, spurred further by the major tax cut bill of December 2017. Taxes had been rising, along with the economic recovery, increasing by an average of $217 billion per year between FY2010 and FY2015 (calculated from CBO figures), but this then decelerated to a pace of just $26 billion per year between FY2015 and FY2018, and just $13 billion in FY2018. The rate of growth in taxes between FY2015 and FY2018 was just 0.8%, or less even than just inflation.

Federal government spending, including on transfers, also rose over this period, but by less than taxes fell. Overall federal government spending rose by an average of just $46 billion per year between FY2010 and FY2015 (a rate of growth of 1.3% per annum, or less than inflation in those years), and then by $140 billion per year (in nominal dollar terms) between FY2015 and FY2018. But this step up in overall spending (of $94 billion per year) was well less than the step down in the pace of tax collection (a reduction of $191 billion per year, the difference between $217 billion annual growth over FY2010-15 and the $26 billion annual growth over FY2015-18).

That is, about two-thirds (67%) of the increase in the fiscal deficit since FY2015 can be attributed to taxes being cut, and just one-third (33%) to spending going up.

Looking forward, this is expected to get far worse. As was discussed in an earlier post on this blog, the CBO is forecasting (in their most recent forecast, from April 2018) that the fiscal deficits under Trump will reach close to $1 trillion in FY2019, and will exceed 5% of GDP for most of the 2020s. This is unprecedented for the US economy at full employment, other than during World War II. Furthermore, these CBO forecasts are under the optimistic scenario that there will be no economic downturn over this period. But that has never happened before in the US.

Deficits need to be funded by borrowing. And one sees an especially sharp jump in the net amount being borrowed in the markets in CY 2018:

These figures are for calendar years, and the number for 2018 includes what the US Treasury announced on October 29 it expects to borrow in the fourth quarter. Note this borrowing is what the Treasury does in the regular, commercial, markets, and is a net figure (i.e. new borrowing less repayment of debt coming due). It comes after whatever the net impact of public trust fund operations (such as for the Social Security Trust Fund) is on Treasury funding needs.

The turnaround in 2018 is stark. The US Treasury now expects to borrow in the financial markets, net, a total of $1,338 billion in 2018, up from $546 billion in 2017. And this is at time of low unemployment, in sharp contrast to 2008 to 2010, when the economy had fallen into the worst economic downturn since the Great Depression Tax revenues were then low (incomes were low) while spending needed to be kept up. The last time unemployment was low and similar to what it is now, in the late-1990s during the Clinton administration, the fiscal accounts were in surplus. They are far from that now.

E. Conclusion

The economy has continued to grow since Trump took office, with GDP and employment rising and unemployment falling. This has been at rates much the same as we saw under Obama. There is, however, one big difference. Fiscal deficits are now rising rapidly. Such deficits are unprecedented for the US at a time when unemployment is low. And the deficits have led to a sharp jump in Treasury borrowing needs.

These deficits are forecast to get worse in the coming years even if the economy should remain at full employment. Yet there will eventually be a downturn. There always has been. And when that happens, deficits will jump even further, as taxes will fall in a downturn while spending needs will rise.

Other countries have tried such populist economic policies as Trump is now following, when despite high fiscal deficits at a time of full employment, taxes are cut while government spending is raised. They have always, in the end, led to disasters.

You must be logged in to post a comment.